Indiana Farm Operators Evaluate Community Services, Facilities, and Economic Conditions

June 16, 1990

PAER-1990-8

Author: Freddie L. Barnard, Associate Professor

![]()

![]()

![]()

![]()

![]()

Public attention during the 1980’s focused on the magnitude and severity of the financial hardships caused by the “farm crisis”, and on the adjustments needed to address financial problems at the farm and lending institution levels. However, little scientific inquiry was directed at understanding the long-term consequences of the crisis on rural communities. The economic condition of a rural community is of particular concern, since it affects the ability of that community to provide services to residents and to farm families.

This article reports the results of a survey of Indiana farm families that was conducted as part of a larger study in the twelve North Central states. The survey was conducted by the departments of Agricultural Economics and Agricultural Statistics at Purdue University with funding from the North Central Regional Center for Rural Development. The results reported here are the opinions of Indiana farmers on community services, shopping and childcare facilities, and economic conditions.

In February and early March 1989, 1400 Indiana farm operators were mailed a questionnaire. A total of 337 surveys were returned for a response rate of 24.1 percent. However, as noted in the summary table, the number of usable responses varied from question to question.

Opinions on Community Services, Facilities, and Economic Conditions

Farm operators were asked to evaluate community services, facilities, and economic conditions. The respondents indicated each had improved, stayed the same, or gotten worse over the past five years. Overall, the majority of respondents believed community services and facilities had either remained the same or improved. However, the respondents were not as positive about the economic conditions of farmers and agribusiness firms.

