Balancing Business and Financial Risk

Total risk can be divided into two major categories: business risk and financial risk. Business risk involves the variability of the farm’s return to assets. Business risk arises from variability in production levels (e.g., yield variability), output prices (e.g., corn price variability), and input prices (e.g., fertilizer price variability), as well as changes in legal aspects of the business and personnel. Financial risk arises from the financial claims of the farm’s creditors. Financial risk is caused by uncertainty pertaining to interest rates, lending relationships, changes in market value of assets used as collateral, and changes in cash flow used to repay debt. With the relatively high crop net returns experienced from 2007 to 2013, for many farms, financial risk was not a large concern. Under the current environment in which crop net returns are relatively low, financial risk is becoming a much larger issue. In this article, case farms are used to examine the relationship between business, financial, and total risk, and to illustrate what happens to each of these risks when interest rates and leverage change.

Business risk and financial risk combine to determine total risk in a multiplicative way:

(1) Total Risk = Business Risk x Financial Risk

Business risk is expressed as the coefficient of variation of returns on the farm’s assets (i.e., standard deviation of return on assets divided by average return on assets). Financial risk is a function of the farm’s leverage position, and most importantly the difference between the farm’s return on assets and the interest rate on debt. Financial risk increases dramatically if a farm has a high debt to asset ratio, and a small positive gap or a negative gap between its return on asset and the interest rate.

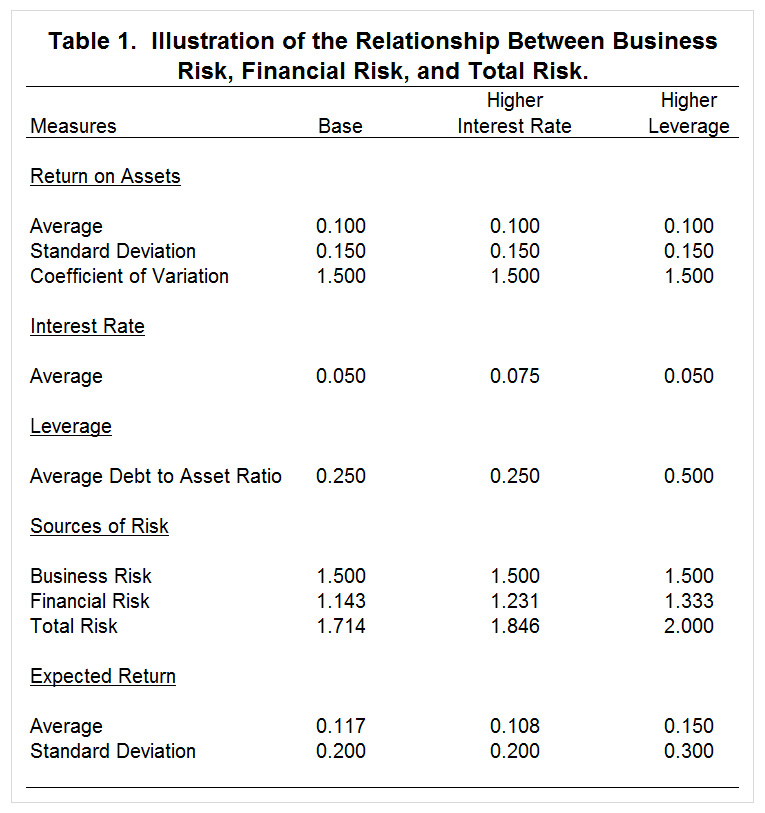

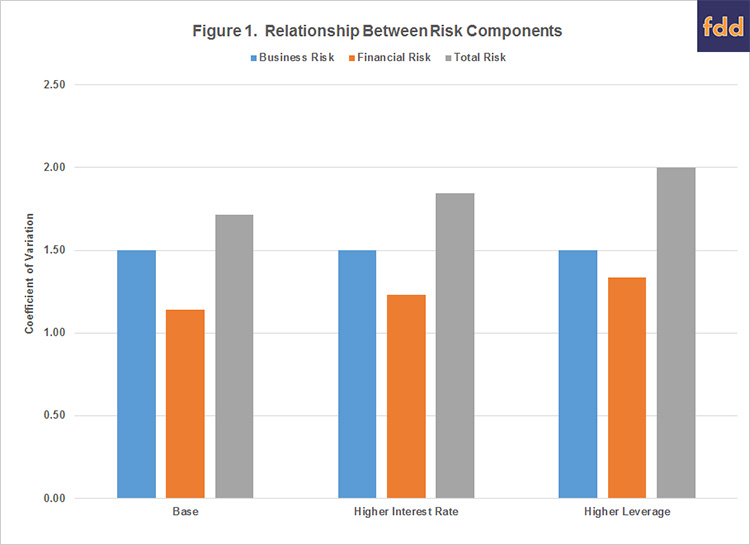

Table 1 illustrates the relationship between business risk, financial risk, and total risk for a base case, a case with a higher interest rate, and case with higher leverage. For all three scenarios, the return on assets is higher than the interest rate, thus we would expect leverage to increase return on equity or expected return. This can be seen by comparing the first and second columns with the third column. The first and second column assume a debt to asset ratio of 0.25 while the third column assumes a debt to asset ratio of 0.50. Expected return is higher in the third column or the scenario with a higher debt to asset ratio. Turning to an examination of risk, business risk is the same for all three scenarios. Financial risk increases with increases in either the interest rate or leverage. The increase in financial risk for the higher interest rate and higher leverage scenarios, results in an increase in total risk. The relationship between total risk, business risk, and financial risk is illustrated graphically in Figure 1.

