Farmer Sentiment Improves Despite Financial Performance Concerns

James Mintert and Michael Langemeier, Purdue Center for Commercial Agriculture

A breakdown on the Purdue/CME Group Ag Economy Barometer July results can be viewed at https://purdue.ag/barometervideo. Find the audio podcast discussion for insight on this month’s sentiment at https://purdue.ag/agcast.

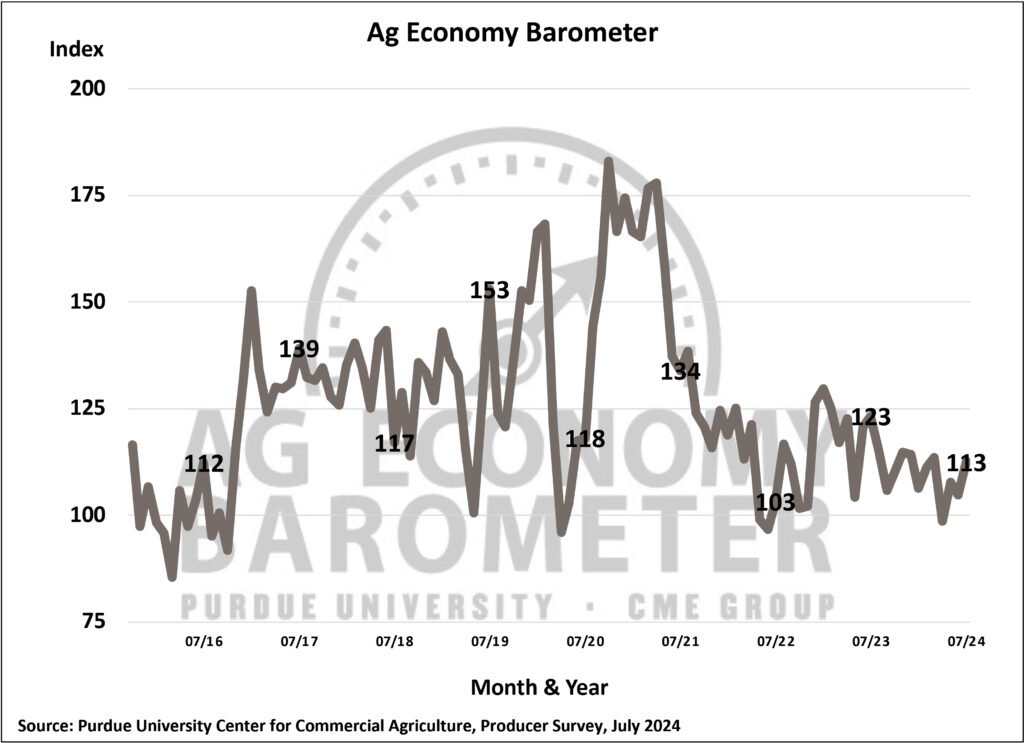

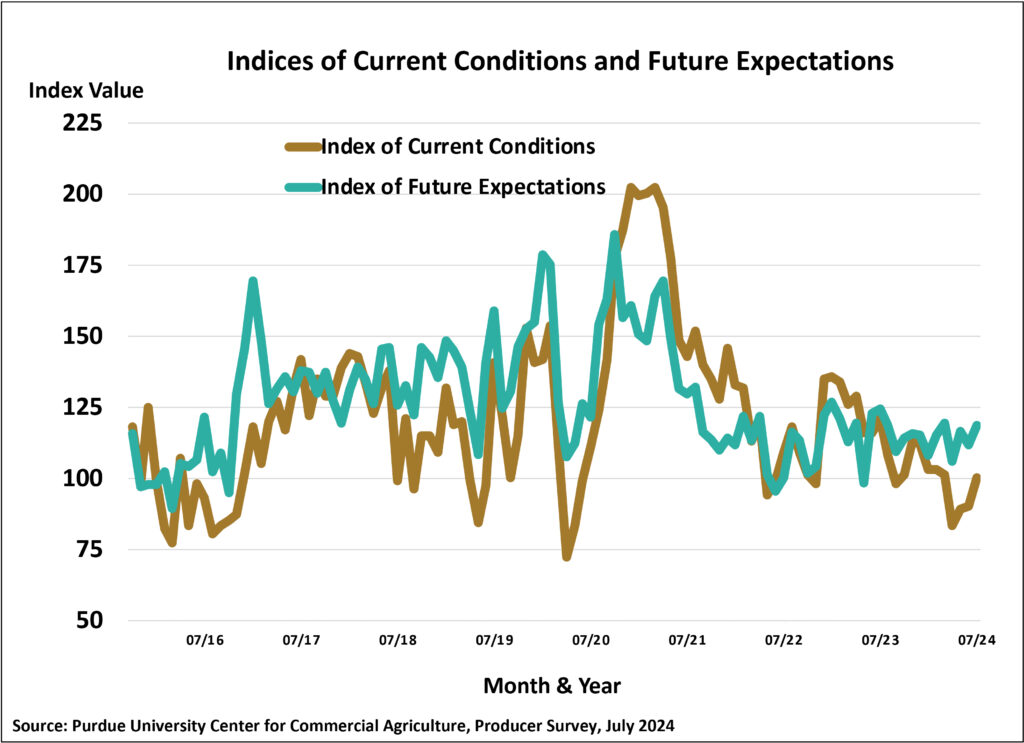

All three broad-based measures of farmer sentiment improved in July. The Purdue University-CME Group Ag Economy Barometer Index rose 8 points to 113. At the same time, the Index of Current Conditions increased by 10 points to 100, and the Index of Future Expectations at 119 was 7 points higher than a month earlier. July’s sentiment improvement occurred even though prices for both corn and soybeans declined from the time survey responses were collected in June to July. For example, Eastern Corn Belt cash prices for corn and soybeans declined 11% and 5%, respectively, from