Farm Managers’ and Rural Appraisers’ Assessment of Indiana’s Farmland Market**

April 23, 2012

PAER-2012-02

Craig Dobbins, Professor

![]()

![]()

![]()

![]()

![]()

The farm press and rural coffee shops have been abuzz this winter with discussions of farm land values in Indiana and other Midwestern states. In the February 2012 issue of the AgLetter, the Federal Reserve Bank of Chicago indicated that farmland values in the Seventh District (Iowa, and parts of Illinois, Indiana, Michigan, and Wisconsin) increased 22% from January 1, 2011 to January 1.2012. This was the largest annual increase since 1976.

To obtain a perspective about changes in Indiana’s farm land market, members of the Indiana Chapter of Farm Managers & Rural Appraisers were surveyed during their winter meeting on February 15, 2012. To obtain information about Indiana’s farmland market, members were asked to estimate current farm land values in the context of the following situation:

80 acres or more, all tillable, no buildings, capable of averaging 165 bushels of corn per year and 50 bushels of soybeans in a corn/bean rotation under typical management and not having special non-farm uses.

Thirty-two responses were received from people in 25 different Indiana counties. The average estimated price of farm land was $7,533 per acre. All of the respondents indicated their estimated price was higher than the value in February 2011. The average percentage increase from February 2011 to February 2012 was 14%. This makes the annual percentage increase less than the annual increase of 27% reported for Indiana in the Federal Reserve Bank of Chicago survey. The range in estimated increase provided by the farm managers and rural appraisers was 2% to 24%.

Attendees were also asked to estimate the cash rent for 2012 given the previously described situation. The average cash rent was $253 per acre. Twenty-seven of the respondents indicated that cash rent was higher than in 2011, and two respondents indicated it was the same. No one indicated a decline in cash rent. On average, the cash rent increased $28 per acre, an increase of 12.4%. There was a wide range in the estimated cash rent and cash rent change. Estimated cash rent varied from $150 to $400 per acre. The change in cash rent varied from $9 to $70 per acre.

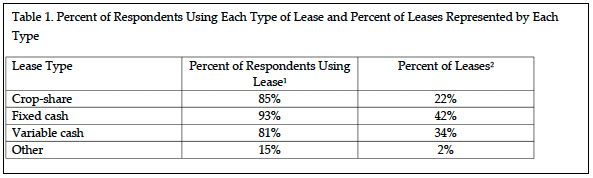

Table 1. Percent of Respondents Using Each Type of Lease and Percent of Leases Represented by Each Type

The increased variability of net returns associated with leasing farm land has prompted tenants and landlords to experiment with various types of adjustable leases. To get a sense of the type of lease used, attendees were asked to report the percentage of their cropland leases that were crop-share, fixed cash, variable cash, and other. The percentage of the respondents who reported using each type of lease and the percentage of their leases of each type are presented in Table 1.

Crop-share, fixed cash, and variable cash leases all had a high rate of usage among the respondents. Many of the respondents were using all three types of lease. The most commonly used lease was the fixed cash lease, averaging 42% of the leases. This was followed by the variable cash lease at 34%. Crop-share leases were 22% of the leases.

Many people ask if the increase in farm land values is likely to continue. The farm managers and rural appraisers were asked to provide two forecasts about future farm land values. One was where farm land values would be in one year. The second was where land values would be in five years. When asked about land values in one year, 75% of the respondents indicated that values would be higher. The other 25% said there would be no change. The expected increase averaged 8%, with a range of 5% to 12%.

There was less agreement about the change in farm land values over the next five years. In this case, 48% of the respondents indicated farm land values would be higher, 31% indicated there would be no change, and 21% indicated farm land values would be lower. For those respondents indicating that farm land values would be higher, the expected increase averaged 18% with a range from 10% to 25%. For those respondents expecting a decrease in farm land values, the decrease averaged 16%, with a range from 5% to 30%.

These results indicate that in the short term, Indiana’s farm land market is expected to remain strong. No one expects farm land values to decline for the year, but relative to the past few years, respondents expect the rate of increase to be much less. Longer term, there is less certainty in how farm land values will change. More respondents expect farm land values to be steady or higher than to decline in five years, but sound risk management suggests that the effect of a 15% to 20% decline in farm land values on the business should be explored.

Purdue’s annual survey of Indiana land values and cash rents will be conducted in June, with results published in the August 2012 Purdue Agricultural Economics Report.

1 These will not total 100% because a respondent often uses more than one type of lease.

2 Across the different types of leases the total will be 100%.

**A special thanks is expressed to the Indiana Chapter of Farm Managers and Rural Appraisers, which participated in the survey. Without their assistance it would not have been possible to take the pulse of Indiana’s farm land market.

![]()

![]()

![]()

![]()

![]()