Farmer sentiment rises as income prospects improve, concerns about key policy issues remain

James Mintert and Michael Langemeier, Purdue Center for Commercial Agriculture

A breakdown on the Purdue/CME Group Ag Economy Barometer December results can be viewed at https://purdue.ag/barometervideo. Find the audio podcast discussion for insight on this month’s sentiment at https://purdue.ag/agcast.

Download report (pdf)

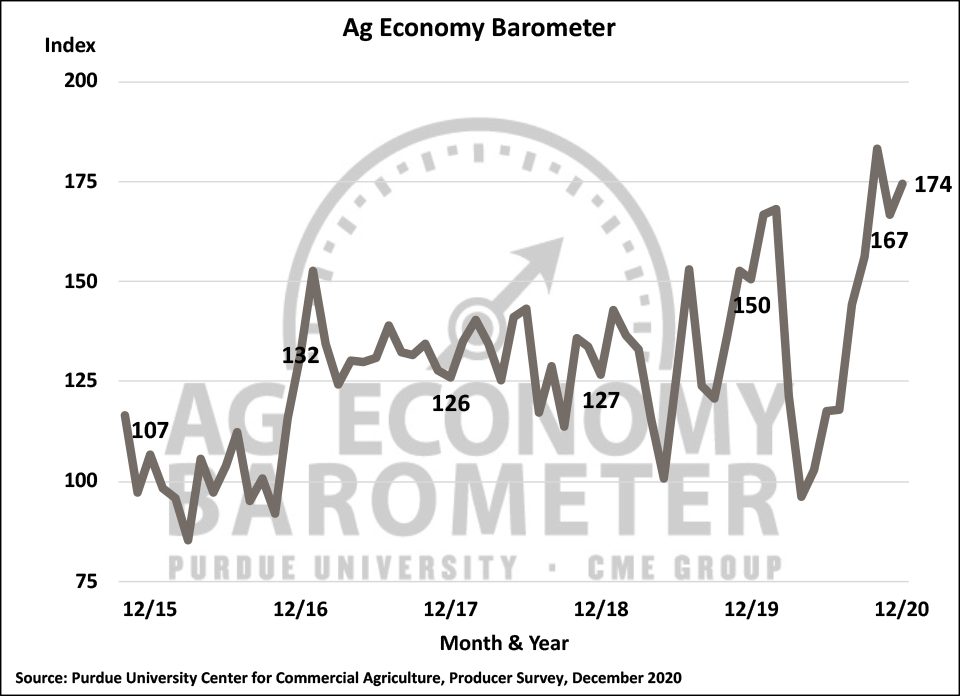

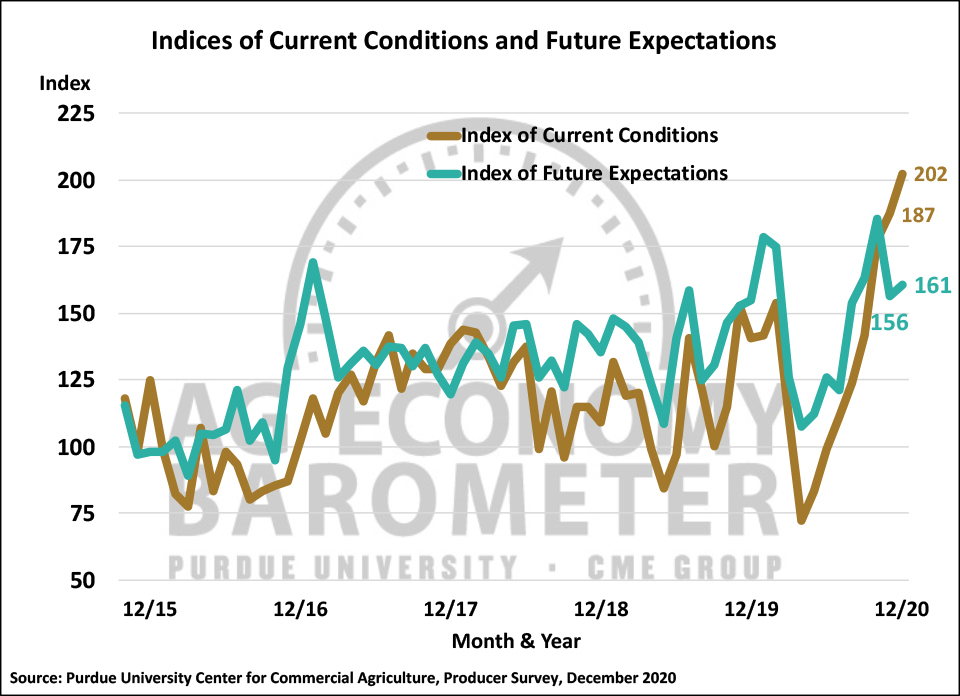

Farmer sentiment improved modestly in December as the Ag Economy Barometer rose to a reading of 174, up 7 points from November. December’s sentiment improvement still left the barometer 9 points lower than in October. Both of the barometer’s sub-indices, the Index of Current Conditions and the Index of Future Expectations, were higher in December than in November although the current conditions improvement was three-times the size of the future expectations increase. The Index of Current Conditions climbed 15 points to 202 whereas the Index of Future Expectations increased by just 5 points to a reading of 161. The farm income boost provided by the ongoing rally in crop prices appears to be the driving force behind the improvement in the Current Conditions Index and the overall improvement in farmer sentiment. The Ag Economy Barometer is calculated each month from 400 U.S. agricultural producers’ responses to a telephone survey. This month’s survey was conducted from December 7-11, 2020.

