Learning International Economics the Hard Way

March 23, 2026

PAER-2026-03

Author: Russell Hillberry, Professor of Agricultural Economics

![]()

![]()

![]()

![]()

![]()

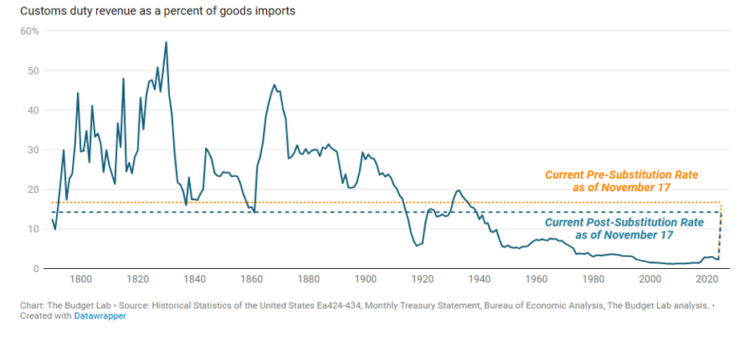

For several years running, the price of bananas at my supermarket in West Lafayette, IN, had been remarkably constant at $0.49/lb. On April 2 of last year, having convinced himself that “foreign countries pay U.S. tariffs,” President Trump raised tariffs on U.S. imports to levels not seen since the Great Depression (see Figure 1). My supermarket’s banana price quickly rose to $0.55/lb. In November, facing criticism for higher prices at the grocery store, the President exempted bananas and other tropical products from the tariffs (Phillips Erb, 2025). The price of bananas in my supermarket promptly returned to $0.49/lb. The lesson – that a tariff on imports is paid (in large part, or even in full) by the importing countries’ consumers – could have been learned much more easily if someone with access to the President had simply opened an undergraduate textbook on International Economics. Instead, we have had to learn these lessons the hard way.

Figure 1

U.S. Average Effective Tariff Rate Since 1790

Source: Yale University Budget Lab

While it is annoying to pay unnecessarily high prices, the total burden of the President’s tariffs on consumers is, in most cases, manageable. Most household expenditures are on services rather than goods, and only imported goods are subject to tariffs. Providers of services have marginally higher costs when using imported goods as inputs, but since these inputs are typically not large shares of most service providers’ costs, it is unlikely that this channel puts substantial upward pressure on prices faced by households. Housing, for example, is a large component of total household spending, but tariffs on imported lumber and steel only affect the cost of new housing. Impacts on the price of the existing housing stock are negligible. In addition to their relatively low exposure to goods affected by tariffs, consumers also have some flexibility, potentially avoiding tariffs by shifting their consumption away from products subject to tariffs (like not buying bananas in the example above). Inflation, as it affects U.S. households, has also been kept in check by reduced oil prices since the President took office.

Instead, it is certain kinds of businesses that bear a disproportionate share of the tariff burden. As the textbooks would tell us, the primary economic effects of tariffs (beyond raising revenue for the government) are that they favor some domestic industries at the expense of other domestic industries. In the simplest models, tariffs cause the industries that are productive enough to export to shrink while growing the industries that are not productive enough to compete with imports. The shift of domestic resources from more internationally competitive to less competitive industries is a drag on the overall economy, but the main effects of trade restrictions are distributional: exporting firms lose while firms that compete with imports win.

Making things just a bit more complicated, the industries most negatively affected by tariffs are typically those that a) have imported or other tariff-sensitive goods as a large share of their input costs, b) compete in foreign markets against firms whose countries do not impose high tariffs on their inputs, and c) have difficulty moving their production abroad. Export-oriented agriculture clearly meets conditions (b) and (c). Condition (a) applies to agriculture via its purchases of steel-intensive capital goods such as farm machinery and structures, for example. U.S. tariffs raise the cost of steel in imported goods by 50%. The 2025 tariffs are a perfect storm for export-oriented agriculture.

