Farmer Sentiment Declines to Lowest Level Since June 2022 Amid Weakened Financial Outlook

James Mintert and Michael Langemeier, Purdue Center for Commercial Agriculture

A breakdown on the Purdue/CME Group Ag Economy Barometer April results can be viewed at https://purdue.ag/barometervideo. Find the audio podcast discussion for insight on this month’s sentiment at https://purdue.ag/agcast.

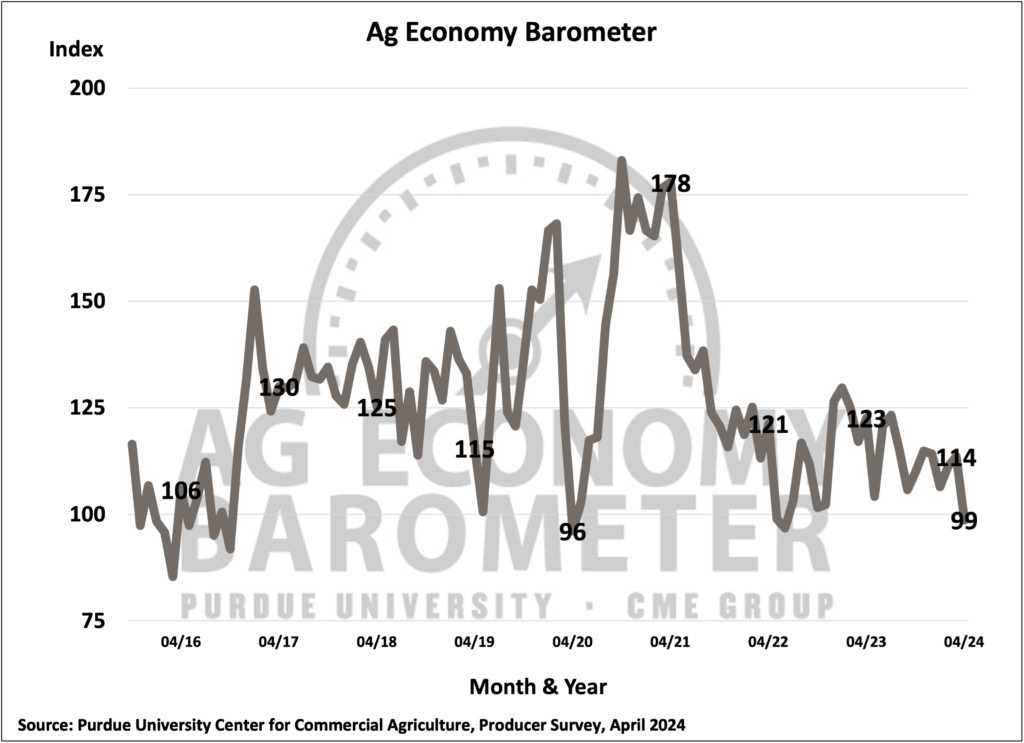

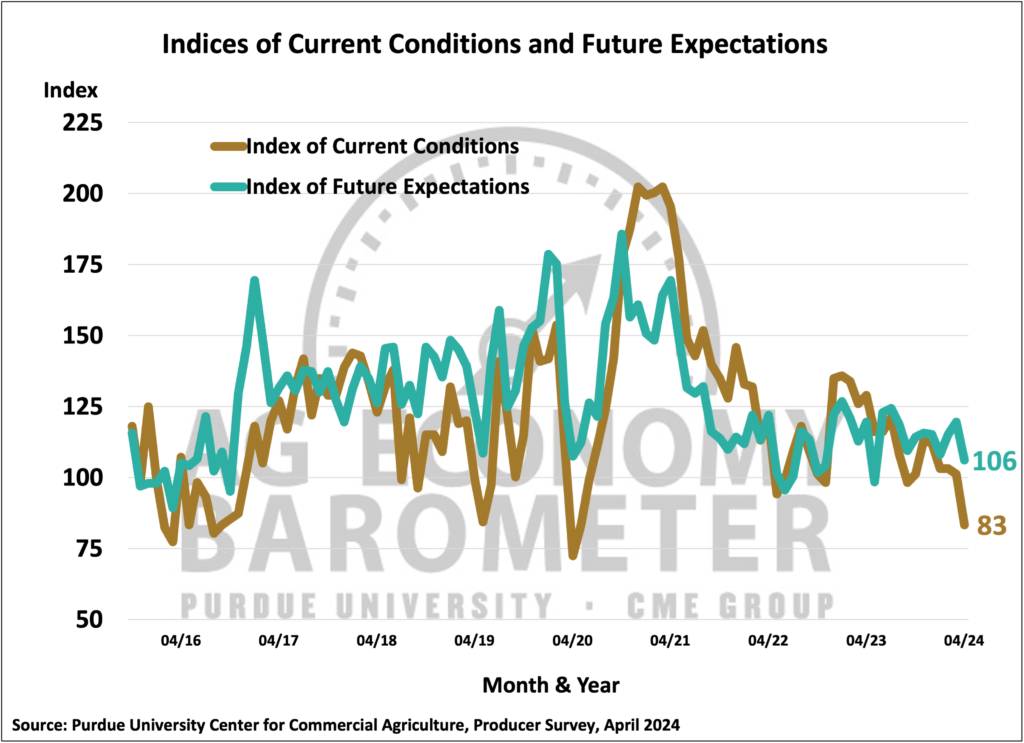

Farmer sentiment plunged in April as the Purdue University-CME Group Ag Economy Barometer fell 15 points below a month earlier to a reading of 99. The barometer’s sub-indices both declined from a month earlier, with the Current Condition Index at 83, down 18 points, and the Future Expectations Index at 106, down 14 points. This was the weakest farmer sentiment reading since June 2022 and the lowest current condition rating since