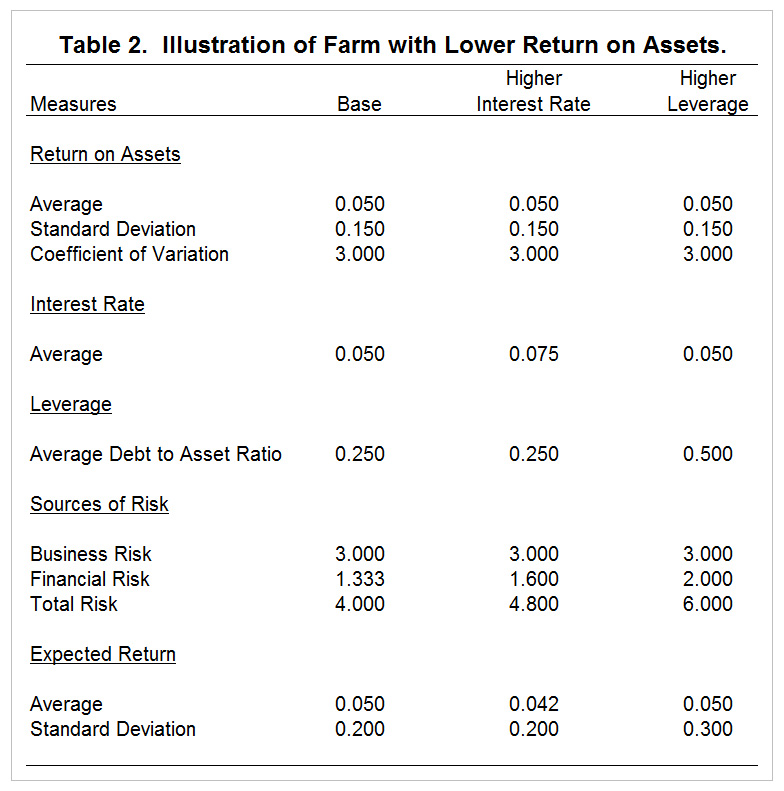

Table 2 uses the same scenarios as depicted in table 1, but uses a lower return on assets. It is extremely important for farms to examine the relationship between the return on assets on their farm and the interest rate. If return on assets is greater than the interest rate, borrowing increases the return on equity or expected return. Conversely, if return on assets is less than the interest rate, borrow lowers expected return. In this instance, return on assets for the base case and the higher leverage scenario is the same as the interest rate. Thus, return on assets is the same as expected return. For the higher interest rate scenario, return on assets is less than the interest rate. Thus, expected return is lower than the return on assets for the higher interest rate scenario. Business risk is the same for the each of the scenarios depicted in table 1. However, financial risk and total risk increase with increases in the interest rate or leverage.

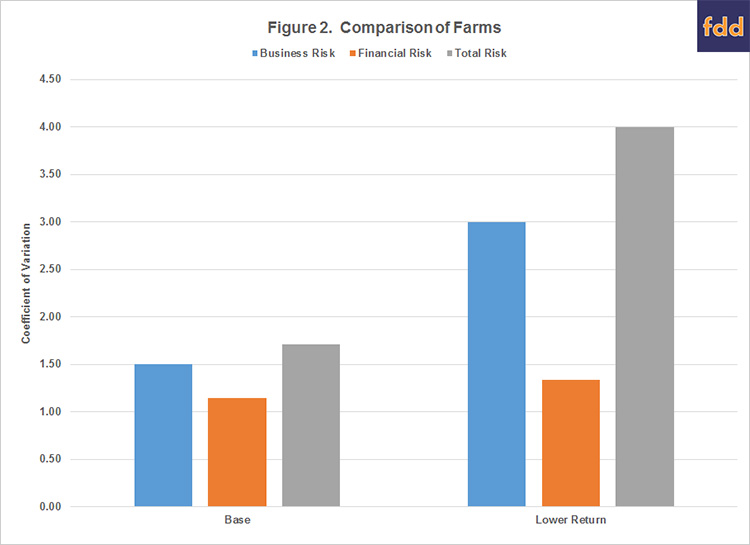

Figure 2 compares business risk, financial risk, and total risk for the base case in table 1 and the lower return scenario in table 2. The farm with the lower return faces much higher risk. In particular, total risk for the farm with the lower return is more than twice as high as total risk for the case farm depicted in table 1. This fact stresses the importance of management. In general, unless they do something to mitigate risk, such as diversifying or using less leverage, farms with lower returns face more risk.

This article discussed the relationship between business risk, financial risk, and total risk; and examined the impact of a change in interest rate and leverage on each risk component. More information on the relationship between business risk, financial risk, and total risk can be found in Barry and Ellinger (2012). As illustrated in this article, increasing interest rates and leverage increased financial risk and total risk. To keep total risk from increasing in response to a change in interest rates or leverage, business risk has to be adjusted. For example, a farm facing more financial risk could diversify, or use crop insurance.

Reference

Barry, P.J. and P.N. Ellinger. Financial Management in Agriculture, Seventh Edition.