Ag Barometer Drops Sharply on Concerns About Weak Farm Income

James Mintert and Michael Langemeier

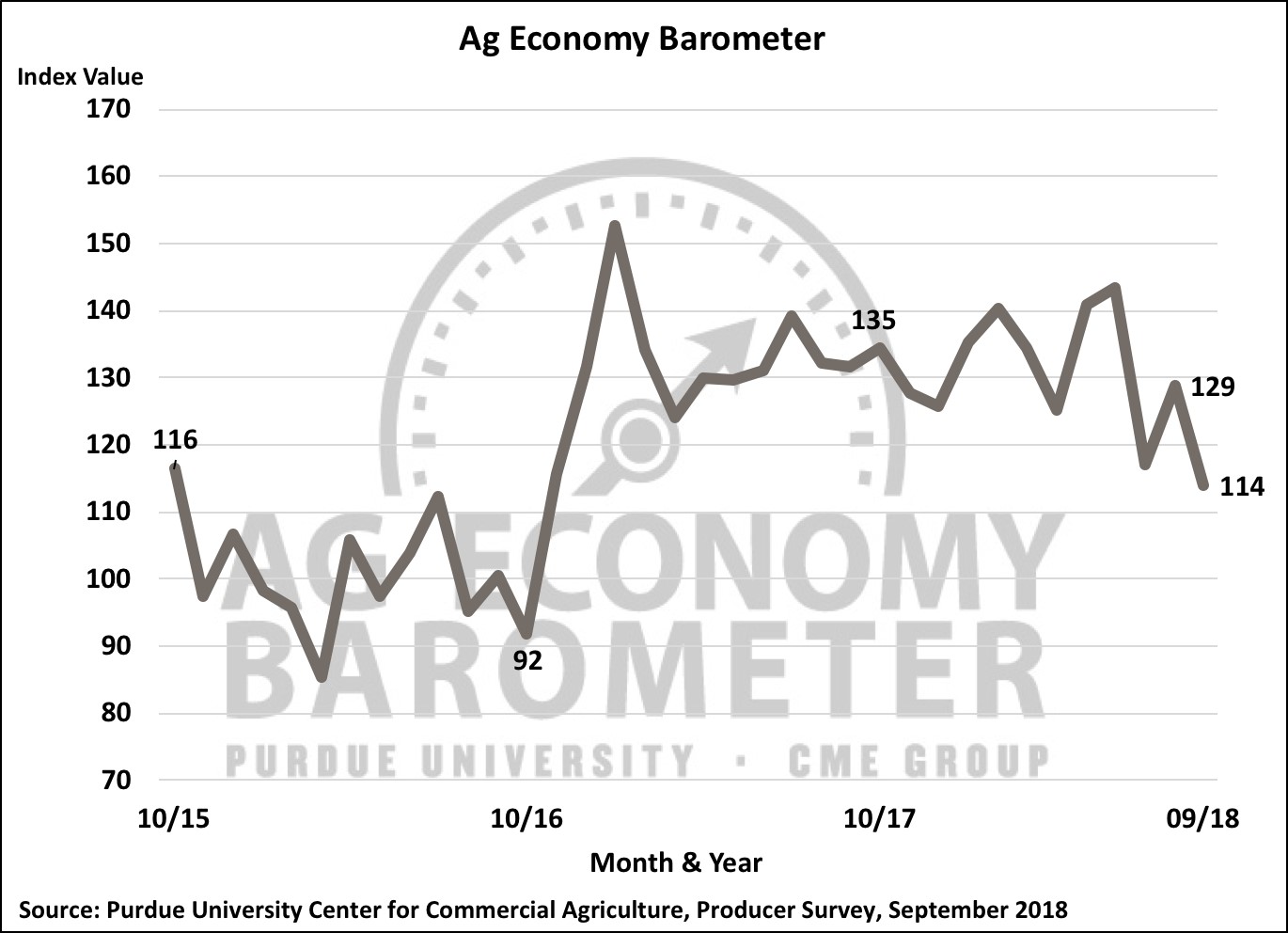

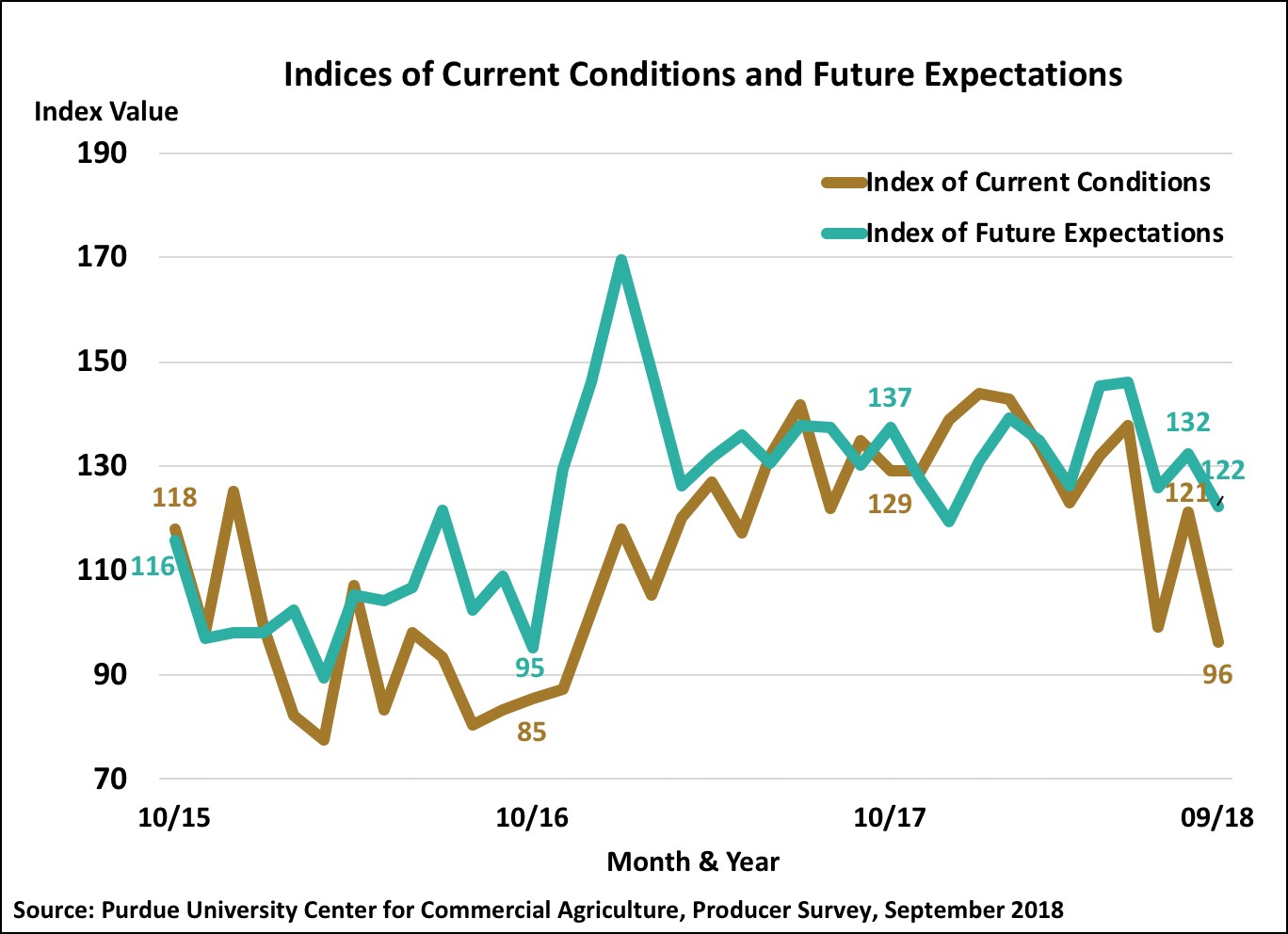

The Purdue University/CME Group Ag Economy Barometer fell to a reading of 114 in September, fifteen points below its August reading of 129 and its lowest reading since October 2016. September marked the second large decline in the barometer this summer, as it also declined precipitously in July. The barometer, a sentiment index based upon a nationwide monthly survey of 400 U.S. agricultural producers, has been unusually volatile in recent months. In June, the barometer came in at a reading of 143, but then declined sharply to 117 in July before recovering somewhat in August. This month’s decline was driven by declines in both of the barometer’s two sub-indices, the Index of Future Expectations, which fell 10 points and, especially, the Index of Current Conditions, which fell 25 points, both compared to their respective August readings.

Figure 1. Purdue/CME Group Ag Economy Barometer, October 2015-September 2018.

Figure 2. Indices of Current Conditions and Future Expectations, October 2015-September 2018.