May 2020. Concerns about their farms’ current financial situation and expectations for weak financial performance in the year ahead were the driving forces behind the fall-off in farmer sentiment. The April Ag Economy Barometer survey was conducted from April 8-12, 2024.

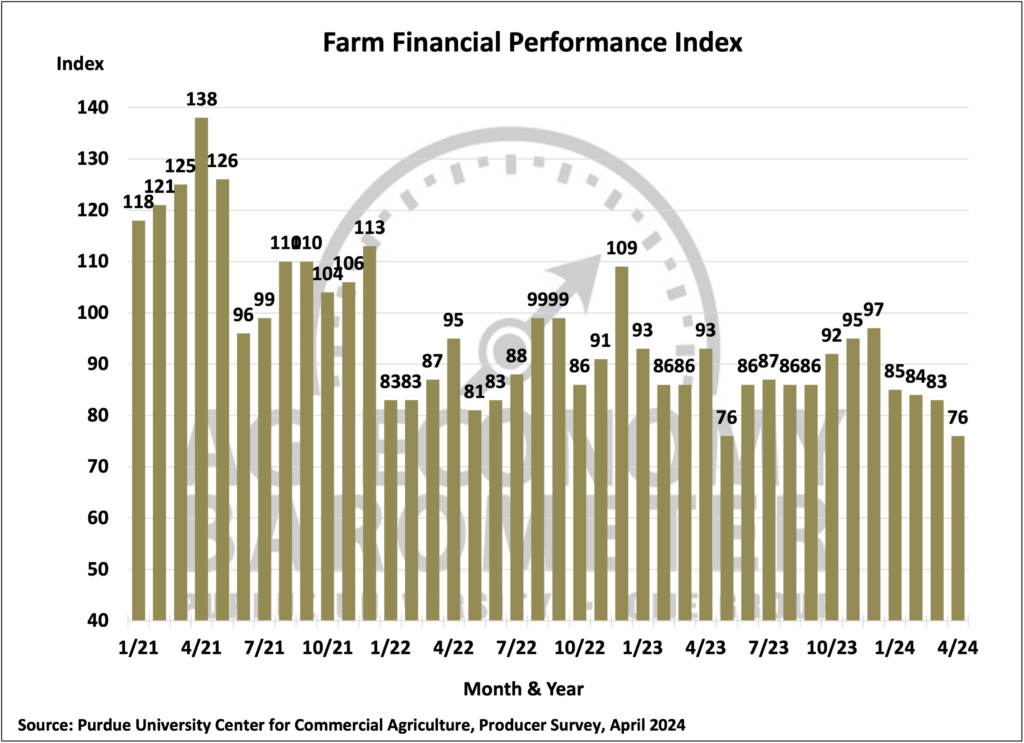

The Farm Financial Performance Index fell to 76 in April, 7 points lower than a month earlier and 21 points lower than last fall’s peak of 97. The financial index is based upon a question that asks farmers if they expect their farms’ financial performance to be better than, worse than, or about the same as last year. This month, fewer producers said they expected better or the same financial performance, with more respondents choosing worse performance than last year. Farmers’ expectation that 2024 will be a difficult year was a big contributor to this month’s decline in farmer sentiment.

