September 23, 2020

Measuring Repayment Capacity and Farm Growth Potential

by Michael Langemeier

![]()

![]()

![]()

![]()

![]()

Introduction

Repayment capacity measures include the capital debt repayment capacity, capital debt repayment margin, replacement margin, term debt and capital lease coverage ratio, and replacement coverage ratio (Farm Financial Standards Council). Capital debt repayment capacity, capital debt repayment margin, and the term debt and capital lease coverage ratio address a farm’s ability to repay operating loans and to cover the current portion of principal and interest due on noncurrent loans such as a machinery, building, or land loan. The replacement margin and the replacement margin coverage ratio enable borrowers and lenders to evaluate whether a farm has sufficient funds to repay term debt and replace assets. For a farm to grow, it is essential that the replacement margin be large enough to repay term debt, replace assets, and purchase new assets, and that the replacement coverage ratio be greater than one. This article defines and illustrates the use of key repayment capacity measures.

Definitions

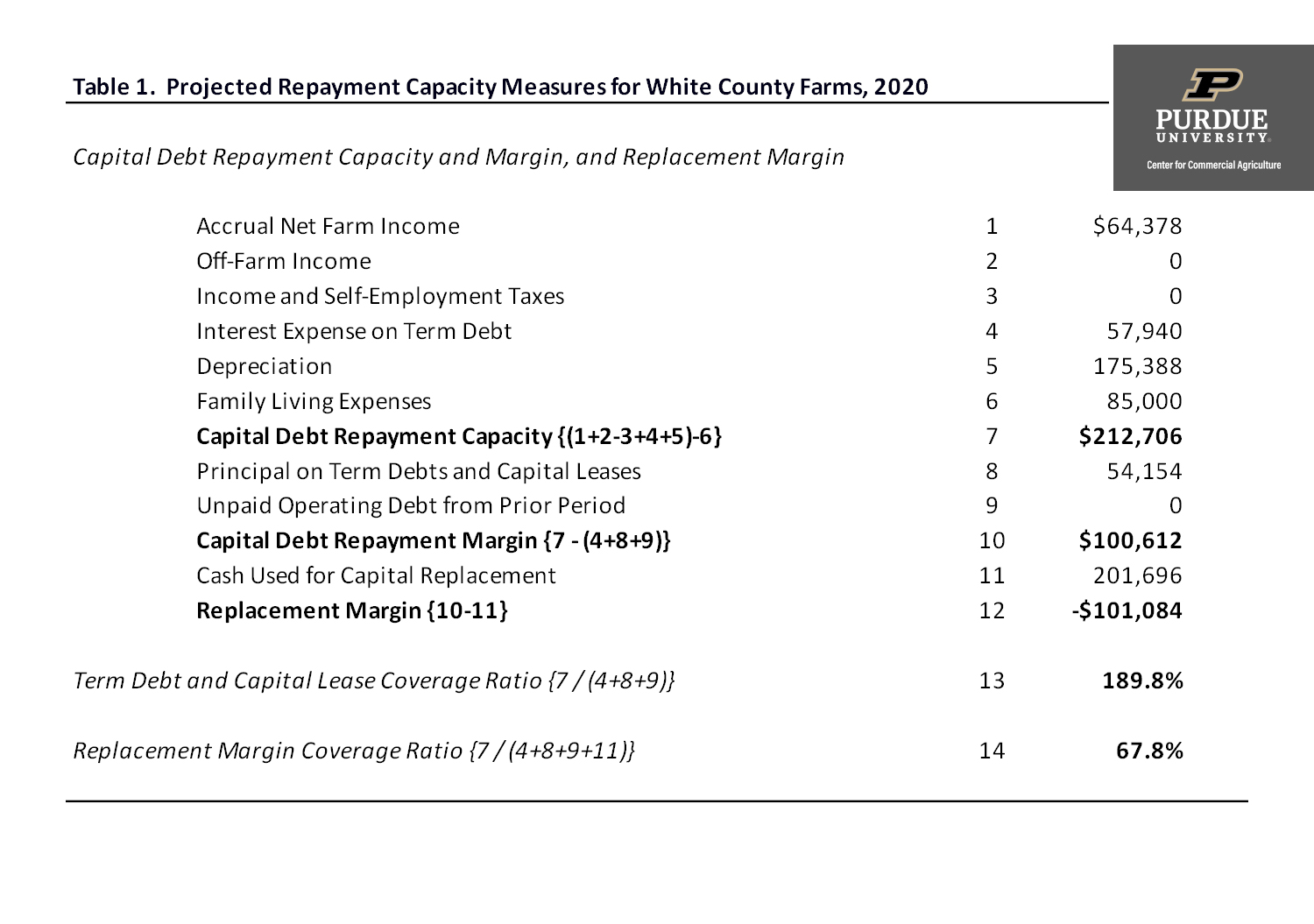

The capital debt repayment capacity margin is computed by subtracting interest expense on term debt, principal on term debt and capital leases, and unpaid operating debt from prior periods from capital debt repayment capacity. Table 1 illustrates the computation of the projected capital debt repayment capacity for 2020 for a case farm in west central Indiana, which will be discussed more below. Essentially, to compute this measure, a farm subtracts family living expenses and income and self-employment taxes from a sub-total consisting of accrual net farm income, off-farm income, and depreciation. The capital debt repayment margin enables borrowers and lenders to evaluate the ability of a farm to generate the necessary funds to repay the current portion of term or noncurrent debt. For this to happen, accrual net farm income, off-farm income, and depreciation have to be large enough to cover family living expenses, income and self-employment taxes, principal and interest on term debt, and unpaid operating debt from prior periods. It is important to note that the appropriate margin will vary among farms, and depends on the size of the farm and the type of enterprises produced.

Table 1. Projected Repayment Capacity Measures for White County Farms, 2020

The term debt and capital lease coverage ratio is closely related to the capital debt repayment margin. To compute this ratio, divide capital debt repayment capacity by principal and interest on term debt. A ratio greater than one indicates that the farm has enough funds to cover principal and interest on term debt.