In last year’s trade outlook, Hillberry (2025) explained that a credible computational model of the effects of the expected Trump tariffs had estimated that the U.S. soybean-producing sector would pay sizable costs if the Trump Administration imposed tariffs on imports from China and would suffer even more if China retaliated. As the 2025 version of this outlook argued was likely, the Trump Administration did in fact impose tariffs on China; China did retaliate against U.S. exports; and the soybean sector suffered. While the Trump administration has proposed a $12 billion bailout for U.S. agriculture, Ailworth et al. (2025) report that many farmers and analysts think that the bailout funding will be insufficient to compensate for the difficult environment generated by the tariffs. There is now a new “deal” with China, but it is not an agreement that we should expect to stick (Attempts to negotiate specific economic outcomes, such as purchase or investment commitments in trade agreements, almost always fail; international trade does not work like that). In broad terms, 2025 saw a replay of the trade war of 2018-2019, with a bailout package band-aid applied to open wounds generated by the negative and predictable consequences for export-oriented agriculture of U.S. tariff increases. Apparently, some lessons prove difficult to learn, even when they were experienced in the quite recent past.

Apologists for the Trump Administration’s chaotic and unwise trade policies, including several elected representatives from Indiana, argue that the Trump administration’s tariffs are simply being used to negotiate “better” agreements. They sometimes go further and claim that the tariffs are only temporary. One wonders if these representatives are arguing in bad faith, or whether they, like the President, lack even a basic understanding of International Economics.

With respect to the “better” agreements, Handley (2025) explains that a key attribute of successful trade agreements is that they are seen to be permanent; they reduce uncertainty about the future path of tariffs and other trade costs. The President’s trade policies – including his “deals” – have generated enormous uncertainty for market participants. The deals have not been submitted to Congress for ratification; they are subject to the same Presidential whims as the agreements that were already in place when he entered office. The President’s deals are almost always structured to avoid credible legal commitments. These agreements are worse, not better, than the formal trade agreements that were in place when the President took office.

Moreover, our representatives’ claim that the tariffs are only temporary simply beggars belief. As discussed last year in Hillberry (2025), the President simply has too many policy objectives that require high tariffs to be in place. First, the tariffs generate revenue that partially offsets the income and corporate tax cuts passed in the “big beautiful bill.” (Shifting the tax burden from one group of Americans to another would be a legitimate political choice if done by Congress, but textbook International Economics teaches that tariffs are an extremely inefficient way to raise tax revenue.) Second, the tariffs are part of the President’s plan to rebuild the U.S. manufacturing sector, a plan that can only work if firms expect the tariffs to be in place long enough to justify long-run investments in domestic capacity. (U.S. manufacturing employment was down sharply in 2025, in part because tariffs on inputs such as steel raised the cost of producing downstream goods in the U.S.) Third, even the President’s “deals” leave U.S. tariff rates at high levels (the US-EU “deal,” for example, leaves U.S. tariffs on EU goods at 15%, and the tariffs on steel remain at 50%). Finally, the President likes to use tariffs as a domestic political tool, exchanging tariff exemptions for political contributions. The information technology sector, for example, has received exemptions for most of its inputs in 2025, in part because its leaders have groveled publicly in the President’s presence, giving the President lavish gifts, and donating to finance the construction of the White House ballroom. Fotak et al. (2025) offer formal statistical evidence that the President’s exemption process favors well-connected Republican donors. The President cannot profit from this tariff exemption process – either politically or personally – without a high average tariff from which to make exemptions.

More broadly, we can see that the President has generally sought to maximize his personal role in determining U.S. economic outcomes. He has sought to involve himself directly in government decisions about mergers and acquisitions (see Dlouhy and Nylen, 2025), decisions that should follow legal precedent rather than the President’s whims. He claims the authority to direct foreign investments (see Ma, 2025), investments that would be more valuable if guided by market opportunities. The tariffs are a small but important part of this same overall story. The President has effectively nullified trade agreements ratified by Congress and signed by earlier Presidents. He has taken the tariff exemption process away from Congress and brought it inside the White House, where exemption decisions are not subject to open debate or appeal. International Economics research has shown how corrupt Presidents in other countries use high tariffs to enrich themselves at the cost of their citizens. For example, Rijkers et al. (2015) show that firms associated with President Ben Ali of Tunisia paid lower tariffs than did otherwise equivalent Tunisian firms.