Concerns about the impact of trade conflicts with major agricultural trading partners, especially China, continue to reverberate throughout the U.S. production agriculture sector. Exacerbating concerns about the impact of China’s tariffs on agricultural products has been unusually favorable weather conditions this summer leading to record yields, and large domestic supplies for corn and soybeans. Prices for both fall harvested crops experienced large price declines since June 1st with nearby corn futures declining 12 percent and nearby soybean futures declining 19 percent. The futures price declines were accentuated by unusually negative basis values for both commodities, especially soybeans, pushing cash prices down even further.

Farm Financial Conditions Deteriorating

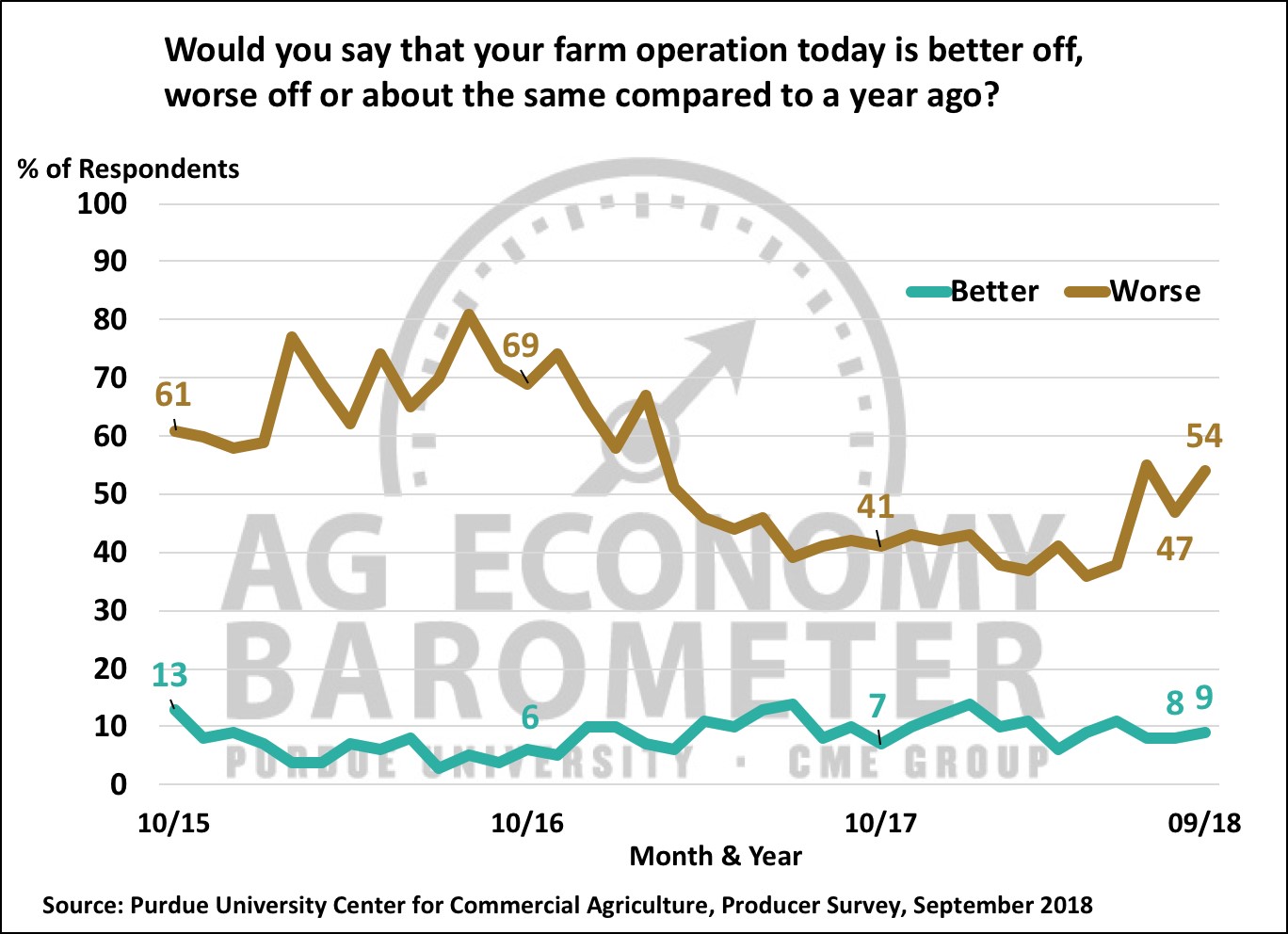

Producers indicated that financial conditions on many farms deteriorated significantly as 2018 unfolded and farmers’ expectations for the future weakened as well. On the September survey 54 percent of respondents said their farms’ financial condition was worse than a year earlier, compared to 47 percent in August and noticeably worse than the 36 percent recorded in May and 38 percent reached in June. Asked to look ahead, 33 percent of producers in September said they expect financial conditions on their farm to be worse a year from now, compared to 24 percent who felt that way in August and just 18 percent that expected worsening financial conditions as recently as June.

