2026 Farmland and Cash Rent Outlook

March 23, 2026

PAER-2026-12

Authors: Binayak Kunwar, Ph.D. Student, Agricultural Economics; Todd Kuethe, Professor of Agricultural Economics, Schrader Chair in Farmland Economics

![]()

![]()

![]()

![]()

![]()

Farmland Values

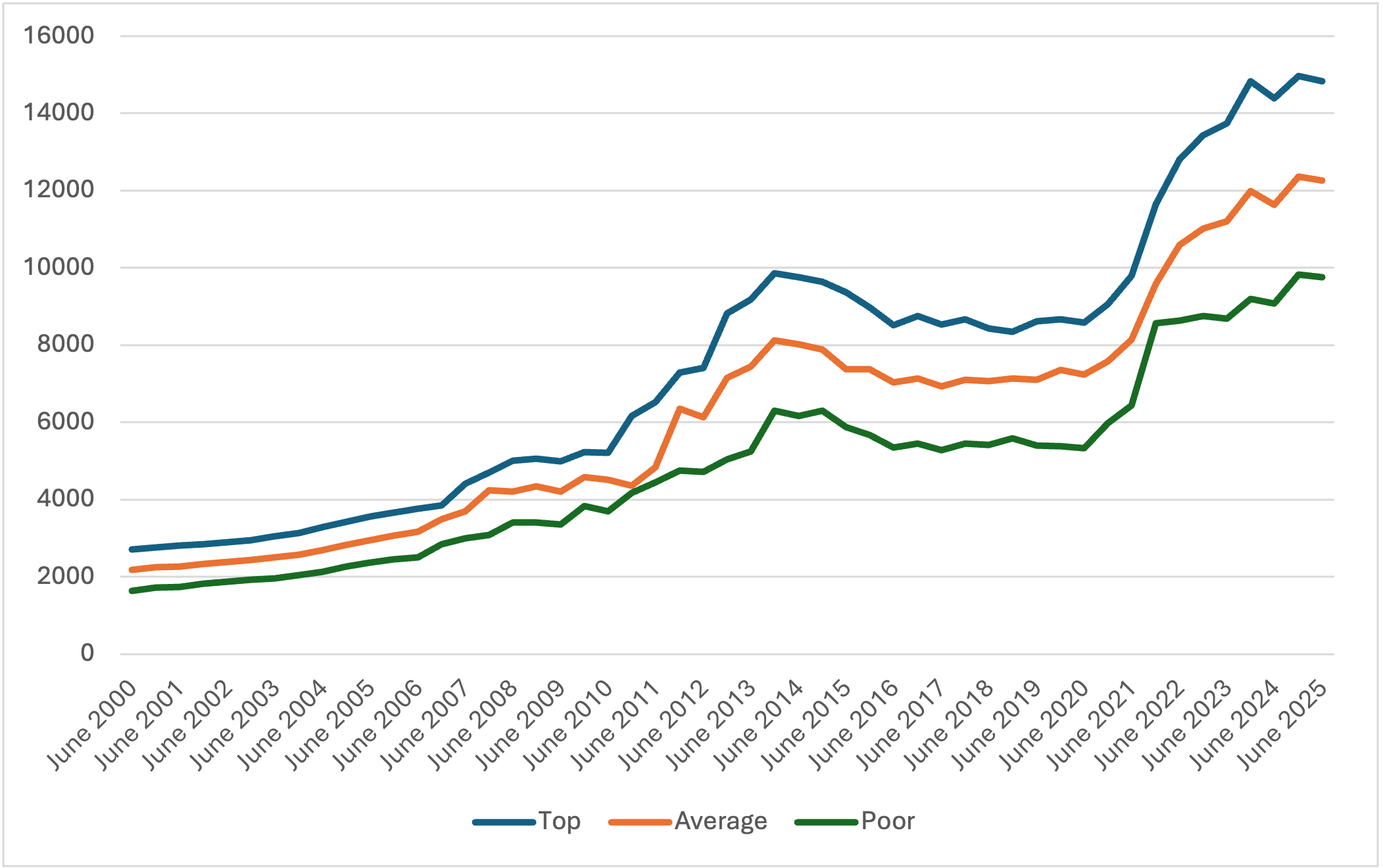

The 2025 Purdue Farmland Value and Cash Rent Survey suggests that Indiana farmland values remain historically strong, though there are some signs of market softening. According to the recent survey, statewide farmland values continued to hold near record levels in 2025 across top-, average-, and poor-quality land. Top-quality farmland averaged $14,826 per acre, a 3.0% increase from June 2024. Average-quality land rose to $12,254 per acre, up 5.4%, while poor-quality farmland increased 7.6% to $9,761 per acre. Although statewide values set new nominal records, the survey also indicates more mixed regional patterns than in recent years. Farmland prices increased in the Northern regions but declined in the Southwest and Southeast, where earlier rapid appreciation appears to have corrected downward.

To provide context for recent changes in farmland values, the long-run trend in Indiana farmland values is shown in Figure 1 below.

Figure 1

Indiana Farmland Price Trend (2000-2025)

Market participants reported that farmland values softened in late 2024 but rebounded modestly during early 2025. A key factor supporting higher values was development pressure, particularly related to solar projects, commercial and industrial expansion, and emerging data-center activity. Respondents emphasized that these effects could spill across county lines through 1031 exchanges and broader regional competition for land. Recreational land values were also notably strong, increasing 18% from 2024 to 2025.

