The April 2026 CPI and PPI Reports: The Food Price Pipeline Is Opening Purchasing Power Under Pressure for Second Consecutive Month

May 18, 2026

PAERPB-2026-09

Ken Foster, Professor of Agricultural Economics and Director, Purdue Farm Policy Study Group; Bernhard Dalheimer, Assistant Professor of Macroeconomics and Trade

![]()

![]()

![]()

![]()

![]()

Key Takeaways

- – The April 2026 Consumer Price Index rose 0.6 percent on a seasonally adjusted monthly basis and 3.8 percent over the prior 12 months — the highest annual rate since May 2023, and up from 3.3 percent in March.

- – Energy remained the largest driver, rising 3.8 percent for the month and accounting for over 40 percent of the monthly increase, alongside shelter (+0.6%). The monthly energy deceleration from March’s 10.9 percent reflects partial crude oil price pullback following early ceasefire signals in April.

- – Food at home rose 0.7 percent in April after being flat in March — exactly the supply chain lag transmission our earlier briefs predicted. The food price pipeline is beginning to open, and further increases are expected over the coming months, though pre-conflict inflationary pressures from tariff pass-through and other sector-specific dynamics are also contributing.

- – Real average hourly earnings fell 0.5 percent in April, following a 0.6 percent decline in March — the first back-to-back monthly declines in purchasing power since 2023. Driven primarily by energy, this erosion compounds the regressive burden of the shock, particularly for lower-income households.

- – Several food categories reflect confounding factors beyond the Iran Conflict: avian influenza base effects, tariff pass-through, drought-reduced beef herd sizes, and global coffee supply constraints – each shape the category-level picture.

- – The April 2026 PPI, released today, confirms that energy cost pressure has now reached the industrial chemicals and packaging materials stage of the food supply chain — putting these costs approximately one to two months from food manufacturers and two to four months from retail shelves.

- – The conflict’s direct impact on farm profitability in the 2026 crop year is likely to be modest and uneven. A more significant farm-level reckoning is coming in 2027 if Strait of Hormuz restrictions persist into the fall 2026 input purchasing and spring 2027 planting cycles.

What the April CPI Report Confirms

The April CPI release is the most analytically important inflation report since the Iran Conflict began on February 28, 2026. In March’s report (Brief #2026-4), we documented the conflict’s initial footprint of a gasoline price spike triggered by a crude oil supply shock with no supply-chain lag. In the March Producer Price Index report (Brief #2026-5), we then discussed the cost pressure that was building at the wholesale level, indicating that retail food price increases were loading into the pipeline. April’s CPI report confirms both analyses, and the April PPI extends the picture forward.

Food at home rose 0.7 percent for the month — the largest monthly increase since the 2022 Russia-Ukraine shock — after being flat in March. Food manufacturers and retailers who absorbed higher energy, packaging, and logistics costs in March without passing them through have now begun adjusting prices. The adjustment is likely to continue so long as there is no resolution to high oil prices.

At the same time, the monthly energy reading decelerated from 10.9 percent in March to 3.8 percent in April. This reflects the partial pullback in crude oil prices during the CPI collection window as early diplomatic signals reduced the conflict’s near-term severity premium. The 12-month energy reading of 17.9 percent is large, but for forecasting the monthly trajectory, it matters more. If oil prices stabilize near current levels, the energy contribution to the CPI will moderate, while the food contribution accelerates. That is the shift the April data appear to show beginning to occur, although pre-conflict factors likely weigh more heavily on food items in the April CPI than conflict-driven costs. It is also worth noting that the deceleration in the monthly gasoline reading — from 21.2 percent in March to 5.4 percent in April — is arithmetically expected and does not indicate a weakening conflict impact. The Iran Conflict delivered a level shock: oil prices stepped up sharply from roughly $71 per barrel in late February to $95–118 by mid-March, and retail gasoline followed — rising approximately 40 percent nationally from roughly $2.94 per gallon before the conflict to $4.50 per gallon in April. That step up produced a very large monthly rate of change in March. April’s smaller monthly gasoline rate simply reflects the fact that prices were largely stable at the new elevated level between the two months, not that the shock has diminished. With national average gasoline prices at $4.50 per gallon and Brent crude remaining well above $100, the level effect on food supply chains is fully operational — and it is the sustained level, not the monthly rate of change, that drives the lag-based food price transmission that the coming months are expected to reveal.