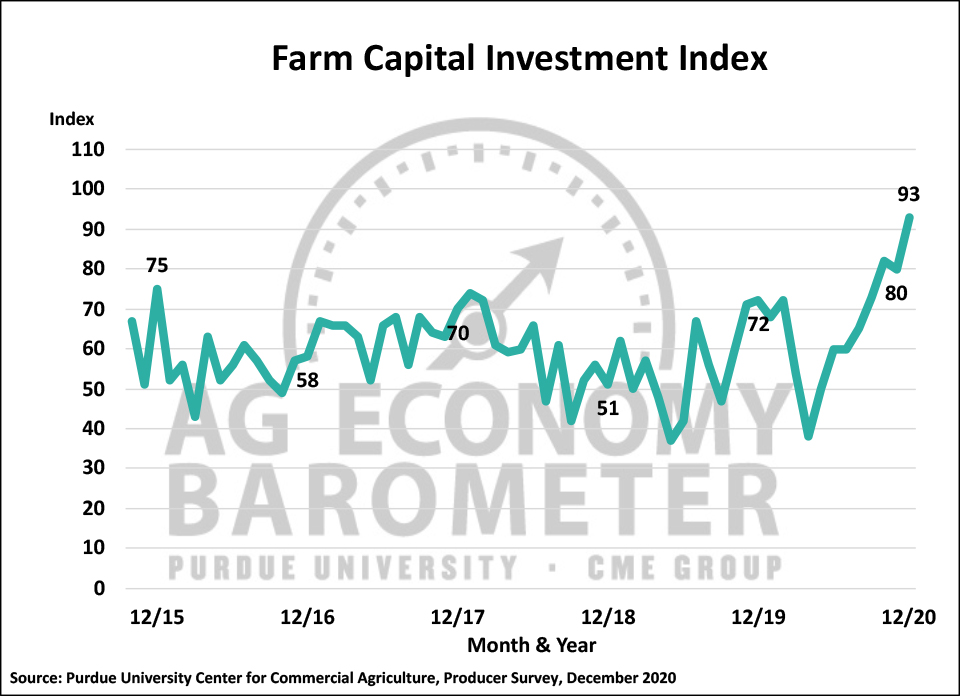

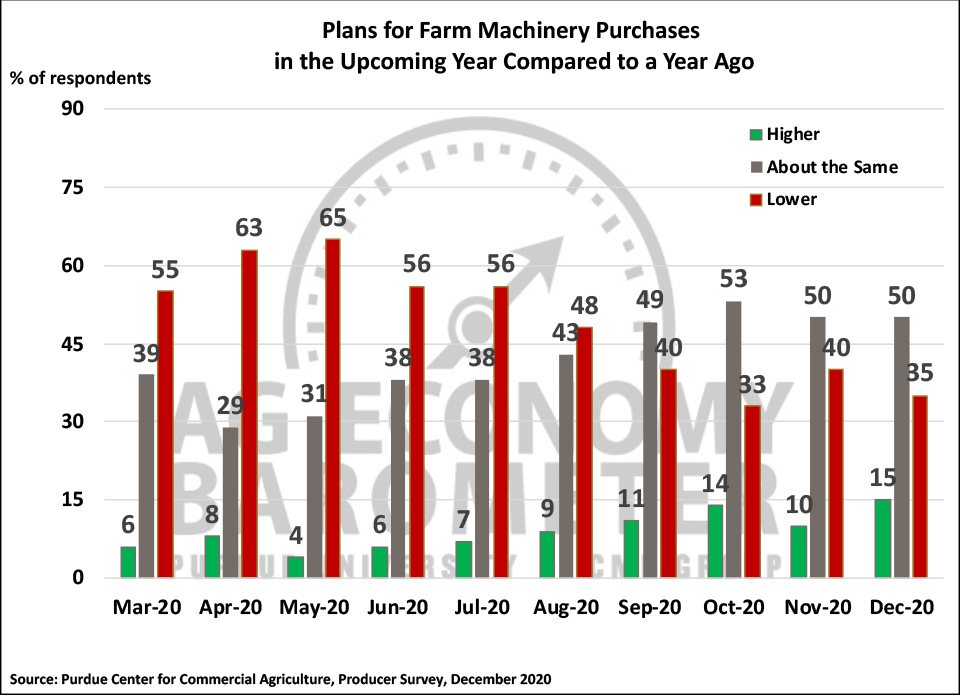

Producers were noticeably more inclined to think now is a good time to make large investments in their farming operations than in November. The Farm Capital Investment Index increased 13 points in December to a record high 93. The comparison is even more dramatic when December’s reading is compared to earlier in the year. December’s investment index reading was 28 points higher than back in August, when the crop price rally was just getting underway in earnest, and it is more than double the April reading of 38. When asked more specifically about their plans for farm machinery purchases, the percentage of farmers expecting to increase their machinery purchases in the upcoming year rose 5 points to 15 percent in December, while the percentage expecting to reduce their purchases declined by the same amount.

