Weakening Commodity Cast A Shadow On Farmer Sentiment

James Mintert and Michael Langemeier, Purdue Center for Commercial Agriculture

A breakdown on the Purdue/CME Group Ag Economy Barometer January results can be viewed at https://purdue.ag/barometervideo. Find the audio podcast discussion for insight on this month’s sentiment at https://purdue.ag/agcast.

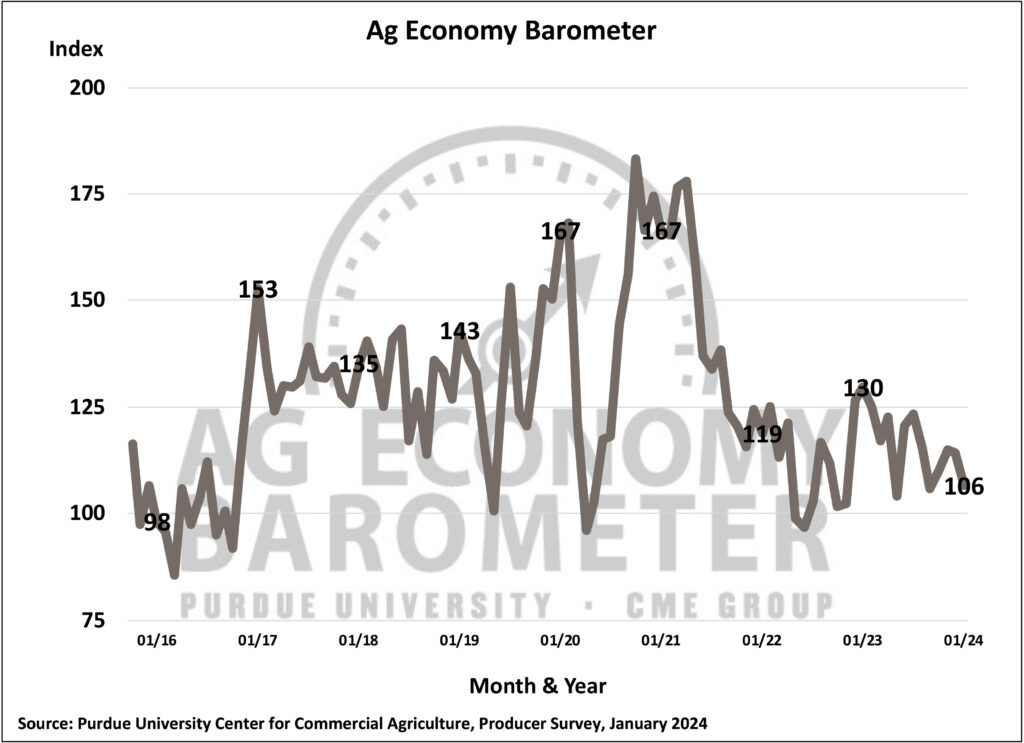

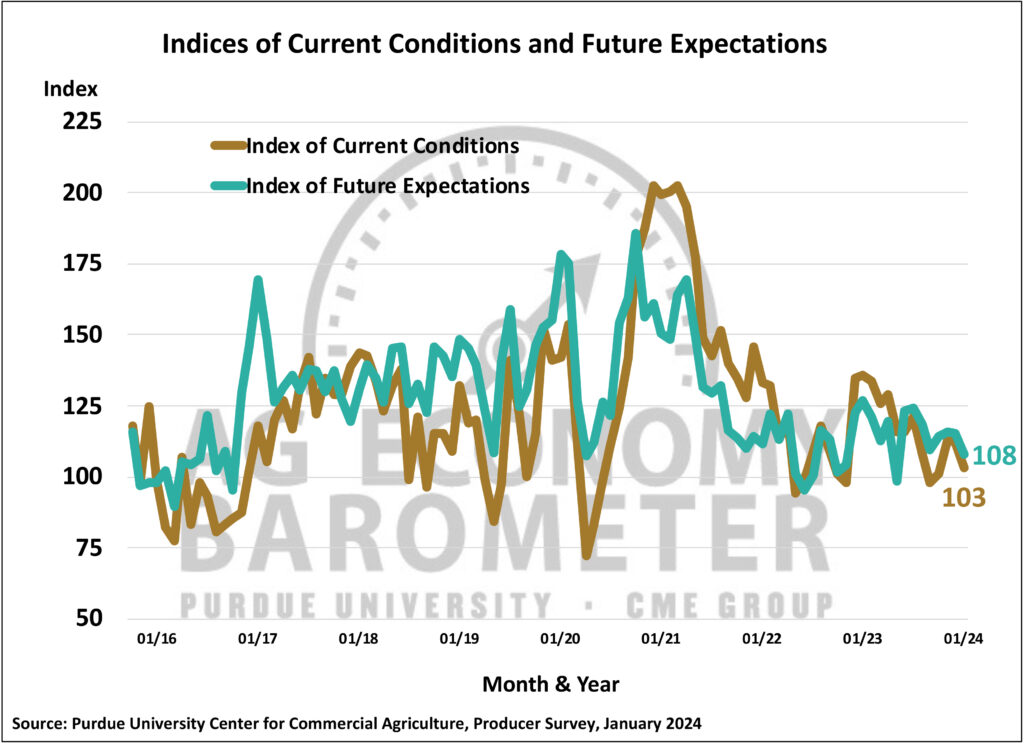

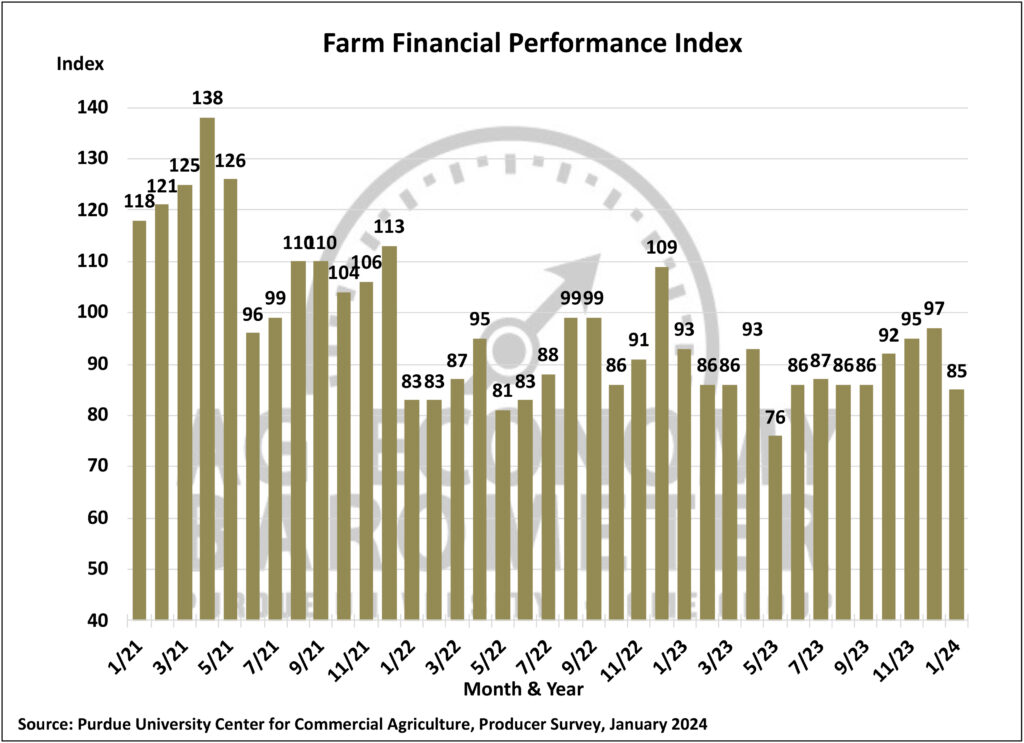

Farmer sentiment took a downturn at the start of 2024 as the January Purdue University-CME Group Ag Economy Barometer Index fell to a reading of 106, 8 points below a month earlier. Compared to year-end, producers had a more negative outlook of their farms’ current situation along with a weakened outlook for the future as the Current Conditions Index fell 9 points and the Future Expectations Index dropped 7 points, both compared to December. Anticipated lower farm income in 2024 significantly influenced the decline across all indices, evident in the Farm Financial Performance Index registering at 85, which was 12 points lower than a month earlier. The January Ag Economy Barometer survey was conducted from January 15-19, 2024.