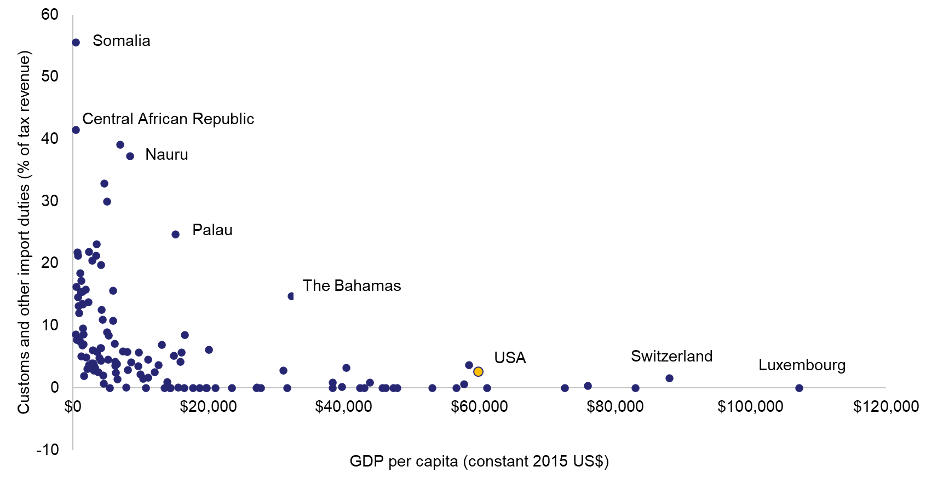

There is a long list of other International Economics lessons that apparently need re-learning (The Constitution gives Congress the power to set tariffs, not the President! It is not governments who trade, it is firms! Trade deficits are a macro-economic phenomenon, not a result of unfair trade policy!). But let us conclude this section of the review with one more lesson: Trade barriers slow the economic growth of countries that impose them. Because the world is messy, this particular claim is difficult to prove; it is nonetheless widely believed among Economists who study these matters. Figure 2 demonstrates that high-tariff countries have low incomes, but this is correlation, not causation. Persuasive statistical studies more rigorously link higher tariffs to slower growth, but these studies, too, are subject to professional caveats.

Figure 2

Tariffs as a share of government revenue and per capita income, 2018

Note: Author calculations using 2018 data from the World Development Indicators.