mid-June to mid-July. Responses to the individual questions used to calculate the indices indicated that the sentiment shift was primarily attributable to fewer respondents saying that 1) conditions were worse than a year earlier and 2) fewer saying that they expect bad times in the future. Data collection for the July survey took place from July 15-19, 2024, which coincided with the dates for the Republican National Convention held in Milwaukee.

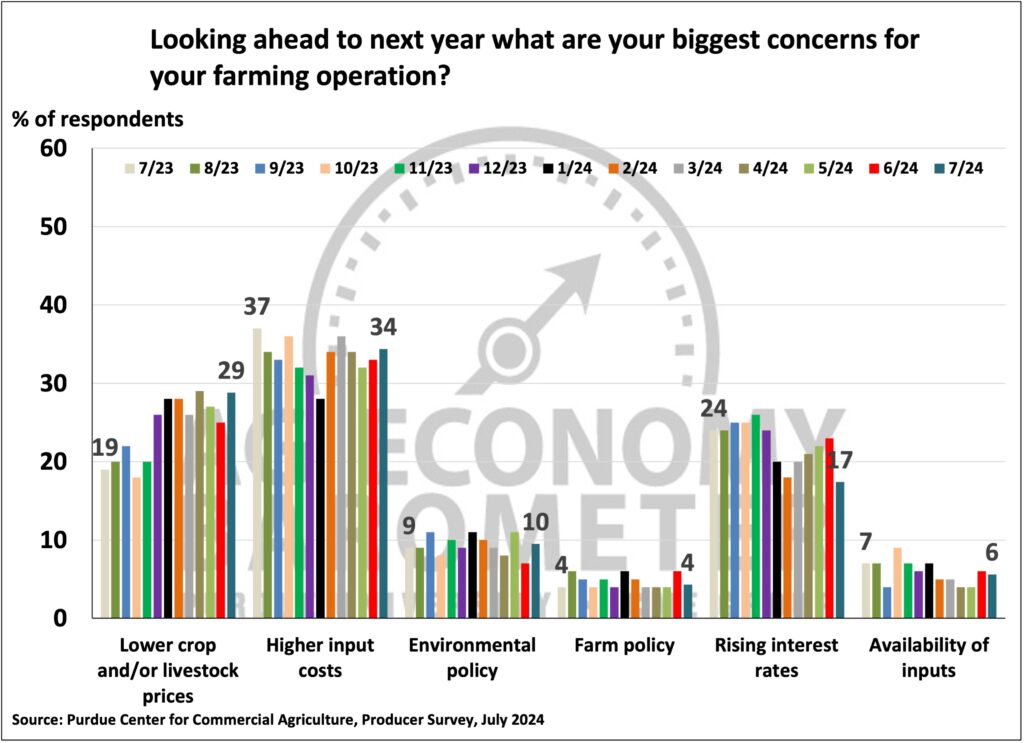

When asked about their biggest concerns in the year ahead, the top choice among producers once again was high input costs, chosen by 34% of respondents. However, weak commodity prices were also on producers’ minds, as 29% of producers in the July survey pointed to the risk of lower crop and livestock prices as a top concern, up from 25% of respondents in June. Only 17% of respondents cited rising interest rates as a top concern, down from 23% in June, consistent with signals from the Fed that interest rates have peaked.