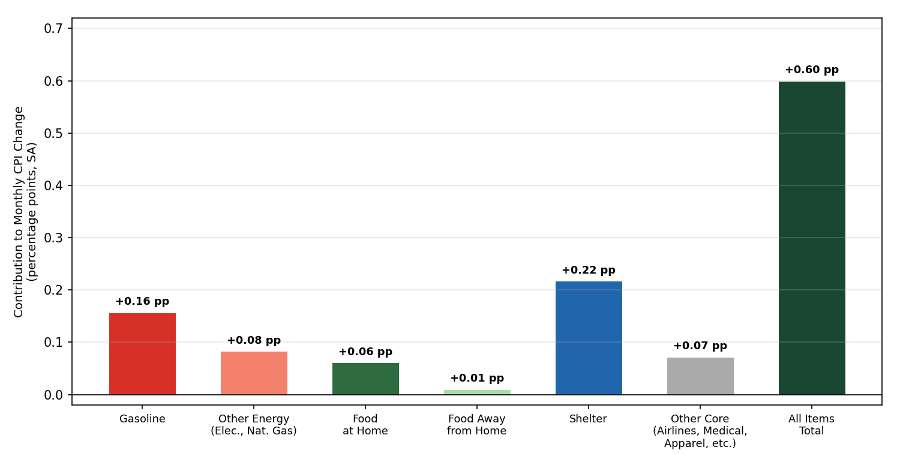

Figure 1

Decomposition of the April 2026 Monthly CPI Increase by Category

Total All-Items CPI rose 0.6 percent (SA); energy and shelter together drove over 76 percent of the monthly increase. Contributions = category weight × monthly percent change (SA). Weights and monthly changes: gasoline 2.9% weight × 5.4% monthly change = +0.16 pp; household energy 3.4% weight × ~2.4% monthly change = +0.08 pp; food at home 8.7% weight × 0.7% monthly change = +0.06 pp; food away from home 4.8% weight × 0.2% monthly change = +0.01 pp; shelter 36.2% weight × 0.6% monthly change = +0.22 pp; other core items (residual) = +0.07 pp. Source: U.S. Bureau of Labor Statistics, CPI — April 2026 (released May 12, 2026).

The Food Price Pipeline Beginning to Open

The most important development in the April CPI report for food price watchers is the 0.7 percent monthly increase in food-at-home prices — the largest single-month grocery price increase since the 2022 Russia-Ukraine shock. However, the April food-at-home increase is still mostly driven by non-conflict factors. At five to nine weeks post-conflict onset, the Iran Conflict’s energy cost channel has not yet had sufficient time to propagate through food manufacturers’ procurement contracts, packaging supply chains, and retail pricing cycles to reach grocery shelves at scale. The distributed-lag framework we documented in Brief #2026-2 projects that conflict-driven food cost pressure begins reaching retail in the three- to six-month window — and the April data, falling squarely before that window, confirm the model rather than negate it. What we are observing in April grocery prices is the accumulated pass-through of tariff-driven input cost increases that were already loading in the supply chain before February 28, combined with ongoing supply-side dynamics in beef, produce, and beverages that predate the conflict. The Iran Conflict’s contribution to retail food prices is not yet visible in the data to any great extent — but it is loading in the pipeline stages we describe below. The April food-at-home increase is the non-conflict baseline against which the conflict’s arrival at the grocery store will be measured in the months ahead. Keep in mind that prior to the conflict, USDA ERS was already predicting 3 percent food inflation for 2026.

