Income Tax Aspects of the Taxpayers Relief Act of 1997

November 18, 1997

PAER-1997-08

George F. Patrick, Professor

![]()

![]()

![]()

![]()

![]()

Introduction

Tax cuts and a balanced budget were negotiated by President Clinton and Congress in the Taxpayer Relief Act of 1997 (TRA ‘97). However, political realities resulted in many of the tax cuts only occurring several years in the future. A few provisions of the law are retroactive, some take effect in 1997, and most are phased in gradually beginning in 1998 or later years. This article provides an over-view of some of the provisions affecting agriculture as well as those affecting producers as individuals.

Agriculturally-Related Provisions

Deferred Payment Contracts – TRA ‘97 defers proceeds from deferred payment contracts for sales of crops and livestock until the year of receipt for both regular tax and alternative minimum tax (AMT) purposes. This provision applies to farmers using the cash basis method of accounting and is retroactive to tax years after 1986. In 1996, the IRS had taken the position that producers selling commodities using a deferred payment contract could defer the income from the sale until the year of receipt of the proceeds for regular tax purposes. However, the proceeds would have needed to be included as income in the year of delivery of the commodity for AMT. Later, in Notice 97-13, the IRS allowed producers to follow previous procedures for the 1996 tax year but would have required AMT income adjustments in the 1997 to 2000 tax years. TRA ‘97 eliminates the need for these adjustments. Farmers who included the proceeds from sales made in 1996 under deferred payment contracts for 1996 AMT income, or earlier years, and paid AMT should explore their refund possibilities.

Income Averaging for Farm Income – TRA ‘97 makes income averaging available to farmers for years in the 1998 to 2000 period. Producers can elect to treat part or all of their farm income as if it had been earned equally over the three preceding tax years. Farm income is defined as Schedule F, or Form 4835, income plus the income from the sale of draft, breeding and dairy animals and farm machinery and equipment, but not land, reported on Form 4797. For example, assume that a producer’s taxable income in 1995, 1996, and 1997 was $10,000 below the beginning of the 28% tax bracket and$30,000 above the beginning of the 28% tax bracket in 1998. If the producer elected to treat the $30,000 from 1998 as if it had been earned equally in the three previous tax years, then the entire $30,000 in this example would have been taxed at the 15% marginal tax rate. These income averaging provisions apply only for income tax purposes and not for self-employment tax. Only farm income, as defined above, is eligible for averaging. However, the entire taxable income of the taxpayer in the preceding years is included in the tax calculations. Although the new income averaging provisions may provide tax relief to farmers in some high income situations, because of the wide tax brackets there may be little or no tax savings for farmers with income averaging in many situations. Thus, tax planning prior to the end of the tax year should not be neglected.

Distress Sales of Livestock – TRA ‘97 expanded the relief provisions for the drought sales of livestock to floods and other weather-related conditions for sales after 1996. Because of weather-related conditions, a farmer may sell more livestock than normally would have been sold. As an exception to the general rule, reporting of the proceeds from the sale of those additional animals may be postponed for one year at the producer’s election. A Presidentially declared disaster area must exist, although the animals or the sales do not need to be located in the disaster area. However, the producer must be able to show a direct relationship between the disaster and the sale of the animals. In other weather-related situations, a producer may sell more animals than normal and replace them within two years of the year of sale. A producer may elect to postpone recognition of the gain of the livestock by reducing the basis of the replacement livestock. A Presidentially declared disaster area is not required for this provision to be used. Both of these elections are described in detail in IRS Publication 225, The Farmer’s Tax Guide, for drought situations. Similar procedures would be used for other weather-related conditions in 1997 and later years.

Selected Other Business Provisions – Although not just specific to agriculture, TRA ‘97 increased the self-employed health insurance premium deduction to 50% in the year 2000. The deduction continues to increase, reaching 100% of premiums for 2007 and later years. TRA ‘97 also allows the same recovery period for alternative minimum tax (AMT) depreciation as for regular tax depreciation for assets placed in service in 1999. Thus, farmers will not need to have a separate AMT depreciation schedule for assets acquired after 1998. For net operating losses (NOL) in years after 1997, the carryback period will be two years instead of the current three years, while the carryforward period will become 20 years. However, if the business NOL is attributable to losses in a Presidentially declared disaster area, the carryback period remains at three years.