The replacement margin and the replacement margin coverage ratio take the analysis one step further. The replacement margin is computed by subtracting cash used for capital replacement from the capital debt repayment margin. This measure enables a borrower to evaluate a farm’s ability to repay term debt and replace assets. It can also be used to evaluate a farm’s ability to acquire additional assets. Cash used for capital replacement can be measured using actual capital purchases (more specifically the portion of capital purchases that need to be paid for in the first year) or depreciation. The idea behind using depreciation is straightforward. Depreciation represents wear and tear, and obsolesce of machinery and buildings. Over the long-run, a farm needs to be able to replace machinery that is wearing out, to be able to afford new technology, and to be able to expand. We typically recommend using depreciation plus another 10 to 20 percent of depreciation as the farm’s measure of cash used for capital replacement. This amount will likely not be covered every year. However, over the long-run, it is essential that the replacement margin be positive. Without a positive replacement margin, a farm will not be able to fully replace depreciable assets or grow. Like the capital debt repayment margin, the replacement margin varies by farm size and type.

The replacement margin coverage ratio is closely related to the replacement margin. To compute this ratio, divide capital debt repayment capacity by the sum of principal and interest on term debt, unpaid operating debt in prior periods, and cash used for capital replacement. If the replacement margin coverage ratio is greater than one, the farm has sufficient funds to repay term debt and replace assets.

Case Farm Example

Table 1 provides an illustration of the repayment capacity measures discussed above for a case farm in west central Indiana. This case farm has 3000 acres of corn and soybeans. Cash used for capital replacement was computed by multiplying depreciation by 1.15. This ensures that there are enough funds available long-term to replace equipment and to expand. The information in table 1 is based on projections in mid-September rather than actual data. It is often useful to compute both actual and projected repayment capacity measures.

Projected capital debt repayment capacity for the case farm is $212,706. This amount is large enough to cover principal and interest on term debt. Consequently, the farm’s capital debt repayment margin is a positive $100,612. The replacement margin, however, is negative indicating that the farm is not expected to generate enough funds in 2020 to cover both term debt obligations and to replace assets. This is also signified by a replacement margin coverage ratio that is less than one or less than 100 percent.