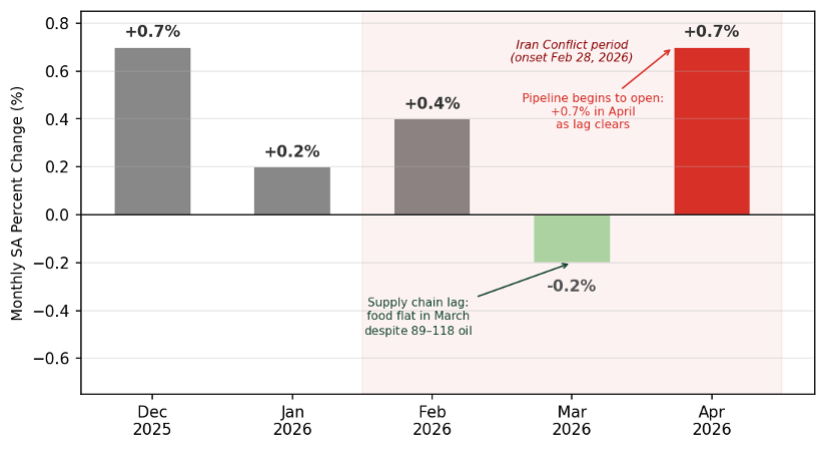

Figure 2

Food-at-Home CPI Monthly Percent Change, December 2025–April 2026

Supply chain lag now clearing: grocery prices rose 0.7 percent in April after being flat in March, consistent with the three- to six-month transmission timeline documented in Brief #2026-2. Iran Conflict onset: February 28, 2026. Seasonally adjusted monthly percent changes. Source: U.S. Bureau of Labor Statistics, CPI releases, December 2025–April 2026.

What comes next follows from the lag structure. Diesel fuel and freight costs, which rose sharply in March, are already embedded in logistics contracts that will show up in wholesale and then retail prices from May through July. Petrochemical packaging cost increases quoted to manufacturers in March and April are expected to begin reaching retail shelves by mid-summer. For seasonally stored commodities — canned goods, flour-based products, grains — the lag can extend to 12 months, meaning some categories may continue to rise even after energy prices stabilize.

One caveat deserves more emphasis. The April energy price pullback from March’s peak will reduce the ultimate magnitude of the food price pass-through relative to the worst-case scenario we modeled, if it is sustained. This is further compounded by the unresolved question of conflict duration, which is the single most important variable we identified in Brief #2026-2. If Strait of Hormuz transit restrictions ease materially in May or June, the food inflation wave will be real but shorter and shallower than a prolonged disruption would produce.

It remains important to remember that prior research shows energy price shocks only partially propagate through to retail prices because energy is a fraction of the retail food dollar.

Category-Level Analysis: Conflict Effects and Confounding Factors

The 12-month food price changes in the April report are confounded by both pre-conflict pressures and other factors. Several categories carry their own supply-side narratives that predate or operate alongside the conflict’s energy channel. Careful analysis requires separating these threads.

Fruits and Vegetables (+6.1%). This category is directly exposed to diesel-driven transportation costs — fresh produce travels by refrigerated truck from the field to the distribution center to the store, burning fuel at every leg. Due to its perishability, it is among the most immediate food-cost responders to an energy shock and likely already reflects the bulk of the transport-related price increase from the Iran Conflict in this episode. Coincidental impacts unrelated to the conflict in this category likely dominate, however. For example, the U.S. obtains approximately 70 percent of its fresh tomato imports from Mexico. In July 2025, the U.S. withdrew from the Tomato Suspension Agreement, subjecting Mexican tomatoes to tariffs, and weather-related tomato supply shortages in Mexico have driven prices even higher. Spring seasonality also contributes to this dynamic. April typically brings elevated demand and early-season supply variability for fresh produce. Domestically grown items should see some seasonal relief as the growing season progresses, though fuel costs will dampen that relief as long as oil remains elevated. Similarly, weather-related supply shocks, combined with tariffs, exert upward pressure on lime and blueberry prices.

Nonalcoholic Beverages and Beverage Materials (+5.1%). Coffee prices have been elevated for reasons substantially predating the Iran Conflict, driven primarily by Brazilian weather constraints on Arabica supply. Processing and packaging are energy-intensive for most beverage products, so the petrochemical packaging channel from the conflict compounds a pre-existing problem. Tariff pass-through is also a factor here: New York Federal Reserve research estimates that tariff pass-through to consumer prices has risen to approximately 90 percent in 2026, and beverage imports — including coffee, tea, and tropical juices — carry meaningful tariff exposure. Do not attribute this category’s inflation primarily to the Iran Conflict.