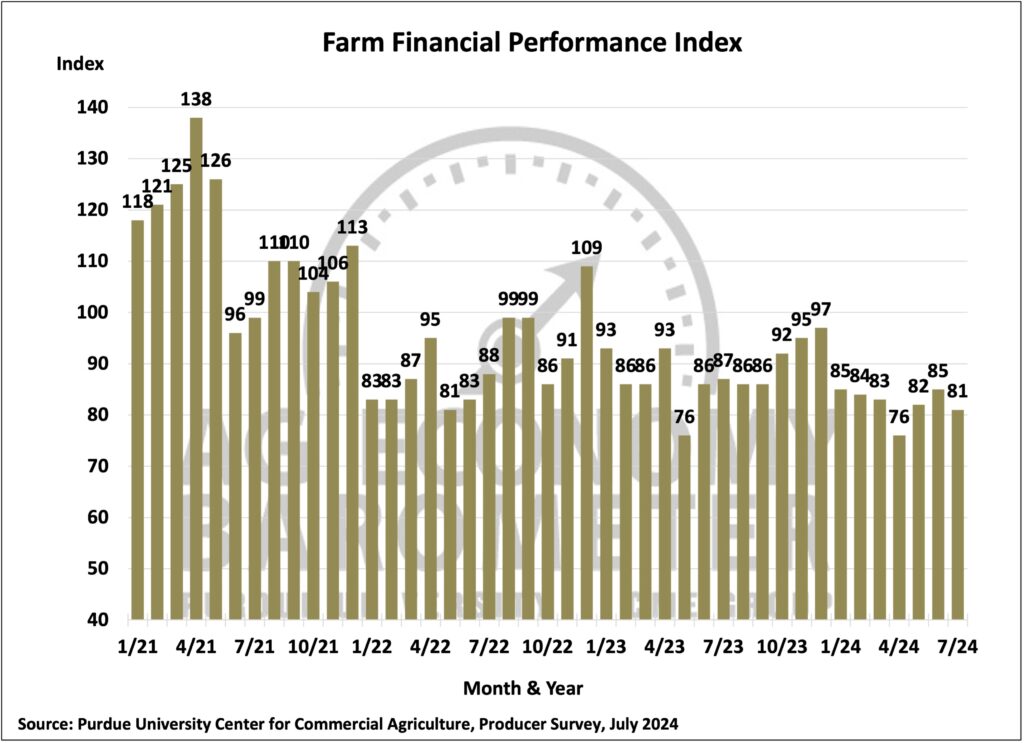

The Farm Financial Performance Index weakened by 4 points in July to 81, leaving the index 6 points lower than a year earlier. July’s decline followed back-to-back improvements in the index in May and June. The index’s fall reflects farmers’ concerns about the impact of weakening commodity prices combined with high input prices. Although the cost of production for principal crops, including corn and soybeans, has fallen year-to-year, output prices have declined even more, raising the possibility of a cost-price squeeze for U.S. crop producers.