Capital Gains

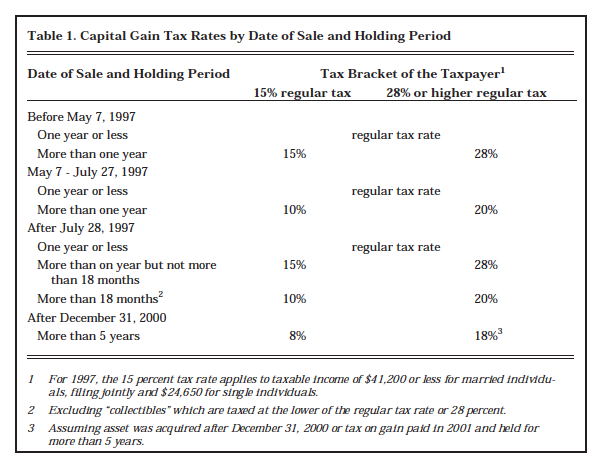

Tax rates on capital gains were generally reduced for sales after May 6, 1997. However, the tax rate on short-term capital gains, generally assets held a year or less, continues to be the individual’s regular tax rate which could be as high as 39.6 per-cent. “Mid-term” gains, assets held for more than a year but not more than 18 months and sold after July 28, 1997, are taxed at the lower of the individual’s regular tax rate or 28 percent. Long-term gains, generally for assets held for more than 18 months, are taxed at a 20 percent rate (10 percent for individuals in the 15 percent regular tax bracket). The holding period for livestock held for draft, breeding, dairy and sporting purposes to qualify to be treated as a long-term capital gain continues to be more than 12 months (more than 24 months for cattle and horses). Thus, the proceeds from a producer’s sale of a sow that had been held for 17 months would be treated as capital gain but taxed at the lower of the producer’s regular tax rate or 28 percent.

Gains on “collectibles” such as works of art, antiques, and “old iron” are taxed at the lower of the regular tax rate or 28 percent even if held for more than 18 months. A special maximum tax rate of 25 percent applies to the gains on the sale of real estate which is attributable to Section 1250 recapture. This would apply to the gain on a general purpose farm building or non-farm real estate on which straight-line depreciation had been taken. For example, if a building which originally cost $20,000 and had been depreciated to$12,500 were sold for $25,000, then the $7,500 of depreciation recapture would be taxed at the 25 percent rate and the remaining $5,000 of gain would be taxed at 20 percent. Any depreciation recapture on machinery, equipment, or other Section 1245 property is treated as ordinary income and taxed at the taxpayer’s regular income tax rate. Thus, the sale of multiple assets may involve several capital gain tax rates.

For assets held more than five years, the tax rates will be even lower beginning in 2001. For individuals in the 28 percent or higher regular tax bracket, the 20 percent capital gains tax rate drops to 18 percent for assets acquired on or after January 1, 2001 and held for five years. An asset owned on January 1, 2001 can qualify for the reduced rate if an individual pays the tax due on the gain as of the end of the year 2000 and then holds the asset for five years or more. For individuals in the 15 percent regular tax bracket, treatment is more favorable. First, the 10 percent capital gain rate drops to 8 percent for assets held for five years or more as of January 1, 2001. Second, an individual in the 15 percent regular tax bracket does not have to pay tax on the gain as of the end the year 2000 to qualify for the reduced capital gain tax rate.

The rates and holding periods are summarized in Table 1.

Table 1. Capital Gain Tax Rates by Date of Sale and Holding Period

Long-term capital losses are first used to offset long-term capital gains in the same tax rate group. If there is a net long-term capital loss in a rate group, it is used to offset gains in the next highest rate group. Any net short-term capital loss would first offset long-term capital gain from the highest rate group with remaining net loss being applied to the next highest rate. As under previous law, annual deductibility of net capital losses is limited to $3,000 for individuals.

Up to $500,000 of gain on the sale of a principal residence may be excluded from income by a married couple, filing jointly ($250,000 for single individual) for sales after May 6, 1997. In general, the home must have been the principal residence for two of the five years prior to the sale. This provision replaces the postponement of the recognition of gain if reinvested in another principal residence within a two-year period and the “once in a lifetime” exclusion of$125,000 of gain for individuals age 55 or older. However, it should be noted that the exclusion applies to gain on the sale of the personal residence and not the rest of the farm.

Child Tax Credits

For years after 1997, taxpayers with qualifying children may claim a maximum tax credit of $500 ($400 in 1998) for each qualifying child. To qualify, the child must be an individual who can be claimed as a dependency exemption by the taxpayer, is under the age of 17 at the end of the tax year of the taxpayer, and the child, stepchild, or eligible foster child of the taxpayer.

The credit is reduced $50 for each$1,000 that adjusted gross income

(AGI) exceeds $110,000 for married filing jointly, $75,000 for single, or$55,000 for married filing separately. The credit reduces income tax liability on a dollar for dollar basis. How-ever, this credit interacts with the Earned Income Credit (EIC) and there is a complex formula to deter-mine the amount of the credit and whether it is refundable.

Educational Incentives

TRA ‘97 provides several ways of reducing the cost of your or your children’s college education. In general, these programs do not start until 1998 and are subject to income limitations. Also, the provisions are mutually exclusive. Thus, taxpayers must choose which of the credits or exclusions they will use.

HOPE credit is a nonrefundable credit against federal income taxes (cannot exceed the income tax liability) of up to $1,500 per student per year. The credit applies only to the first two years of the student’s post-secondary education in a degree or certificate program. The HOPE credit is available only for the tax-payer, spouse, or individuals who may be claimed as dependents, who are pursuing a course of study on at least a half time basis, and have not been convicted of a felony drug offense. The credit is 100 percent of the first $1,000 of qualified tuition and fees, and 50 percent of the next$1,000 of such qualified expenses. Books, room, and board are not qualified educational expenses for the HOPE credit. The HOPE credit is effective for expenses paid after December 31, 1997 for academic periods beginning after that date. Because the HOPE credit can be claimed for only two tax years per student, it may be possible that not all of the expenses of the first two years of education will qualify. The HOPE credit will be phased out over the $80,000 to $100,000 modified adjusted gross income level for married couple filing jointly. The phase-out level of incomes will be adjusted for inflation beginning in 2001.