Meats, Poultry, Fish, and Eggs (+1.5%). This modest reading conceals significant underlying dynamics. Retail egg prices were 44.7 percent lower in March 2026 than in March 2025, as flock recovery from the 2024–25 Highly Pathogenic Avian Influenza outbreak proceeds. That base effect actively suppresses the 12-month reading for the entire category. Strip it out and underlying protein price inflation is materially higher. Separately, the U.S. beef herd has been contracting due to multi-year drought conditions and is slow to rebuild; import tariffs add additional pressure to domestic beef prices. Steady consumer demand against tightening supply will keep beef prices elevated regardless of energy market conditions.

Dairy and Related Products (-0.6%). Dairy is deflationary year-over-year, consistent with the joint-product dynamic we identified in our earlier work. Expanded soybean crushing for biofuel generates more soybean meal as an unavoidable co-product, reducing feed costs for dairy operations. It is worth noting, however, that dairy was up month-over-month in April, suggesting the energy cost channel may be beginning to narrow the deflationary gap and perhaps an early indication of the magnitude of this oil supply shock. Watch this category in May.

Cereals and Bakery Products (+2.6%). Grain commodity prices have remained relatively contained because Iran is not a grain exporter, and global wheat and corn supplies have not been directly disrupted. The 2.6 percent figure largely reflects ongoing labor, energy, and packaging cost pressures at the milling and baking level, not a farm-level commodity spike. Notably, flour prices have been declining for the past two months, suggesting some domestic supply expansion as retaliatory tariffs from trading partners reduce export demand for U.S. wheat and corn.

Food Away from Home (+3.6%) vs. Food at Home (+2.9%). Restaurant and foodservice prices exceeding grocery prices is the historical norm — the 20-year USDA average gap is approximately 0.9 percentage points — reflecting the higher labor intensity of foodservice. The April gap of 0.7 percentage points is actually narrower than the historical average, driven by the now-accelerating grocery-price component. The BLS definition of food away from home includes delivery and takeout meals, and delivery drivers face significantly higher gasoline costs as a direct operating expense. The 28.4 percent year-over-year gasoline price increase feeds directly and with minimal lag into delivery-based meal pricing, contributing to the foodservice number independently of restaurant input costs.

Real Earnings: The Purchasing Power Squeeze

Alongside yesterday’s CPI release, the BLS published its April Real Earnings Summary — and the results compound the consumer welfare picture significantly. Real average hourly earnings for all employees fell 0.5 percent from March to April, following a 0.6 percent decline in March. This marks the first back-to-back monthly decline in real purchasing power since 2023. Over the past 12 months, real average hourly earnings are down 0.3 percent.

Nominal wages rose 0.2 percent in April while the CPI-U rose 0.6 percent, producing a 0.4 percentage point real loss. The primary driver of the real wage erosion is energy — particularly gasoline — which inflates the price denominator without adding to workers’ nominal compensation. Food is not the dominant part of the real wage problem, but the April acceleration in food-at-home prices means the food contribution to purchasing power erosion may grow over the coming months.

The distributional consequences deserve emphasis. As documented in Brief #2026-2, lower-income households spend 25 to 35 percent of after-tax income on food, compared to 7 to 10 percent for the highest-income quintile. They also spend a larger share of their income on gasoline and are less able to reduce driving. The combination of declining real wages and rising prices for both energy and food creates a particularly acute squeeze for the households least able to absorb it. The energy shock was regressive when it was primarily a gasoline story; as it spreads into food, the regressive character deepens.

What April’s PPI Data Tells Us About Where Food Prices Are Heading

The April 2026 Producer Price Index, released on May 13, provides the upstream companion to the CPI report released the day before — and together they tell a coherent story about where food prices are and where they are likely heading. Final demand energy rose 7.8 percent in April and is now up 22.7 percent over the prior year, driven almost entirely by motor fuels and jet fuel. Consumers are already experiencing this at the gas pump and through airline fares. The PPI’s value for food price analysis, however, lies in the intermediate stages — the supply chain rungs between the energy shock and the grocery shelf.