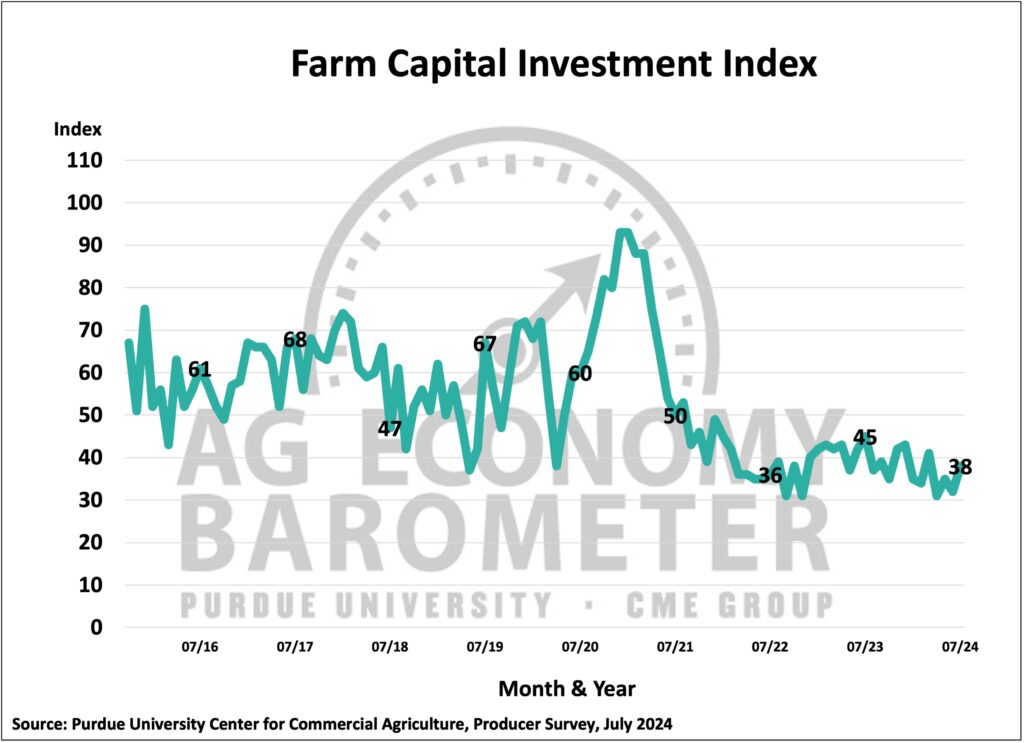

Despite the weakness in producers’ perspectives on their farm’s financial performance, the Farm Capital Investment Index rose 6 points in July to 38. Although the index rose above June’s reading, it remains in very weak territory as it was still 7 points lower than in July 2023. This month’s improvement in the index was primarily attributable to a modest shift in the percentage of producers who said it was a bad time to make large investments. In July, 75% of survey respondents said it was a bad time to invest, down from 80% who felt that way in June. The shift in perspective coincided with fewer producers citing interest rates as a top concern for the upcoming year.

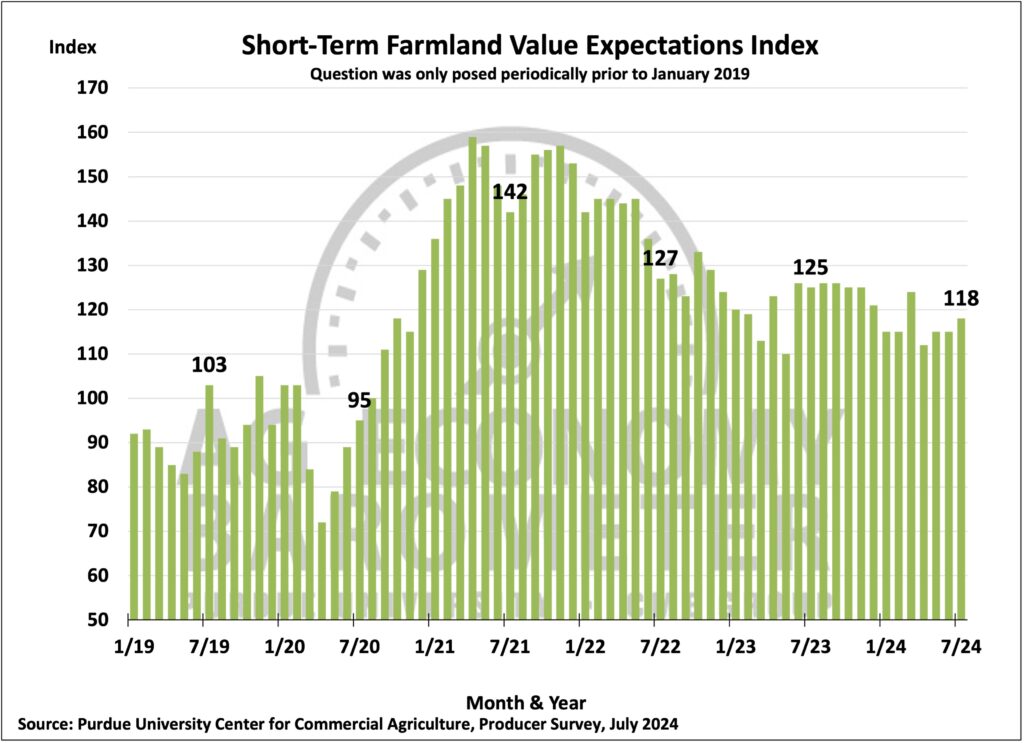

There was a small improvement in July’s Short-Term Farmland Value Expectations Index, which rose to 118, up from 115 in June. The small sentiment shift was attributable to more respondents saying they expect farmland values over the next year to stay the same, with fewer farmers saying they expect values to rise or fall. The long-term index weakened in July to 146, 6 points lower than in June. The change in the long-term index came about because fewer respondents said they expect to see values rise over the next five years, while more farmers said they expect values to remain unchanged.