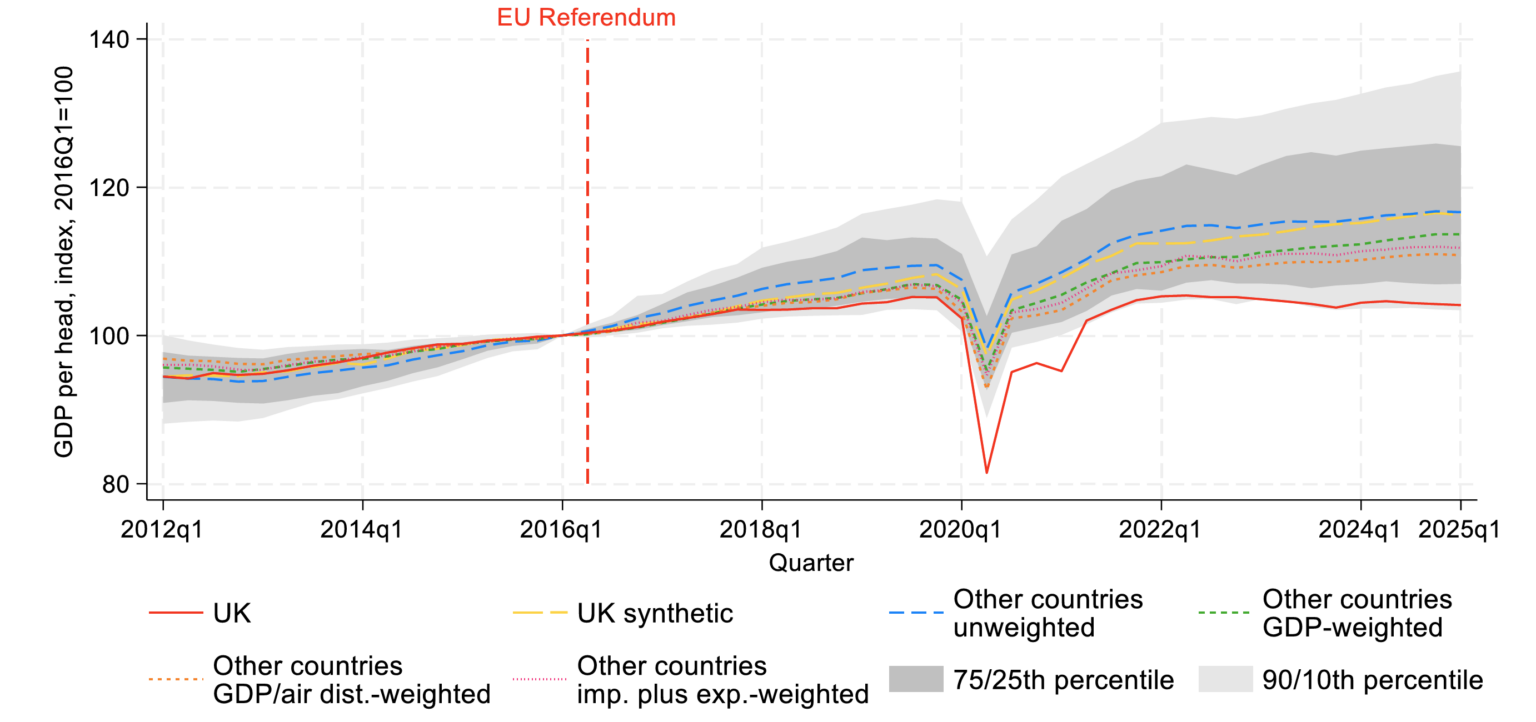

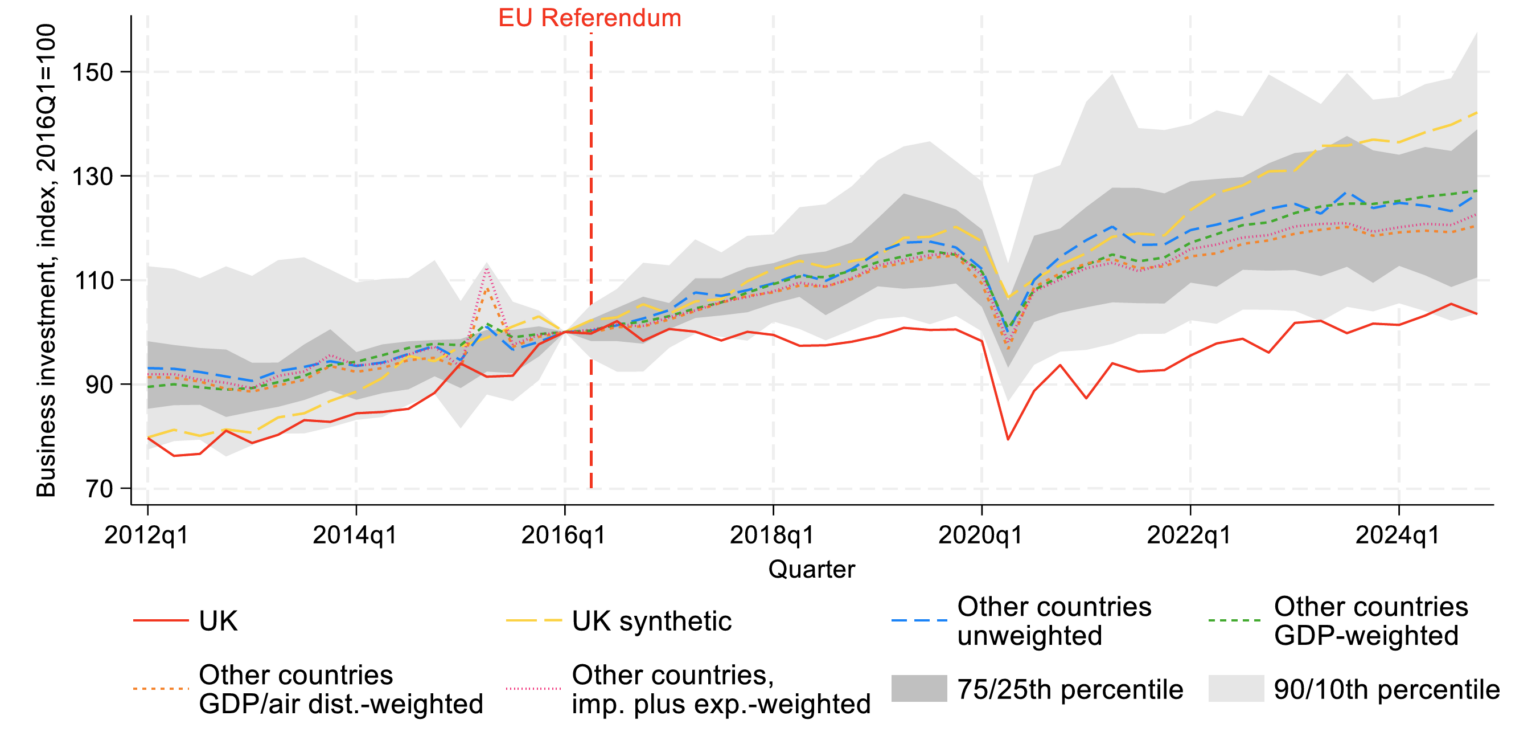

For the purposes of this review, perhaps the best evidence that trade barriers reduce economic growth is the now-visible consequences of Brexit, the populist-fueled exit of the United Kingdom from the European Union in 2016. While Brexit did not materially change British tariffs, it made trade with the European Union much more difficult and generated substantial uncertainty about the future path of British trade policy. We now have quite persuasive evidence that Brexit reduced the growth of the British economy. For example, Bloom et al. (2025) conducted a comprehensive study of the effects of Brexit on economic outcomes in the United Kingdom. Figures 3 and 4 below show comparisons of per capita income and business investment in high-income countries. Since the Brexit referendum, the British economy (red line) has lagged behind comparison economies significantly on both measures. Other statistical tests in the paper formalize these and other related insights in different ways. The broad lesson is that Brexit has slowed economic growth in the United Kingdom, relative to other high-income countries.

Figure 3

Brexit and per capita income growth in the United Kingdom

Source: Bloom, N., Bunn, P., Mizen, P., Smietanka, P. and Thwaites, G., 2025. The

Economic Impact of Brexit. National Bureau of Economic Research, No. w34459.

Figure 4

Brexit and business investment in the United Kingdom

Source: Bloom, N., Bunn, P., Mizen, P., Smietanka, P. and Thwaites, G., 2025. The

Economic Impact of Brexit. National Bureau of Economic Research, No. w34459.