The Lifetime Learning Credit is equal to 20 percent of qualified tuition and fees incurred after June 30, 1998 on behalf of the taxpayer, tax-payer’s spouse, or dependents. For the period of June 30, 1998 to January 1, 2003, up to $5,000 of qualified expenses are eligible per taxpayer return. This increases to $10,000 for 2003 and later years. The Lifetime Learning Credit is available for any course of instruction at an eligible educational institution to acquire or improve job skills of the student. This is in addition to the type of expenses which would qualify for the HOPE credit. Like the HOPE credit, the Lifetime Learning Credit is phased out in the $80,000 to $100,000 modified adjusted gross income range for joint filers. Furthermore, the credit is not allowed on scholarships which are excluded from gross income or expenses that are deductible. For tax planning, it should be noted if the educational expense can be deducted as a business expense on Schedule F or Schedule C, the tax-savings (considering both income and self-employment taxes) will generally be larger than claiming the Lifetime Learning Credit. If the educational expense may be taken only as an itemized deduction, one should determine whether the deduction or credit provides the larger tax-savings in a year.

Special “educational IRAs” were created solely to pay qualified higher education expenses. For 1998 and later tax years, $500 annually per beneficiary under the age of 18 can be contributed to an education IRA. Only one education IRA is permitted per beneficiary. The contribution is reduced for contributors with modified adjusted gross incomes of $150,000 to $160,000 for joint returns. Distributions from an education IRA are excludable from income to the extent that they do not exceed the qualified higher educational expenditures (which are defined more broadly than for the HOPE credit) of the individual. If the education IRA has not been used for qualified educational expenses by the time the beneficiary reaches 30 years of age, it must be distributed and is subject to a 10 percent penalty tax in addition to regular income tax. However, a rollover of the education IRA from one beneficiary to another is allowed, provided the new beneficiary is a member of the family of the old beneficiary.

Distributions after 1997 from an existing retirement IRA are not subject to the 10 percent early withdrawal penalty if used to pay qualified higher educational expenses (including graduate school) of the taxpayer, taxpayer’s spouse, or any child or grandchild of the tax-payer or spouse. However, such distributions are subject to regular income tax.

Interest paid on student loans will be deductible for computing adjusted gross income after 1997. The maximum interest deduction is$1,000 in 1998, $1,500 in 1999, $2,000 in 2000 and $2,500 in 2001 and later years. The deductible amount is phased out for single individuals with income beginning at $40,000 and $60,000 for joint returns. The deduction is allowable only for interest which must be paid on a qualified educational loan during the first 60 months in which interest payments are required. The interest deduction is not allowed for an individual who may be claimed as a dependent on another taxpayer’s return.

Individual Retirement Accounts (IRAs)

The adjusted gross income (AGI) limitations for deductible contributions to IRAs are gradually increased. Currently, deductible contributions are phased out beginning at $30,000 AGI for single individuals and $50,000 for married individuals filing jointly. The lower phase-out limit will be $50,000 for single individuals by 2005 and $80,000 for joint filers by 2007. Spouses of individuals who are covered by a qualified retirement plan could not make a deductible IRA contribution under previous tax law. Deductible contributions will be allowed for 1998 and later tax years, although they are phased out for taxpayers with an AGI of more than $150,000.

“Roth IRAs” are nondeductible IRAs available in 1998 and later years. Unlike regular IRAs, contributions to a Roth IRA do not reduce income for income tax purposes when the contribution is made.

However, if invested for five years or more and distributed after the beneficiary reaches age 59 ½, then the distributions are not taxable. The maximum contribution to all IRAs, including Roth IRAs, is limited to $2,000 per year. Roth IRA contributions are phased out for joint filers with an AGI of more than $150,000 ($95,000 for single individuals). Tax-payers with an AGI of less then

$100,000 can rollover or convert an existing IRA into a Roth IRA in 1998 and the tax due can be spread over four tax years. The Roth IRA will be a very attractive investment alternative for some people.

Selected Other Provisions

TRA ‘97 has many other income as well as estate and gift tax provisions which can affect individuals and businesses. Some provisions, such as the increase in the mileage rate for charitable use of a car increase from$0.12 to $0.14 per mile, may affect a number of people but have only limited impact. At the other extreme, provisions such as the repeal of the 15 percent tax on excess distribution and excess accumulation of retirement accounts may have a very large effect on a small number of individuals.

Because of the very extensive nature of the changes being implemented by TRA ‘97, individuals are encouraged to review their tax situation carefully, both for 1997 and future tax years. Even individuals who have prepared their own tax returns may want to review their situation with a competent tax advisor.

![]()

![]()

![]()

![]()

![]()