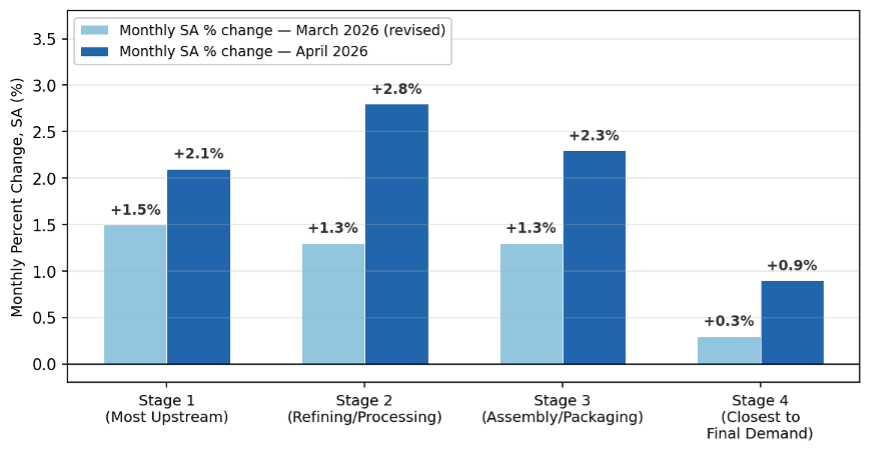

Figure 3

PPI Intermediate Demand by Production Stage: Monthly Percent Changes, March and April 2026

All monthly changes are seasonally adjusted. Stage definitions follow the BLS Final Demand–Intermediate Demand (FD-ID) production flow framework: Stage 1 industries (most upstream, e.g., oil and gas extraction, grain farming) produce inputs consumed by Stage 2 industries (e.g., petroleum refineries, natural gas distribution, cattle ranching), whose outputs flow to Stage 3 (e.g., food processing, motor vehicle parts manufacturing) and Stage 4 (closest to final demand, e.g., food service, retail trade, hospitals). The acceleration from Stage 4 in March (+0.3%) to April (+0.9%), and the elevated readings at Stages 2 and 3, are consistent with an energy cost wave propagating downstream toward food manufacturers and retailers. March figures reflect revised values published in the April 2026 PPI release. Source: U.S. Bureau of Labor Statistics, Producer Price Indexes — April 2026, Table D (intermediate demand by production flow), released May 13, 2026.

Figure 3 makes the pipeline dynamic visible. The BLS production stage framework organizes industries from the most upstream (Stage 1: raw extraction and grain farming) through to the nearest final demand (Stage 4: food service, retail, hospitals). Reading the April bars from left to right, the energy cost wave is clearly present: Stage 2 rose 2.8 percent for the month — the largest advance since August 2022 — driven by crude petroleum, natural gas, diesel fuel, and plastic resins feeding into refining and chemical manufacturing. Stage 3 rose 2.3 percent, reflecting industrial chemicals and packaging materials moving into food processing and assembly. Stage 4, where food manufacturers and retailers operate, rose a more modest 0.9 percent. The gradient — 2.8, 2.3, 0.9 — is the signature of a price shock that has hit hard upstream and is working its way downstream. Critically, the comparison with March (lighter bars) shows Stage 2 accelerating from +1.3% to +2.8%, meaning the upstream pressure is intensifying rather than fading. The conflict’s energy cost impact on the food supply chain is not behind us; it is advancing through the pipeline toward retail shelves.