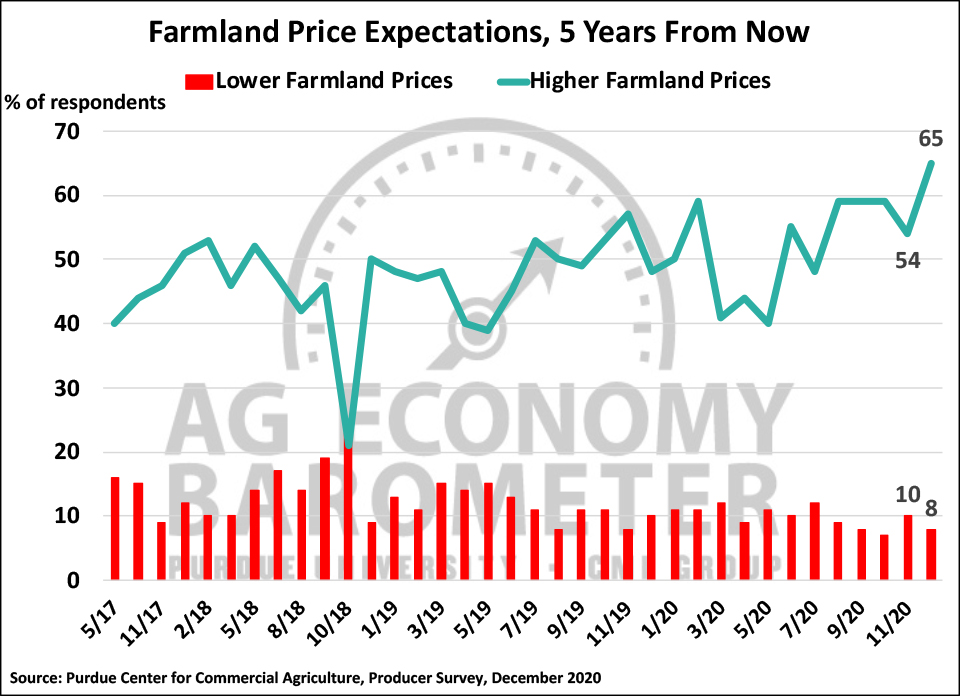

The improvement in farmer’s sentiment was reflected in a noticeably more bullish perspective on farmland values. In December, producers were more optimistic that farmland values will rise over both the short-term (12 months) and longer-term (5 years) than in November and even more so when compared to farmland value expectations from earlier in the year. The percentage of farmers expecting farmland values to rise over the next year increased to 35, up from 26 percent a month earlier. Producers were even more optimistic regarding their longer-run perspective on farmland values with a life of survey high 65 percent of farmers saying they expect farmland values to rise over the next five years, which was 11 points higher than in November.

The December survey also included a question regarding producers’ expectations for farmland cash rental rates in 2021 compared to 2020. In December, 18 percent of respondents said they expected cash rental rates to rise in 2021, which was double the percentage who felt that way in August and September, but was 20 points lower than in October, the last time this