Figure 3. Would you say that your farm operation today is better off, worse off, or about the same compared to a year ago?, October 2015-September 2018.

Concerns extend beyond producers’ own farming operations to the broader agricultural economy. In September, 69 percent of producers said they expect bad times in the U.S. ag economy in the upcoming 12 months vs. 52 percent that felt that way in August. As recently as June, less than half (46 percent) of the respondents expected bad times in the upcoming year. The percentage of producers expecting a protracted downturn also increased on the September survey. This month 41 percent of producers said they expect widespread bad times in U.S. agriculture over the next five years, up 6 points from August and 10 points compared to the June survey.

Producers Backing Away from Making Large Farm Investments?

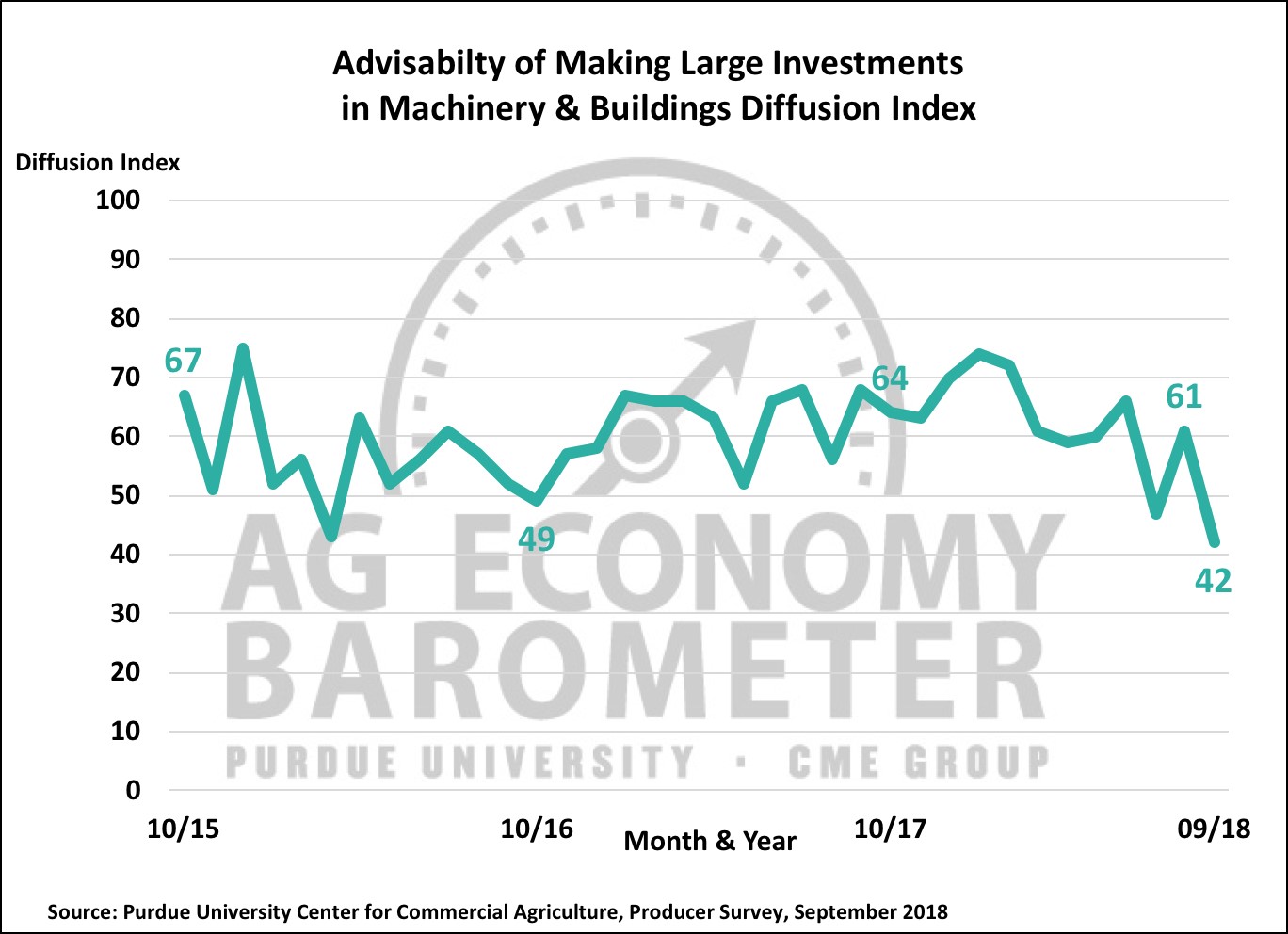

The negative perspective on the ag economy was particularly noticeable when producers were asked for their perspective on making large investments in farm machinery and buildings for their farming operation. Just 20 percent of respondents said now is a good time to make large farm investments and 78 percent said it was a bad time to make such investments. Combining the good and bad time responses into a diffusion index that can best characterize farmers perspective on making investments in farm machinery and buildings resulted in the most negative reading on large farm investments since the Ag Economy Barometer survey launched in October 2015.

Figure 4. Advisability of Making Large Investments in Machinery & Buildings Diffusion Index, October 2015-September 2018.

Trade Conflicts Lead Farmers to Expect Lower Incomes

The impact of trade conflicts on U.S. agriculture and farm incomes continues to be a source of angst among U.S. farmers. For the third month in row, 70 percent or more of farmers in our survey indicated that trade conflicts are expected to lower their farm’s net income in 2018. Farmers that expect to see income decline because of trade conflicts indicated they expect to see a larger income decline than when the same question was posed in August. In September 72 percent of respondents said they expect an income decline of more than 10 percent, up from 66 percent that expected an income decline of that magnitude in August and comparable to results from the July survey.

Figure 5. By how much do you expect your farm’s net income to decline because of trade conflicts?, October 2015-September 2018.

Farmers Expect Lower Farmland Cash Rental Rates in 2019