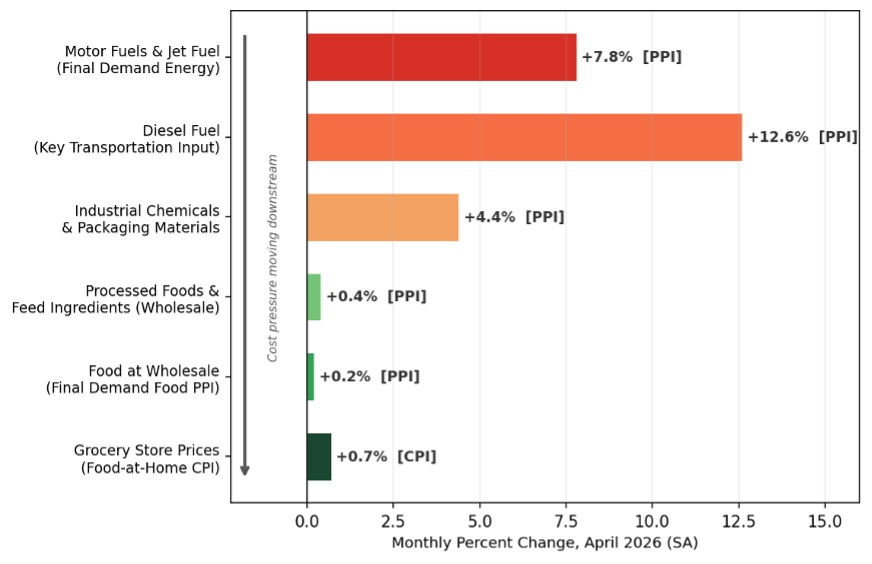

Figure 4 traces the specific commodity movements within that stage framework. The clearest food-relevant signal in April’s PPI data is the advance of industrial chemicals and plastic resins within processed intermediate goods. These are the petrochemical feedstocks for food packaging — the films, containers, and wraps that enclose virtually everything in the grocery store. Industrial chemicals rose 4.4 percent in April, and plastic resins and materials also increased significantly. Based on typical procurement and repricing cycles, these packaging cost increases will reach food manufacturers over the next one to two months and retail shelves by mid-summer. This is the cost wave currently loaded in the pipeline but not yet visible at the checkout counter. Keep in mind that the data in the April reports is already over two weeks lagged from the release dates.

Processed foods and feeds — the intermediate index most directly linked to food manufacturing inputs — rose 0.4 percent in April, its sixth consecutive monthly advance. Notably, despite six months of consecutive gains, the 12-month reading for this index remains at −0.6 percent — still negative — reflecting the degree to which pre-conflict deflationary forces in food-manufacturing inputs have been suppressing wholesale food costs. This is modest in isolation, but it sits at precisely the level our two-force analysis predicts. The pre-conflict tariff-driven and supply-side pressures that explain much of April’s retail food-at-home increase have not yet fully cleared the wholesale pipeline, while the Iran Conflict’s energy cost wave — still residing in the upstream industrial chemicals and packaging materials stages — has not yet arrived at the processed foods level in force. The 0.4 percent advance reflects the handoff point between these two forces, and as pre-conflict pressures finish clearing and conflict-driven costs advance downstream through packaging and logistics over the next two to three months, the processed foods and feeds index will face compounding pressure from both directions. The divergence between the upstream advance and the modest downstream reading is indicative of a price shock still in transit, not one that has fully cleared.

Figure 4

The Food Price Pipeline: Where April’s Cost Increases Sit. Monthly percent changes, April 2026 (seasonally adjusted)

Upstream energy costs hit hardest; industrial chemicals and packaging materials are now moving through the middle of the pipeline; wholesale and retail food costs are just beginning to respond. Sources: PPI stages — U.S. Bureau of Labor Statistics, Producer Price Indexes, April 2026 (released May 13, 2026). Grocery store prices — U.S. Bureau of Labor Statistics, CPI, April 2026 (released May 12, 2026).

Final demand food — what food manufacturers charge before the retail markup — rose only 0.2 percent in April, well below the 0.7 percent monthly increase in retail food-at-home prices from April’s CPI. This apparent inversion is not surprising. Some retail repricing in April reflects pre-existing tariff and supply chain pressures clearing simultaneously with the earliest conflict-driven cost increases, as we discussed in our earlier briefs. The two datasets together confirm that the pipeline is open and advancing, but that much of the conflict’s cost contribution to food prices is still upstream of the store shelf.

One piece of genuine good news for consumers in today’s PPI: corn prices fell within the Stage 1 intermediate demand data. This is consistent with global grain markets remaining calm. Iran is not a grain exporter, and direct grain supply disruption — the amplifier that made the 2022 Russia-Ukraine episode so severe — remains absent from the current shock. It also provides some reassurance about the cost structure of grain-based food products going forward, though energy, transportation and packaging costs will continue to pressure even these categories through the remainder of 2026.

Core Inflation and the Federal Reserve

Core inflation — all items less food and energy — rose 0.4 percent for the month and 2.8 percent over the prior 12 months, up from 2.6 percent in March. This acceleration reflects two sources: first, the cost pressure is broadening into transportation services, apparel, and other goods as energy costs permeate supply chains; second, a technical shelter catch-up effect from the October 2025 government shutdown data gap. Full-service restaurant prices and airline fares (up 20.7 percent year-over-year, driven by jet fuel cost pass-through) also contributed.