question was posed. The sentiment shift from October to December was primarily the result of a shift towards expecting rates to remain about the same as in 2020. Examining responses from August through December, it’s clear that downward pressure on cash rental rates has largely evaporated. In August, 17 percent of respondents said they expected cash rental rates to decline, whereas in December, just 5 percent of farmers in our survey said they expected to see lower rental rates in the upcoming year.

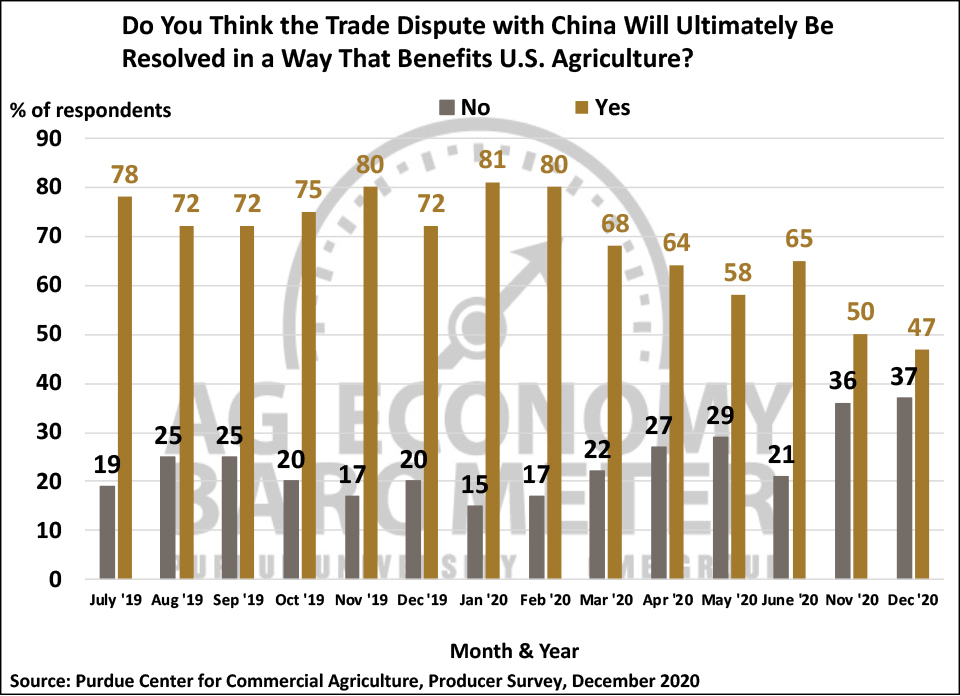

U.S. exports to China have increased substantially in recent months, especially for corn and soybeans. In turn, the rise in exports has been key to the improvement in crop prices. Despite that, producers have become less optimistic that the trade dispute with China will be resolved in a way that’s beneficial to U.S. agriculture. For example, in the first quarter of 2020 an average of 76 percent of respondents thought the trade dispute’s ultimate resolution would favor U.S. agriculture. In the spring quarter, that average declined to 62 percent and in December it fell further, to just 47 percent.