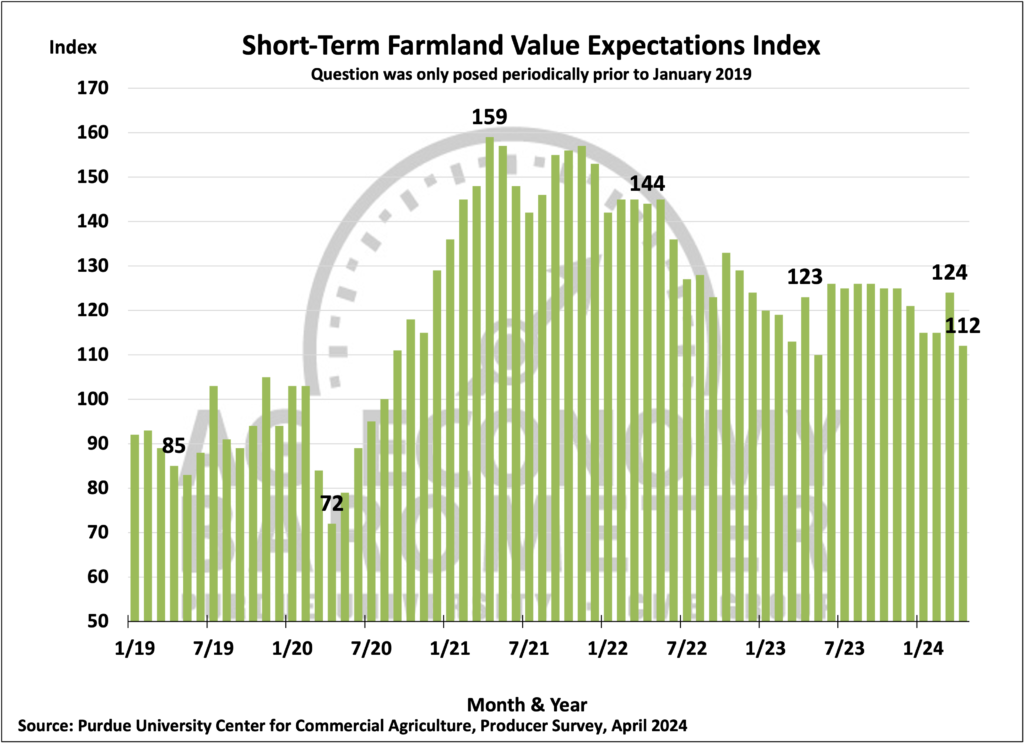

The April Short-Term Farmland Value Expectations Index reading of 112 was 12 points lower than in March, more than wiping out the rise in the index that took place in March. The percentage of producers who expect farmland values in their area to rise over the next 12 months dipped to just 29% from 38% in March, while more respondents said they expect values to remain unchanged in the upcoming year. Concerns about farm financial performance in 2024 this month outweighed farmers’ more optimistic view regarding future interest rate changes. In April, just 24% of respondents said they look for interest rates to rise over the next year, down from 32% of farmers who felt that way in March.