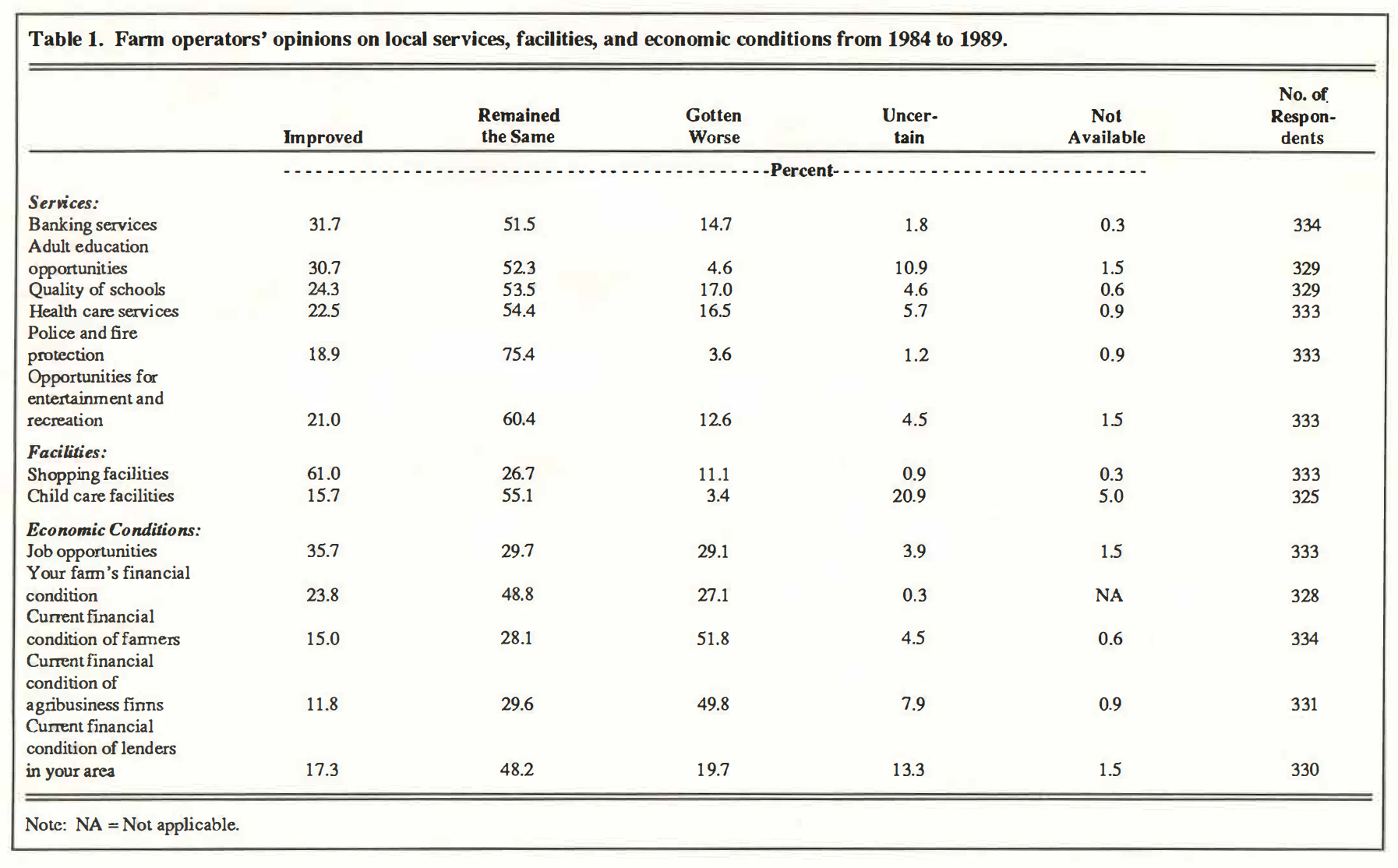

Services. More than 80 percent of the respondents felt each of the services evaluated had remained the same or improved (Table 1). Of particular interest is the evaluation of banking services. Senate Bill 1 was passed by the Indiana General Assembly in the spring of 1985. The legislation authorized cross-county branching for banks. At the time of passage there was concern about the availability of banking services to rural residents. Apparently, the concerns about banking services did not materialize into a problem. Nearly 32 percent of the respondents felt banking services have actually improved over the past five years, compared to only about 15 percent who felt banking services had gotten worse.

One adjustment several farm operators and spouses made during the 1980s to deal with financial stress was to seek off-farm employment. In some instances, individuals needed additional training to prepare themselves for offfarm jobs. Respondents reported adult education opportunities generally improved during the period studied. Nearly 31 percent of the respondents felt adult education opportunities improved over the past five years, compared to only about five percent who felt those opportunities had gotten worse.

Table 1. Farm operators’ opinions on local services, facilities, and economic conditions from 1984 to 1989.

In general, farm operators felt the quality of schools improved or remained the same, but a substantial percentage felt the quality had deteriorated. More than 24 percent felt the quality of schools improved, whereas 17 percent felt the quality deteriorated. When this finding is combined with the fact that the United States is becoming increasingly involved in a rapidly changing, global economy and many farm operators and spouses work at off-farm jobs, a concern surfaces about the ability of graduates from schools in rural areas to compete for off-farm jobs.

Likewise, farm operators generally felt healthcare services remained the same or improved, but a substantial percentage did indicate some concern about these services. More than 22 percent felt health-care services improved, but more than 16 percent felt those services had gotten worse. This concern may be the result of difficulties experienced in some rural communities in providing health-care services. Respondents may also be concerned about long-term health care for the elderly. Since 58 percent of the operators are 50 years of age or older and nearly 20 percent are 65 or older, they may be concerned about family members who require such care or concerned about their own care. Respondents did not specify which aspects of health-care services concerned them, but their concerns likely relate to availability, quality, and cost.

Respondents generally felt police and fire protection remained the same. The same opinion was expressed about opportunities for entertainment and recreation.

Facilities. Sixty-one percent of the respondents felt shopping facilities had improved, and only 11 percent felt those facilities had gotten worse. However, a much lower percentage (16 percent) felt child care facilities had improved. Although only about three percent felt those facilities had gotten worse, nearly 21 percent were uncertain. It should be noted the respondents to this question were operators, and 58 percent of those operators were 50 years of age or older. They may not be as familiar with child care facilities as their spouses. This may explain why 21 percent were uncertain about the facilities. Since many farm spouses work off the farm, there may be an increase in the demand for child care facilities in future years. Hence, this area needs further study.