Trade Policy Outlook for 2026

Given the trade policy chaos in 2025, constructing a trade policy forecast for 2026 is not a straightforward exercise. Nonetheless, broadly it seems reasonable to expect the following four outcomes.

1) Continued volatility in U.S. tariffs.

In imposing his “Liberation Day” tariffs, the President invoked the International Emergency Economic Powers Act (IEEPA), a law that does not even mention the word “tariffs” and requires the existence of an emergency that was not the least bit apparent when he invoked the law. Several courts have determined that the President’s tariffs were illegal, and we simply await a decision from the U.S. Supreme Court to validate or overturn these lower court rulings. It is difficult to predict the Supreme Court’s ruling: On the one hand, the Conservative-leaning court has become quite partisan in its rulings on matters related to the President; On the other hand, a Conservative-leaning court would otherwise be unlikely to endorse an arbitrary and illegal tax increase like the President’s tariffs. If the Court overturns the IEEPA tariffs, the President has threatened to impose new tariffs using different authorities, thus generating even more whipsaw tariff action in 2026. If the Court allows the tariffs to stay in place, prices will rise; many firms have been holding off on price increases while the case makes its way through the courts. Rising import prices will trigger even more domestic pain, which may cause the President to walk back some of the tariffs he has already imposed. One way or another, expect more tariff changes in 2026.