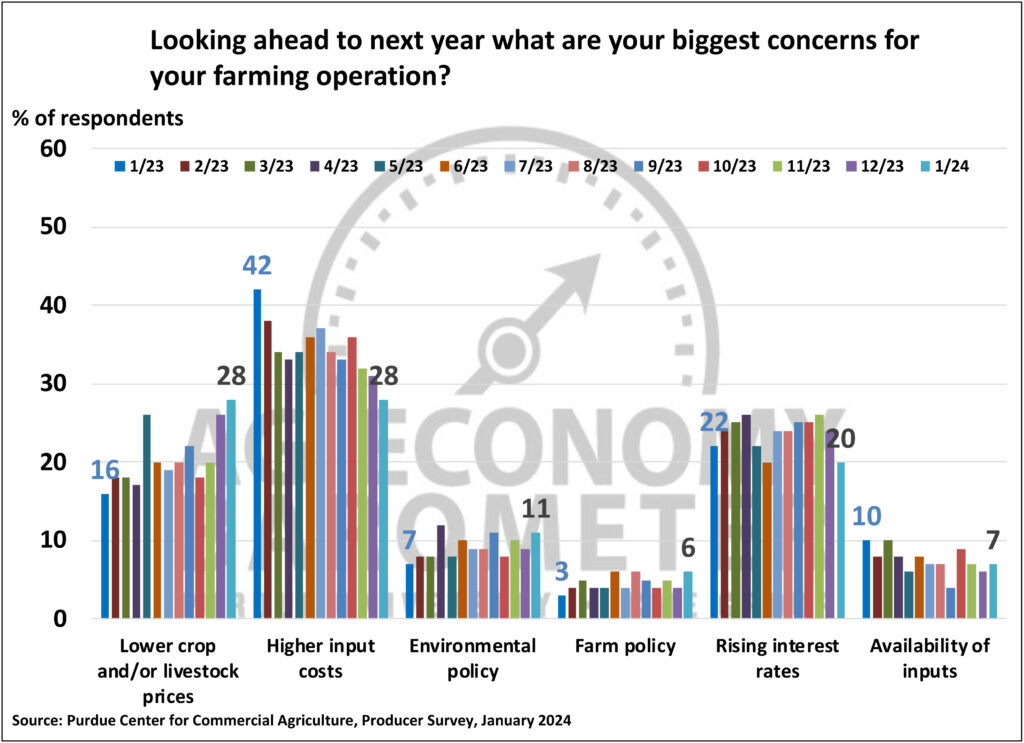

After strengthening during the last half of 2023, the Farm Financial Performance Index recorded its weakest reading since May 2023. The 7-point decline from December to January was primarily driven by a shift in expectations, moving away from anticipating income to remain steady in the upcoming year as it was in 2023, towards expecting income to weaken. The percentage of producers expecting weaker financial performance rose from 20% in December to 31% in January, while those expecting incomes to be about the same fell from 63% to 53%. In a related question, producers expressed two key reasons for farm financial performance to weaken in the year ahead. More producers this month cited lower crop and/or livestock prices as top concerns than at any point since January of last year when the question about upcoming year concerns was first introduced in a barometer survey. For the first time, the percentage of producers choosing lower crop/livestock prices (28%) matched the percentage of producers who chose higher input costs. This alignment indicates that U.S. farmers are worried about a possible cost/price squeeze leading to lower farm incomes.