Farmers expect the farm income decline to put downward pressure on farmland cash rental rates and farmland values in the year ahead. Nearly two-thirds of respondents in both August and September said they expect 2019 farmland cash rental rates to decline compared to a year earlier. The percentage of respondents expecting lower farmland values in the year ahead rose to 32 percent in September, up slightly compared to August and 11 points higher than back in May. The percentage of producers expecting lower farmland values five years from now also rose in September to 19 percent compared to 14 percent in August. However, responding to the same question, the percentage of producers expecting higher farmland values five years from now rose in September to 46 percent vs. 42 percent in August, suggesting the negative outlook for farmland values is focused more on the near term.

Figure 6. Farmland cash rent expectations, 12 months ahead, August and September 2018.

Producer reaction to the Trump administration’s $12 billion relief plan changed little from the August survey, conducted before the plan’s details were made public, to the September survey, which was conducted after the specific compensation levels by commodity were announced by USDA. When asked to what degree does President Trump’s $12 billion relief plan relieve your concerns about the impact of tariffs on your farm’s income the percentage of respondents saying they were somewhat relieved increased slightly to 45 percent from 43 percent while 45 percent of respondents said they were not at all relieved, which was virtually unchanged from August.

Trade Conflicts Encouraging Farmers to Store More Soybeans Than Usual

Soybeans are one of the commodities hardest hit by China’s imposition of tariffs on select U.S. agricultural products. To learn more about how farmers are responding, we asked soybean growers about their storage plans for the soybean crop currently being harvested. Nearly one-fifth (18 percent) of soybean growers plan to store a higher percentage of their production than usual whereas nearly two-thirds (65 percent) of growers said they planned to store the same percentage of their soybeans as usual. Growers planning to store the same as usual or more than usual this fall were asked if they plan to store most of their soybeans until the trade conflict is settled. Although responses to this question were mixed, it did indicate the trade conflict is skewing some producers’ marketing decisions as 46 percent said they plan to store their soybeans until the trade conflict is settled. At the same time, 43 percent of soybean growers in our survey responded no to this question and 11 percent of growers were uncertain about storing soybeans until the conflict is settled. Finally, among producers storing a higher percentage of their soybean crop than usual (18 percent of soybean growers in the survey), two-thirds said the trade conflict with China is the primary factor influencing their soybean storage decision.

Figure 7. Do you plan to store most of your soybeans until the trade conflict is settled?, September 2018.