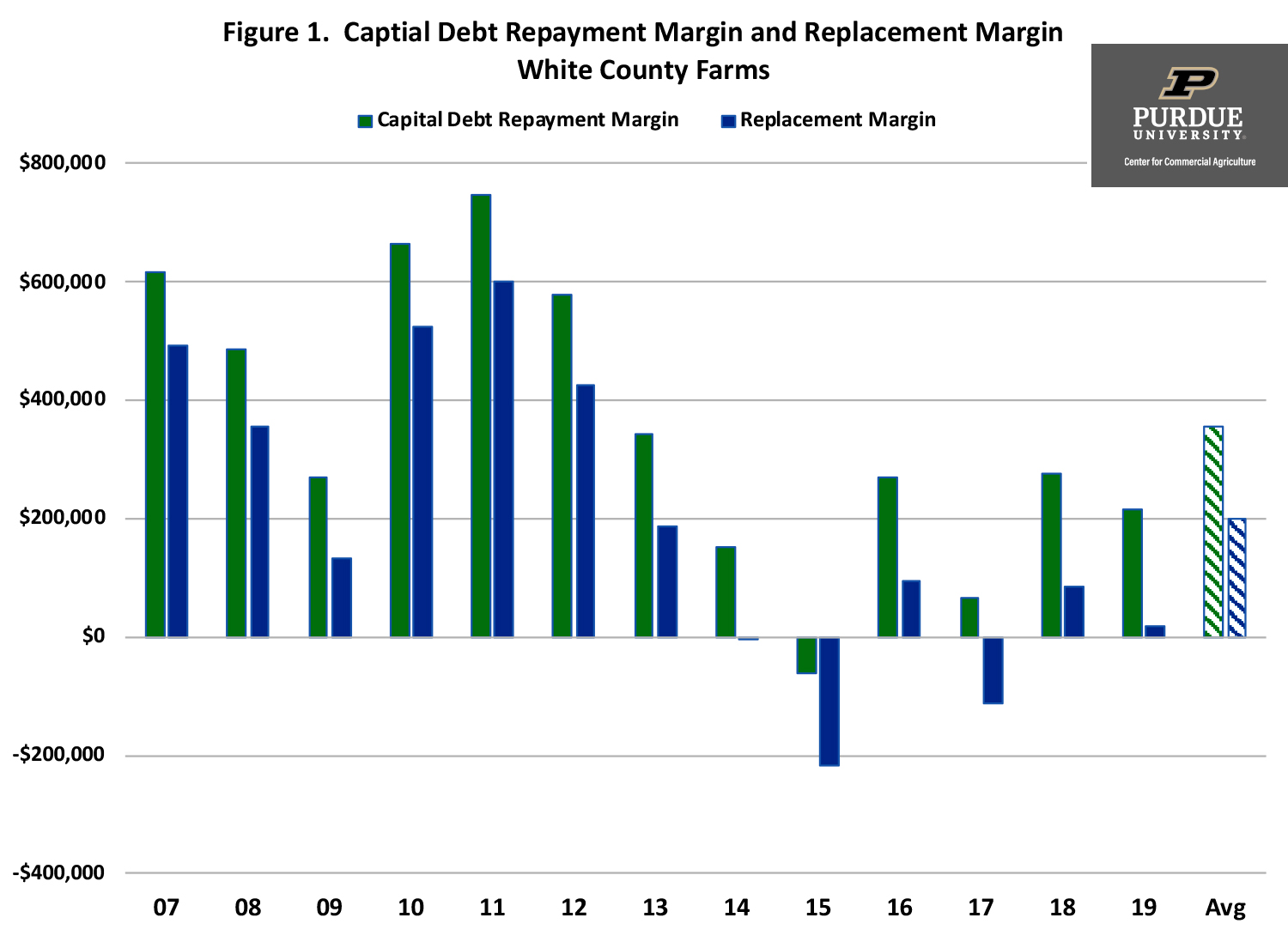

Because of the negative projected replacement margin in 2020, it is important for this farm to evaluate whether the replacement margin is positive over the long-run. Figure 1 presents the capital debt repayment margin and the replacement margin for the case farm from 2007 to 2019. As a frame of reference, average value of farm production and average net farm income from 2007 to 2019 were $2,094,978 and $375,007, respectively. The capital debt repayment margin was negative in 2015, but positive in every other year. The average capital debt repayment margin was $356,131. This margin was particularly strong from 2007 to 2013. The replacement margin was negative in 2014, 2015, and 2017. The long-run average replacement margin was $198,774, indicating that the farm has the ability to cover both term debt obligations and replace assets. Whether the replacement margin is large enough in the long-run to bring another family member into the business or expand rapidly would need further analysis.