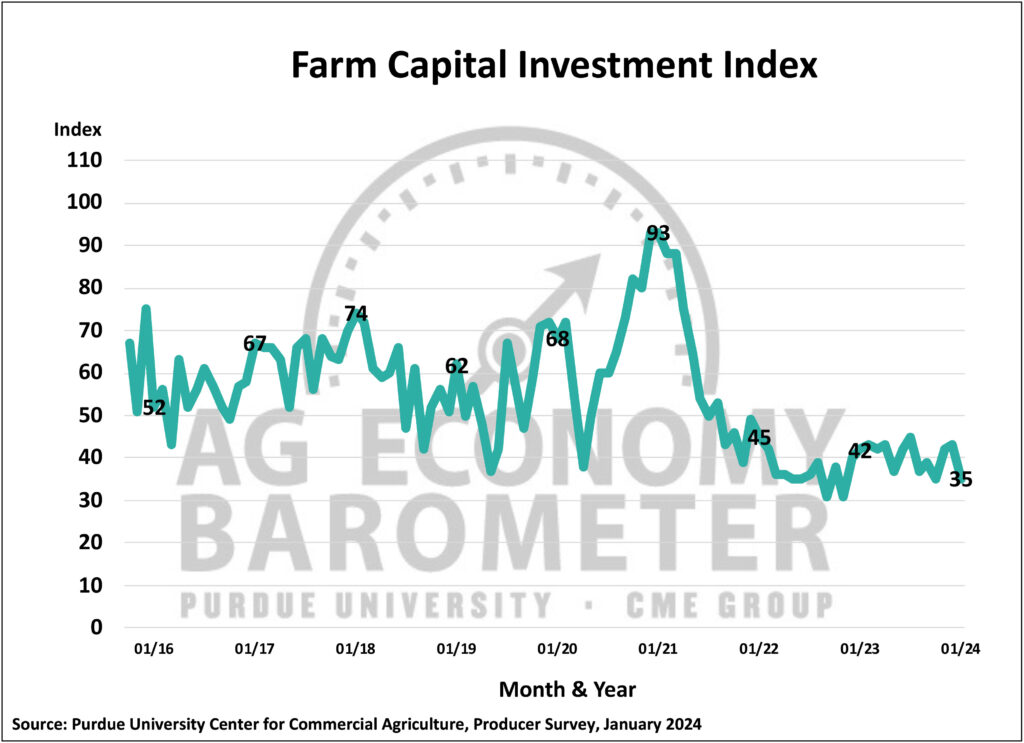

Unsurprisingly, given producers’ concern about farm incomes, the Farm Capital Investment Index fell to 35, 8 points lower than in December. Fewer producers who think now is a bad time to make large investments attributed rising interest rates as the reason this month, reversing a trend evident throughout much of 2023 when concerns about higher interest rates were increasing. This month more farmers pointed to high prices for machinery and construction as a reason to hold off on making investments. Among producers who think now is a good time for large investments, more producers this month pointed to their farms’ expansion opportunities while fewer farmers cited the increase in dealers’ farm machinery inventories as a reason to invest.

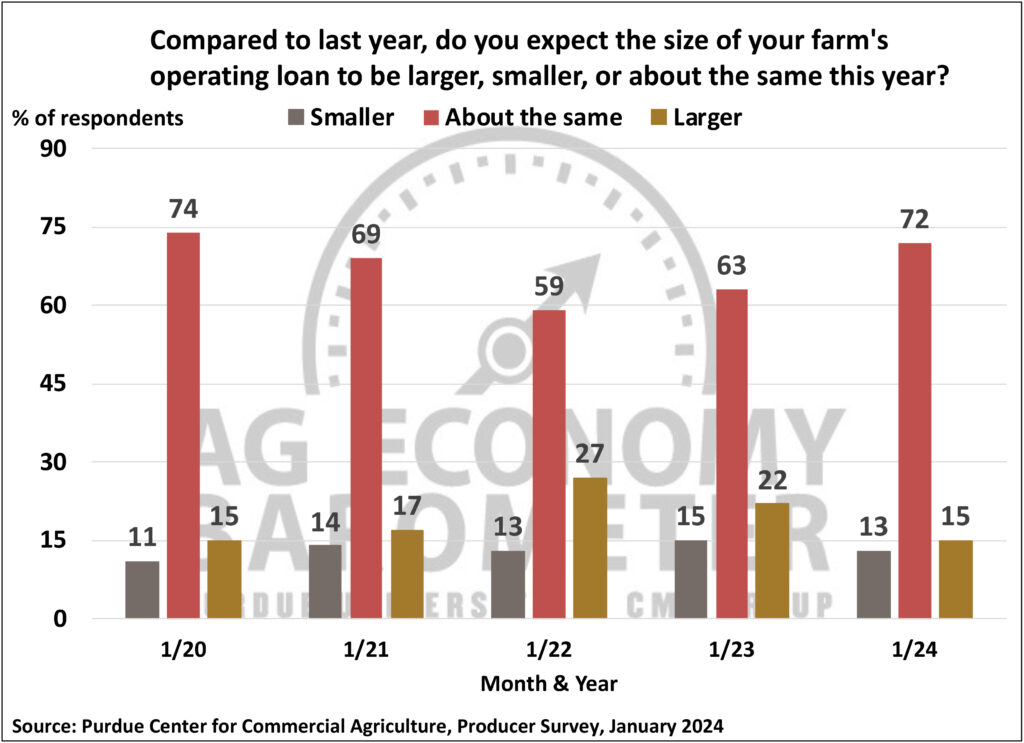

Starting in 2020, the January survey has asked producers if they expect their farm’s operating loan in the upcoming year to be larger, about the same or smaller than the previous year. This year, more producers said they expect their operating loan to be about the same as last year while fewer producers said they expect to have a larger operating loan. Among producers anticipating a larger operating loan, 61% said it was because of an increase in input costs, down from 80% who pointed to high input costs last year. This year, 23% of respondents said their loan size rose due to their farm’s expansion, up from 15% in 2023.