The Federal Reserve monitors both headline and core CPI as primary inputs to interest rate decisions. The April data present a more complex picture than March’s energy-only headline spike: a still-elevated headline (3.8 percent), a broadening core (2.8 percent), and real wages declining for the second consecutive month. These signals do not point uniformly in any single direction for monetary policy, and we do not speculate on rate decisions. What is clear is that the May and June CPI readings will be watched with particular intensity as the first clear test of whether the conflict’s cost pressure is producing durable inflation or a transitory spike that resolves with the conflict itself.

The 2027 Farm Impact: The Coming Crop-Cycle Reckoning

Our farm profitability brief (Brief #2026-1) documented the 2026 crop year outlook in detail and noted that the conflict’s farm-level impact would be complex and uneven in the near term. The April CPI and PPI data reinforce a forward-looking point that deserves an explicit statement. Direct farm income impacts from the Iran Conflict are likely to remain modest and mixed in the 2026 crop year.

The more consequential farm-level reckoning will come in 2027 — if Strait of Hormuz restrictions persist into the fall/winter 2026 purchasing cycle for inputs and the spring 2027 planting cycle. Many commercial farmers make fertilizer purchase commitments in late summer, fall, and winter for the following year’s crop. Most of the fertilizer going into the ground this spring was already contracted at pre-conflict prices or applied last fall, which is why the 2026 crop year is largely insulated from the worst of the input cost shock. But anhydrous ammonia, DAP, and potash prices have already risen materially from pre-conflict levels; if those prices remain elevated through the fall purchasing window, the 2027 crop will carry a substantially higher input cost structure than 2026. Combined with crop revenue that depends on grain prices, which have so far remained relatively contained — grain markets correctly recognizing that Iran is not a grain exporter — the fertilizer-to-crop price ratio could reach historically unfavorable levels heading into 2027 planting. In Brief #2026-6, we dive deeper into near and longer-term factors that may indicate the direction of grain and oilseed prices.

The PPI for fertilizers and agricultural chemicals is the indicator to watch for early signals of the 2027 farm profitability picture — and the news is not good. Retail fertilizer markets have already registered alarming increases: urea is up 49 percent year-over-year, anhydrous ammonia is up 43 percent, and all eight major fertilizers are more expensive than a year ago, with six of eight posting double-digit month-over-month increases in April alone. These are retail market prices; the BLS PPI fertilizer manufacturing sub-indices, buried in the detailed tables of the April release, tell a directionally consistent story at the wholesale level through the industrial chemicals and nitrogenates advance. The farms most exposed are those that did not pre-purchase inputs earlier in the season — particularly producers in the South growing cotton and rice, who face the current market without the protection that Midwest corn and soybean producers secured through earlier contracting.

Three Indicators to Watch

The May 2026 CPI report (scheduled for June 10) will be the most revealing reading yet of the conflict’s food-price footprint. It will be the first report to capture a full month of retail pricing under the conflict’s energy and packaging cost transmission, and will show the degree to which pre-existing pressures are giving way to those from the conflict-driven oil price shock.

The May PPI (scheduled for June 11) will show whether the industrial chemicals and packaging cost increases, now visible at the intermediate level in April, are advancing further toward food manufacturers. A continued increase in processed foods and feeds for intermediate demand above 0.5 percent, combined with further advances in plastic resins and industrial chemicals, would confirm the pipeline is advancing on the central scenario trajectory we projected in Brief #2026-2.

Real average weekly earnings over the next two to three months will reveal whether the purchasing power decline is transitory — a short-lived energy-shock effect that reverses as oil prices cool — or whether it is becoming structural, as food and other cost categories sustain the inflation rate above nominal wage growth. Two consecutive months of decline is significant; a third would signal a more durable household income squeeze with serious implications for consumer spending and food security among lower-income households.

The Bottom Line

The April 2026 CPI and PPI reports, read together, mark a clear transition in the inflation story: from an energy-only shock concentrated at the gas pump to a broadening cost pressure that is now reaching grocery shelves via the most energy-sensitive food supply chains, while also advancing through the industrial chemicals and packaging stages toward a broader food price impact in the months ahead. The transmission we predicted is unfolding on the schedule the supply chain lag model anticipated — and it is not finished.