Figure 1. Capital Debt Repayment Margin and Replacement Margin

White County Farms

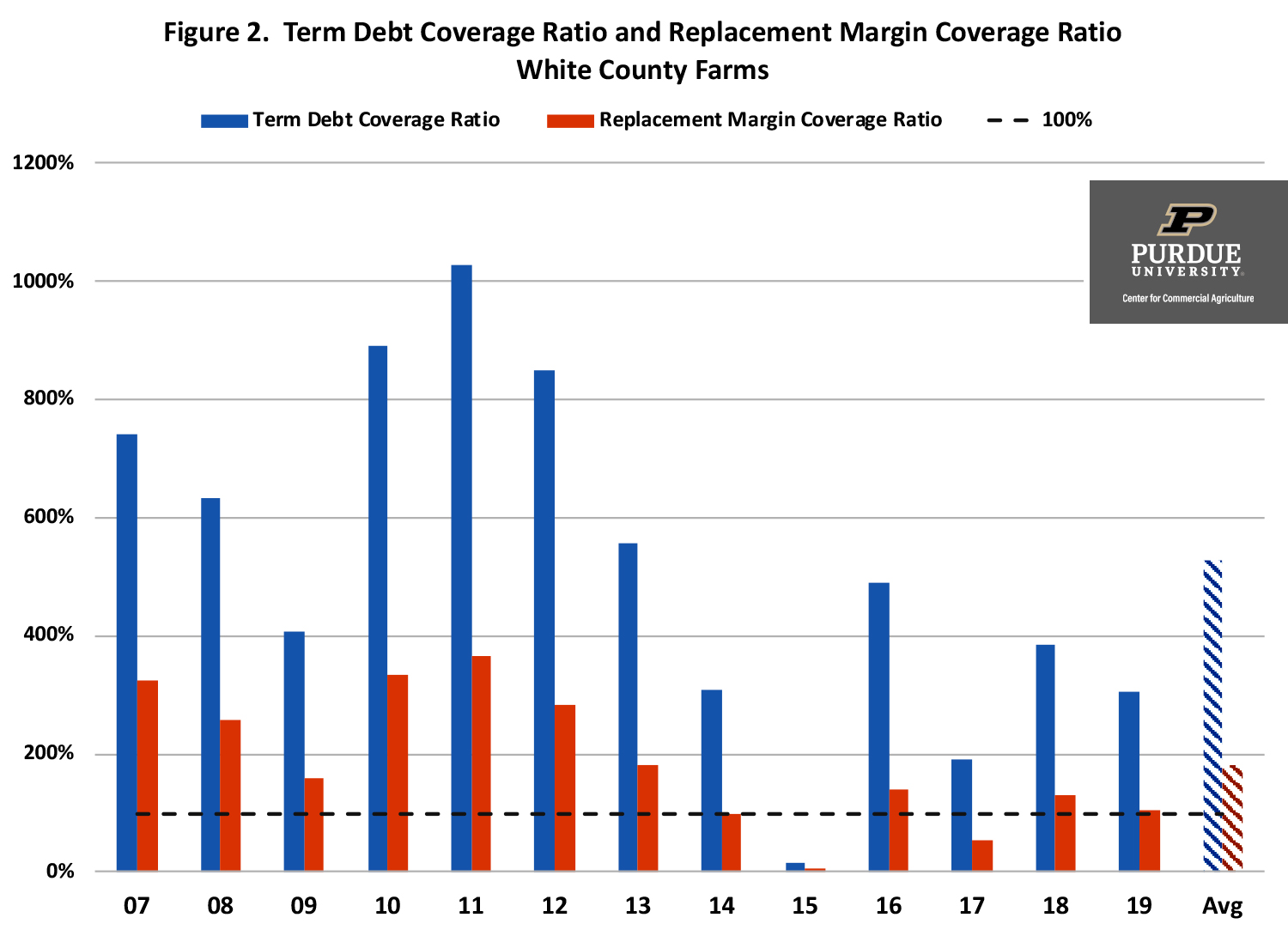

Some individuals prefer to use coverage ratios rather than dollar amounts to evaluate a farm’s repayment capacity. Figure 2 presents trends in the term debt coverage ratio and replacement margin coverage ratio for the case farm. This figure contains similar information to that illustrated in figure 1.

Figure 2. Term Debt Coverage Ratio and Replacement Margin Coverage Ratio

White County Farms

Concluding Comments

Repayment capacity measures are used to evaluate the ability of a farm to repay term debt and replace assets. This article focused on the capital debt repayment margin, the term debt and capital lease coverage ratio, the replacement margin, and the replacement margin coverage ratio. A positive capital debt repayment margin and a term debt and capital lease coverage ratio greater than one indicates that a farm has generated enough funds to repay term debt. A positive replacement margin and a replacement margin coverage ratio greater than one signals that a farm has generated enough funds to repay term debt and replace assets. The replacement margin and the replacement margin coverage ratio can also be used to gauge a farm’s ability to expand.

Repayment capacity measures for a case farm in west central Indiana were illustrated. The case farm had enough funds to repay term debt, but not enough funds to fully replace assets in 2020. The farm’s average replacement margin since 2007, however, was positive. For this farm to expand in the future, the average replacement margin over the next five to ten years will also need to be positive.

References

Farm Financial Standards Council. “Financial Guidelines for Agriculture”, January 2017.

![]()

![]()

![]()

![]()

![]()

TEAM LINKS:

PART OF A SERIES:

RELATED RESOURCES

UPCOMING EVENTS

We are taking a short break, but please plan to join us at one of our future programs that is a little farther in the future.