Economic Conditions. A common adjustment made by some farm operators and spouses during the 1980s was to seek off-farm employment. A concern among community leaders, counselors, academicians, legislators, and others was the availability of off-farm jobs within commuting distances for those individuals. Nearly 36 percent of the respondents felt job opportunities had improved, which is an encouraging result. However, off-farm job opportunities are still not at an acceptable level, because 29 percent of the respondents felt off-farm job opportunities had gotten worse. Additional research is needed in this area to determine ways to diversify and more fully develop rural communities in Indiana.

Opinions on the financial condition of Hoosier farmers continue to vary widely. Nearly 49 percent of the respondents felt the financial condition of their own farm had remained the same. Over 27 percent felt their financial condition had gotten worse, compared to nearly 24 percent who felt their financial condition had improved.

Although nearly one-fourth of the respondents felt the financial condition of their own farm had improved, respondents were not as positive about the economic condition of all farmers and agribusiness firms. Over 51 percent of the respondents felt the current financial condition of all farmers had gotten worse. Only 15 percent felt the financial condition had improved. Since the financial condition of agribusiness firms depends on the financial condition of farmers, it is not surprising to find a similar attitude about agribusiness firms. Nearly 50 percent felt the current financial condition of agribusiness firms had gotten worse.

In general, respondents felt the financial condition of lenders had remained the same (48.2 percent). Only a slightly higher percentage felt the financial condition of lenders had gotten worse (19.7 percent) than felt it had improved (17.3 percent). The percentage who felt the financial condition of lenders had gotten worse is surprisingly low considering the well-publicized problems of the Farm Credit System, Farmers Home Administration, and the savings and loan industry.

Characteristics of Respondents

Age and Education. The average age of operators was 52.1 years. The average age of farm spouses was 49.7 years. Nearly 20 percent of the operators and about 13 percent of the spouses were 65 years of age or older. The average number of years of education for operators and spouses was 12.5 years. More than two-thirds of the operators and spouses have completed 9-12 years of formal education, and over one-fourth have gone on for post- secondary education.

Acres Farmed and Gross Farm Sales. The farm size reported by respondents is larger, in terms of acres farmed and gross farm sales, than reported in the 1987 Census. The average farm size of survey respondents, 489 acres, is more than double the size reported in the Census, 229 acres. Likewise, a higher percentage of respondents had gross farm incomes of $100,000 or more (26 percent) than was reported in the Census (15.5 percent). Therefore, the results from this survey are biased toward operators and spouses of larger farm operations.

Conclusion

This report summarizes data collected from a random sample of Indiana farm families. Respondents were asked to evaluate, over the past five years, the services, facilities, and economic conditions in their communities.

The results from this survey indicate there are at least three issues relating to services and facilities in rural communities that should be addressed by state leaders. The first issue is the availability of off-farm jobs. A related issue is the availability and quality of child care facilities. This issue will continue to be important in the 1990s as a greater number of farmers and spouses work off the farm. The second issue is the quality of schools. Students who attend schools in rural areas must receive a quality education to compete successfully in the high-tech, competitive economic environment of the 1990s. The third issue is the availability, quality, and cost of health-care services. This is particularly important for the elderly.

*This research is in part a contribution to Regional Project NC-184 and supported in part by the North Central Regional Center for Rural Development. Thanks are extended to the farmers who completed the questionnaires; to Ralph W. Gann, Head of the Department of Agricultural Statistics at Purdue University for helpful suggestions regarding design of the questionnaire and for supervising the collection of the survey data; and to Paul Lasley for coordinating the regional project. Helpful comments on earlier drafts of the manuscript by J.H. Atkinson, Professor, Janet S. Ayres and Christopher A. Hurt, Associate Professors, Department of Agricultural Economics at Purdue University are acknowledged.

![]()

![]()

![]()

![]()

![]()