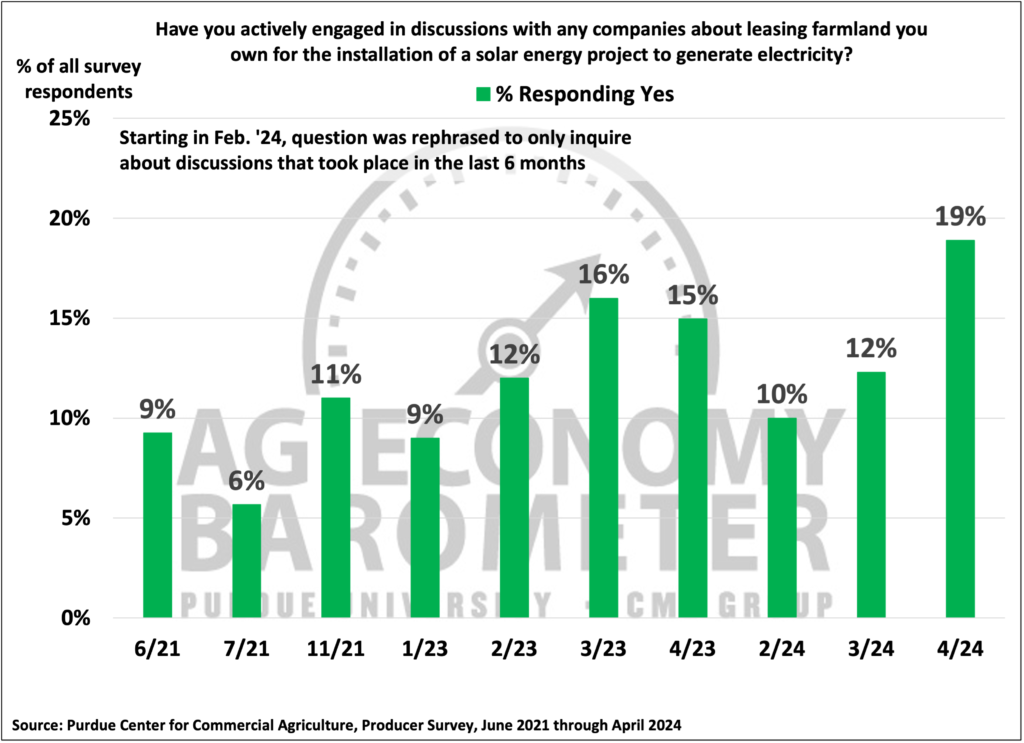

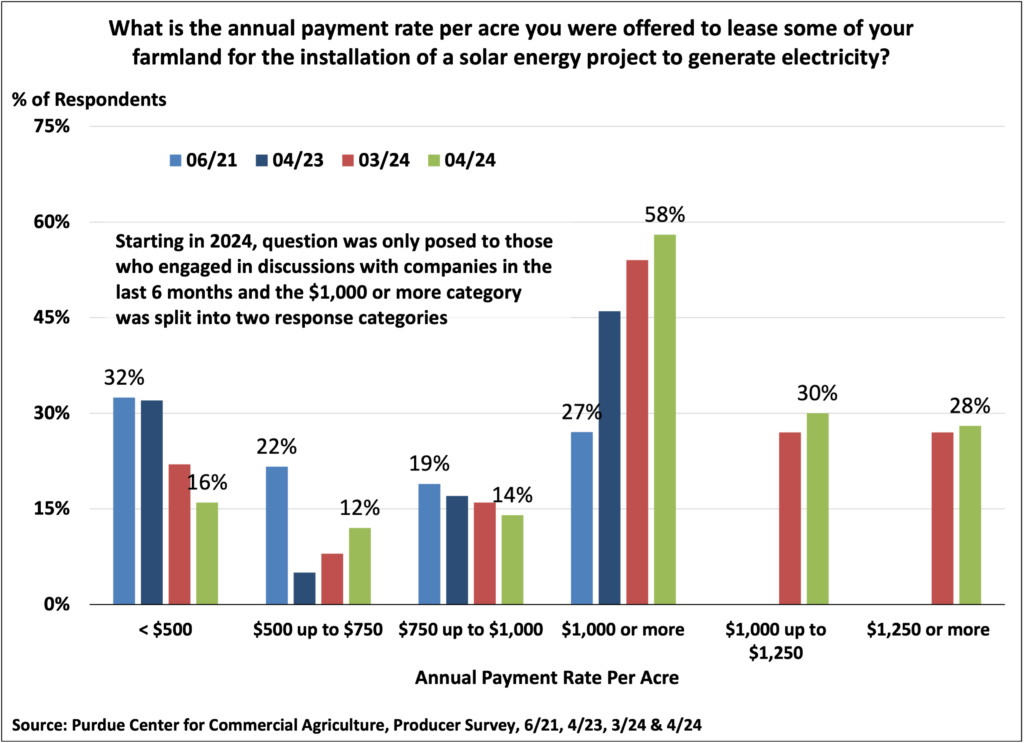

This month’s survey again included questions about leasing farmland for solar energy production. There was a noticeable uptick in the percentage of respondents who reported a discussion with a company in the last 6 months about leasing farmland for solar energy production. In April, that percentage rose 7 points to 19% of respondents, up from 12% in March. The April survey’s question related to farmland values in the next 12 months included a new response category: energy production. Although most (60%) producers continued to point to non-farm investor demand as the key reason for their optimism about farmland values, 8% of this month’s respondents cited energy production, such as wind, solar, or carbon capture usage, as an important reason. Farmers who reported discussing solar leasing with a company were also asked about the annual lease rates they were offered. Fifty-eight percent of them reported a lease rate offer of over $1,000 per acre, up from 54% in the March survey. For the last two months, the solar lease rate question provided an additional breakout of the over $1,000 per acre category. Thirty percent of respondents in April said the lease rate they were offered ranged between $1,000 and $1,250 per acre, while 28% of farmers said they were offered $1,250 or more per acre. These results suggest that lease rates being offered for energy production could provide some support for farmland values and farmland value expectations.

Wrapping Up

Farmer sentiment weakened sharply in April as the Ag Economy Barometer fell 15 points to its lowest reading since June 2022. Farmers’ appraisal of their current situation and outlook for the upcoming year were much weaker than last month as both the Current Conditions and Future Expectations Indices suffered large declines in April. Farmers said they expect weaker financial performance compared to a year earlier, even though fewer farmers look for interest rates to rise than just a month earlier. Weaker sentiment also translated into a less optimistic view of farmland values as fewer farmers said they looked for farmland values to rise over the next 12 months. One factor that could be providing support for farmland values in some locales is energy production. Nineteen percent of respondents to this month’s survey reported discussing leasing farmland for solar energy production with a company, and 8% of farmers who look for farmland values to rise in the upcoming year pointed to energy production on farmland as a supporting factor.