Producers also became somewhat less optimistic about U.S. agriculture’s trade prospects as year-end approached. In the three-month period from August through October, an average of 63 percent of farmers in our survey said they expected U.S. ag exports to increase over the next five years. However, ag trade expectations were less optimistic in November and December with an average of just 52 percent of respondents expecting to see growth in U.S. ag exports over the upcoming five years.

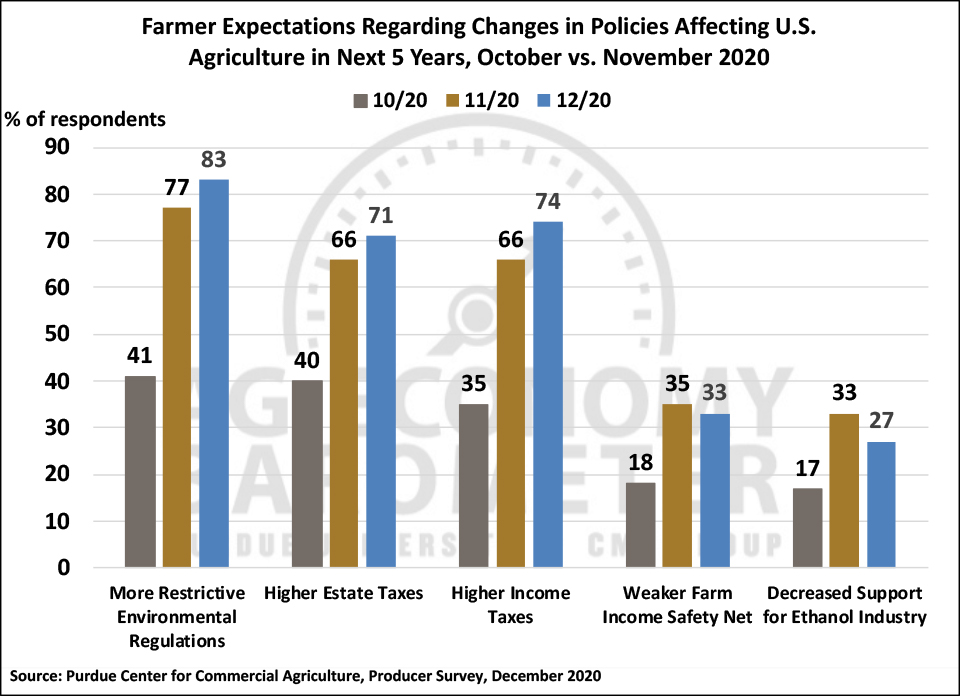

On the December survey, farmers continued to express concerns following the November election about several key policy issues affecting agriculture. Over 80 percent of farmers in the December survey said they expect environmental regulations to become more restrictive, compared to 41 percent who felt that way in October. Over 70 percent of producers expect to see higher income and estate taxes compared to 35 and 40 percent, respectively, who felt that way in October. One-third of farmers said they expect the farm income safety net to weaken compared to 18 percent who felt that way in October and just over one-fourth of producers said they expect government support for the ethanol industry to weaken compared to 17 percent who felt that way in October.

Wrapping Up

Farmer sentiment improved modestly in December, primarily as a result of farmer’s perception that current conditions on their farming operations improved compared to a month earlier. Although the Ag Economy Barometer rose in December, it remained 9 points below its October reading. Producers this month were markedly more inclined to say this is a good time to make large investments in their farming operation than a month earlier, as the Farm Capital Investment rose 13 points to a life of survey high reading of 93. Their optimism was also reflected in their expectations for farmland values as the percentage of farmers who expect farmland values to rise over the next five years rose to a record high of 65 percent. Comparing survey results from before the November election to the post-election time frame, there continues to be less optimism following the election about future ag exports and more concerns about increasing environmental regulations and prospects for higher taxes. Additionally, the percentage of producers concerned that the farm income safety net will weaken remained higher post-election than before the election, as did the percentage of farmers expecting government support for the ethanol industry to decline.