The ultimate footprint of this episode depends on the duration of the Strait of Hormuz disruption, the nature of any conflict resolution, and the pace of crude oil price normalization. The April data suggest we are still in an early chapter of the story, not the end. The good news is that there is still time for a resolution to the conflict to mitigate any large structural food price inflation results. The households feeling it most acutely are those with the least capacity to absorb it — and as food prices accelerate in the coming months, that concentration of burden will only deepen.

References and Sources

Prior Farm Policy Study Group Briefs

Foster, K. and Dalheimer, B. (2026). “The Iran Conflict, Energy Prices, and U.S. Farm Profitability: A Balanced Assessment.” Extension Brief #2026-1. Purdue Agricultural Economics Report. https://ag.purdue.edu/commercialag/home/paer-article/the-iran-conflict-energy-prices-and-u-s-farm-profitability-a-balanced-assessment

Foster, K. and Dalheimer, B. (2026). “The Iran Conflict and Consumer Food Prices: A Broad but Lagged and Sticky Shock.” Extension Brief #2026-2. Purdue Agricultural Economics Report. https://ag.purdue.edu/commercialag/home/paer-article/the-iran-conflict-and-consumer-food-prices-a-broad-but-lagged-and-sticky-shock

Foster, K. and Dalheimer, B. (2026). “The Iran Conflict and Global Food Security.” Extension Brief #2026-3. Purdue Agricultural Economics Report. https://ag.purdue.edu/commercialag/home/paer-article/the-iran-conflict-and-global-food-security-why-the-burden-falls-hardest-on-the-worlds-most-vulnerable

Foster, K. and Dalheimer, B. (2026). “The March 2026 CPI Report: What It Tells Us About the Iran Conflict’s Inflation Footprint — And What Is Still Coming.” Extension Brief #2026-4. Purdue Agricultural Economics Report. https://ag.purdue.edu/commercialag/home/paer-article/the-march-2026-cpi-report-what-it-tells-us-about-the-iran-conflicts-inflation-footprint-and-what-is-still-coming

Foster, K. and Dalheimer, B. (2026). “The March 2026 Producer Price Index: Reading the Food Price Pipeline.” Extension Brief #2026-5. https://ag.purdue.edu/commercialag/home/paer-article/the-march-2026-producer-price-index-reading-the-food-price-pipeline

Foster, K., Dalheimer, B., and Keeney, R. (2026). “Commodity Prices at the Crossroads: Trade Policy, the Iran Conflict, and the 2026 U.S. Grain Markets.” Extension Brief #2026-6. Purdue Agricultural Economics Report. https://ag.purdue.edu/commercialag/home/paer-article/commodity-prices-at-the-crossroads-trade-policy-the-iran-conflict-and-the-2026-u-s-grain-markets

Sources & Additional Reading

Amiti, M., Flanagan, C., Heise, S. and Weinstein, D. (2026). “Who is Paying for the 2025 U.S. Tariffs?” Liberty Street Economics, Federal Reserve Bank of New York. New York Federal Reserve research estimates that tariff pass-through to consumer prices has risen to approximately 90 percent in 2026

Baumeister, C., and Kilian, L. (2014). “Do oil price increases cause higher food prices?” Economic Policy, 29(80), 691–747. https://doi.org/10.1111/1468-0327.12039

Kilian, L., and Zhou, X. (2023). “A broader perspective on the inflationary effects of energy price shocks.” Energy Economics, 125, 106893. https://www.sciencedirect.com/science/article/abs/pii/S0140988323003912

Kilian, L., and Zhou, X. (2022). “The impact of rising oil prices on U.S. inflation and inflation expectations in 2020–23.” Energy Economics, 113, 106228. https://doi.org/10.1016/j.eneco.2022.106228

USDA, ERS. (2026) “Food Price Outlook, 2026.” https://www.ers.usda.gov/data-products/food-price-outlook/summary-findings

Data Sources

U.S. Bureau of Labor Statistics, Consumer Price Index — April 2026 (released May 12, 2026), https://www.bls.gov/cpi/; BLS Producer Price Indexes — April 2026 (released May 13, 2026), https://www.bls.gov/ppi/; BLS Real Earnings Summary — April 2026, https://www.bls.gov/news.release/realer.nr0.htm; USDA Economic Research Service Food Price Outlook, https://www.ers.usda.gov/data-products/food-price-outlook/.

![]()

![]()

![]()

![]()

![]()