2) Foreign countries will continue to reduce their exposure to trade with the United States.

The U.S. is now seen as an unreliable trading partner. Traditional U.S. trading partners have responded by seeking to deepen their relationships with other partners. Canada, in particular, has been active in this regard, seeking new free trade agreements with Europe and in Asia. The U.S. is too large to be entirely isolated, but foreign governments have learned not to overinvest in deep trade relations with the U.S. We should expect this trend to continue in 2026 and for the foreseeable future.

China’s response to the President’s 2018 trade war was to reduce its dependence on imports of U.S. soybeans. One strategy has been to cultivate other suppliers like Brazil and Argentina, but China is also pushing for self-sufficiency. Zuo (2025) summarizes a report by Goldman Sachs analysts who expect that the share of imported soybeans in Chinese consumption will fall from 90 percent to 30 percent within the next decade. The introduction of genetically modified seeds and changes in the feed mix are allowing China to reduce its dependence on imports.

3) The average U.S. tariff will be lower at the end of 2026, but remain very high by post-World War II standards.

The President has shown that he responds to the economic pain caused by tariffs. These responses are usually too slow and too small, but they do happen. Much of the pain generated by his 2025 tariffs has been deferred, as firms wait on the Supreme Court’s decision before following through with higher prices. If the Supreme Court allows the IEEPA tariffs to remain, prices will rise, and the increasing pain of rising prices will lead to some political pressure to reduce them. If the Supreme Court decides to overturn the tariffs, the President will have a difficult time fully replacing the IEEPA tariffs with tariffs justified by other authorities. Either path leads to lower, but still high, average tariffs in 2026. Moreover, the President seems to be open to giving tariff exemptions to large importing firms whose leaders bring a combination of gifts/flattery to the White House. Tariff exemptions like these will continue to be made, and will cause the average tariff to drift slowly downward, while remaining at very high levels by historical standards.

One might also hope for Congressional action to reduce tariffs. We shall see. The President has shifted the domestic political narrative, such that members of Congress who should know better have abandoned their principles along with their sworn duty to protect and defend the Constitution (Article I, Section 8 of the Constitution says that Congress sets tariff rates, not the President). We are not in the emergency that the President has claimed. Congress should have acted on this fact already and rejected the IEEPA tariffs. Indiana’s delegation has been part of the problem. Our two senators have both voted repeatedly to keep the tariffs in place. In the House of Representatives, most Indiana members have voted to avoid taking any vote at all on the tariffs, effectively acting to leave them in place. Only the two Democratic representatives and Victoria Spartz voted to have the House take up its legal duty to determine whether or not the President’s claimed emergency justifies the tariff increases. It is to be hoped that Congress will do better in 2026, but it seems unlikely.

4) Renegotiation of the USMCA will be a prominent trade policy issue for 2026.

As was discussed in last year’s outlook, Mexico is an important market for U.S. agriculture. It buys a large share of the United States’ corn, pork, and poultry exports. So far, most goods that qualify under the U.S.-Mexico-Canada Agreement (USMCA) still enter the U.S. tariff-free, leaving little reason for Mexico to retaliate. But the President sees the 2026 USMCA renewal process as another opportunity to “negotiate,” which means threats of higher U.S. tariffs and more uncertainty on both sides of the border. The Mexican economy is highly dependent on sales in the U.S. market, but it, like Canada, should probably begin looking elsewhere. The ways in which the President approaches USMCA renegotiation in 2026 will likely have longer-term consequences for U.S. agricultural exports to Mexico.