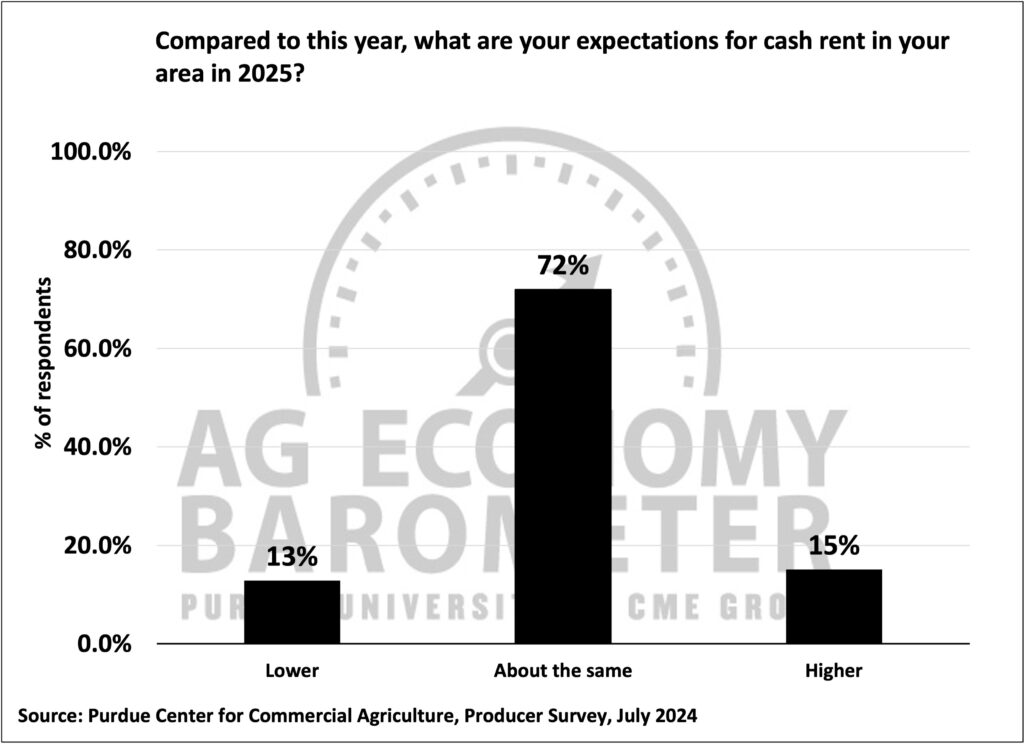

Farmland leasing discussions for the 2025 crop year are starting to take place across the nation. This month’s survey asked farmers who grow corn, soybeans, wheat, or cotton what their expectations are for cash rental rates in their area. Nearly three-fourths (72%) of farmers who responded to the July survey said they expect cash rental rates to remain about the same as in 2024. The remaining respondents’ views on cash rental rates were split almost evenly between those who expect rates to rise (15%) vs. those who expect rates to fall (13%).

Wrapping Up

The broad measure of farmer sentiment, the Ag Economy Barometer, climbed 8 points above the June reading as producers’ perspectives on both current conditions and the future improved. The sentiment improvement was puzzling in part because prices for principal commodities weakened from mid-June to mid-July, which could be expected to reduce farmers’ income. In contrast to the sentiment improvement, producers confirmed that their farms’ financial condition was weaker than a year ago. Looking ahead, producers continue to express concerns about high input costs and declining prices for crops and livestock. Producers in July were somewhat less concerned about the impact of interest rates on their farm operations, and that could be a reason why their outlook on capital investments improved modestly. Despite this month’s improvement in their investment perspective, farmers’ outlook on capital expenditures remained weak from both a long-term perspective and compared to a year ago. Finally, looking ahead to 2025, nearly three-fourths of crop farmers in this month’s survey said they expect farmland cash rental rates to remain about the same as in 2024.