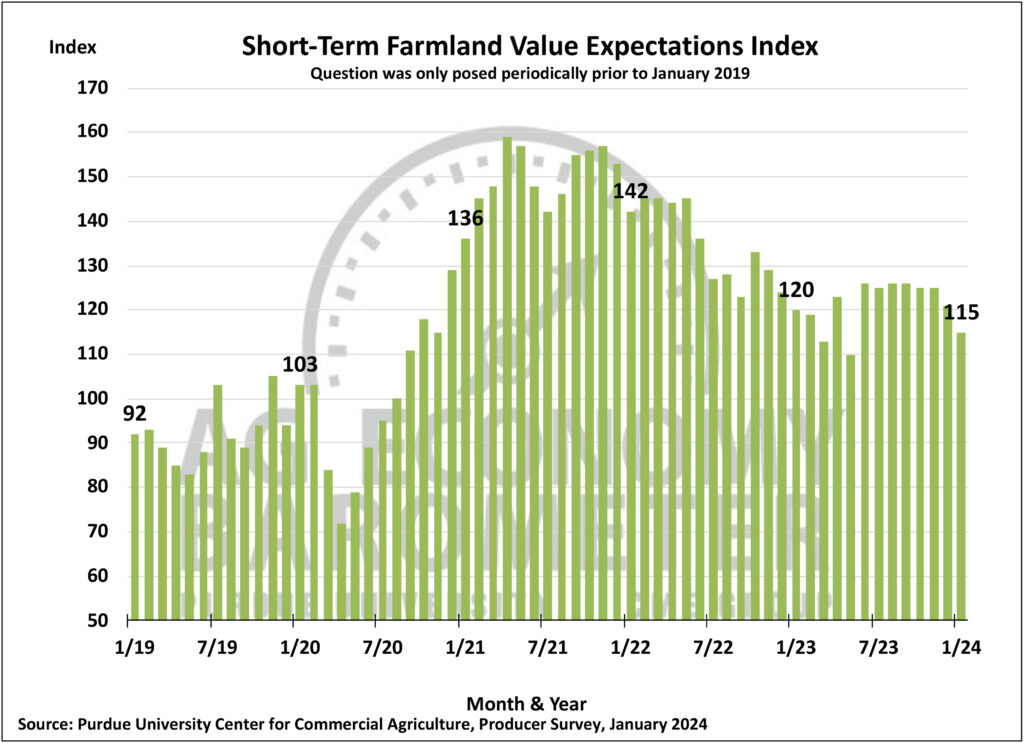

The Short-Term Farmland Value Expectations Index dropped to 115, 6 points lower than in December, while the long-term index remained virtually unchanged at 150. Since the index was still above 100, it indicates that more producers in the survey expect farmland values to rise in the upcoming year compared to those expecting values to decline. However, digging into the survey responses used to compute the short-term index reveals an interesting trend. The proportion of producers anticipating a decline in this year’s farmland values in their area rose to 16% in January, up from the 10% who felt that way as recently as October. At the same time, the percentage of producers expecting higher farmland values fell from 35% to 31%. When corn-soybean growers were asked about farmland cash rental rates in 2024 vs. 2023, results were similar to those obtained last summer. Just over one-fifth of respondents (22%) expect rates to rise while a large majority (72%) expect no change in cash rental rates. Among those who expect to see rental rates rise, nearly half (46%) expect cash rental rates to rise less than 5%.

Starting in 2021, barometer surveys have periodically included questions about payments for capturing carbon. In this month’s survey, 8% of respondents said they have engaged in discussions about carbon capture. Reviewing nine barometer surveys conducted in 2021, 2022 and 2023 that included this question, the percentage of producers who discussed carbon contracts with a company ranged from a low of 2.6% to a high of 9%, suggesting relatively consistent interest among producers in this regard. A majority of producers (61%) who reported discussions with companies this month said they were offered a payment rate of less than $10 per metric ton, while 12% of respondents were offered a rate of $30 or more per ton.

Wrapping Up

Declining prices for key commodities weighed on agricultural producer sentiment in January. The percentage of producers citing lower prices for crops and livestock as a top issue this month matched the percentage indicating input prices as a top concern. Previously, the response “higher input prices” was consistently chosen by producers as their top concern. The combination of high input costs and declining commodity prices generated a weaker financial performance outlook for 2024 and a weaker capital investment index. When asked to compare their farms’ operating loan size in 2024 to 2023, fewer producers than a year ago expected a larger loan. Among those anticipating an increase in loan size, fewer farms attributed it to rising input costs with more farms pointing to an increase in their operation’s size as a key reason.