Summary

U.S. trade policy in 2026 will not be as damaging as it was in 2025. But the remaining high tariffs mean that 2026 will likely be the second-most damaging year in the last ninety, trailing only 2025. We will not soon return to the 2016 situation, nor even that of 2024. The U.S. has badly damaged its reputation as a reliable trading partner, and this damage will not soon be undone. Canadian Premier Mark Carney has said, “The system of global trade anchored on the United States … is over. The 80-year period when the United States embraced the mantle of global economic leadership … is over. While this is a tragedy, it is also the new reality.” Unfortunately, he is almost certainly right about this.

The U.S. economy is a large one, and so not, in aggregate, overly dependent on international trade. Tariffs are not a large enough drag on the entire economy to generate a quick reversion to better trade policy. But the President’s tariff chaos will continue to hurt export-oriented agriculture more than most sectors of the economy. The traditional path to expanding U.S. agriculture exports – durable and credible free trade agreements – will not be available in the near term. The focus must be on helping Washington to learn the lessons of International Economics as quickly and as painlessly as possible. It will not be easy. Both the President and a majority in Congress seem committed to learning these lessons the hard way, and possibly not at all.

References

Ailworth, Erin, Michael Hirzer and Ilena Peng. 2025. “US Farmers Say $12 Billion Bailout Won’t End Industry Slump,” Bloomberg, December 8, reprinted at Equipment Finance News. https://equipmentfinancenews.com/news/agriculture/us-farmers-say-12-billion-bailout-wont-end-industry-slump/

Bloom, N., Bunn, P., Mizen, P., Smietanka, P. and Thwaites, G., 2025. The Economic Impact of Brexit. National Bureau of Economic Research, No. w34459. https://doi.org/10.3386/w34459

Dlouhy, Jennifer A. and Leah Nylen. 2025. “Trump Warner Bothers Meddling Pushes the Limits of Executive Power,” Bloomberg, December 11. https://docs.house.gov/meetings/JU/JU05/20251216/118753/HHRG-119-JU05-20251216-SD002-U2.pdf

Erb, K. P. (2025, November 17). Trump reverses tariffs on coffee, bananas and other foods in response as prices soar. Forbes. https://www.forbes.com/sites/kellyphillipserb/2025/11/17/trump-reverses-tariffs-on-coffee-bananas-and-other-foods-in-response-as-prices-soar/

Fotak, V., Lee, H. S., Megginson, W. L., & Salas, J. M. (2025). The political economy of tariff exemption grants. Journal of Financial and Quantitative Analysis, 60(6), 2678–2717. https://doi.org/10.1017/s0022109024000437

Handley, K. (2025, June 11). Uncertainty is the new Trump tariff — and everybody loses. National Review. https://www.nationalreview.com/2025/06/uncertainty-is-the-new-trump-tariff-and-everybody-loses/

Hillberry, R. 2025. “Interesting times for U.S. trade policy,” Purdue Ag Econ Report, January 2021. https://ag.purdue.edu/commercialag/home/paer-article/interesting-times-for-u-s-trade-policy/

Ma, J. (2025, July 29). U.S.-Japan trade deal gives Trump control over $550 billion in investments. It could be ‘vaporware’—and a model for other countries. Fortune. https://fortune.com/2025/07/26/us-japan-trade-deal-trump-tariffs-550-billion-investment-vehicle/

Rijkers, B., Baghdadi, L., & Raballand, G. (2015). Political Connections and Tariff Evasion Evidence from Tunisia. The World Bank Economic Review, 31(2), 459–482. https://doi.org/10.1093/wber/lhv061

State of U.S. tariffs: November 17, 2025. (n.d.). The Budget Lab at Yale. https://budgetlab.yale.edu/research/state-us-tariffs-november-17-2025

Zuo, M. (2025, December 12). China’s food-security push to slash soy imports by two-thirds in a decade: Goldman Sachs. South China Morning Post. https://www.scmp.com/economy/global-economy/article/3336111/chinas-food-security-push-slash-soy-imports-two-thirds-decade-goldman-sachs

![]()

![]()

![]()

![]()

![]()