Despite these upward influences from developmental and land conversion pressure, traditional agricultural fundamentals exerted measurable downward pressure. Net farm income remained weak, commodity prices softened compared to prior years, and interest rates, though stabilizing, continued to limit buyers’ purchasing power. Respondents in the survey consistently rated current farm income, crop prices and interest rates as the most significant negative forces affecting the farmland market.

A brief external check comes from the Federal Reserve of Chicago, which reported that Indiana farmland values increased by 6% year-over-year in 2025. However, the Fed also noted that the prices were mostly flat from quarter to quarter, suggesting that the market might be entering a period of stabilization after several years of rapid gains.

Outlook for 2026

Looking ahead, the most likely scenario for land values in 2026 is sideways to slightly positive movement, with little indication of a major downturn unless interest rates rise sharply or commodity prices weaken further. A rapid decline is unlikely given ongoing margin pressure across crop farms. Instead, the farmland prices are expected to be stable, or slightly higher, with selective appreciation in regions influenced by developmental pressure. Top-quality farmland may experience slower gains due to its sensitivity to commodity prices, while average- and poor-quality land could see firmer demand from local buyers and diversified investors.

Cash Rental Rates

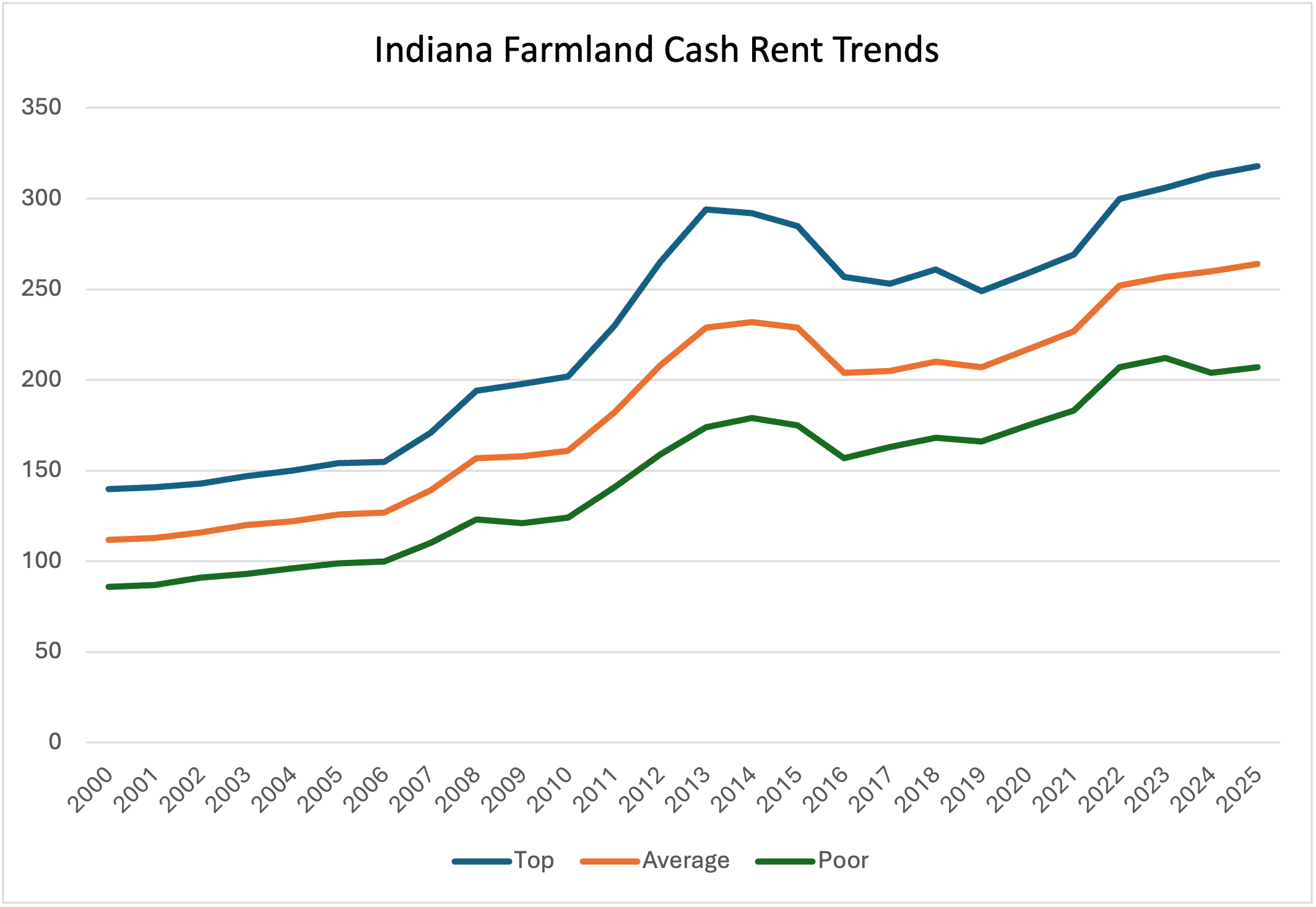

The Cash Rental Survey indicates that statewide cash rental rates increased modestly from 2024 to 2025. Cash rent in Indiana increased 1.7% from $313 to $318 per acre for top-quality farmland. Similarly, average-quality rents increased 1.6% to $264 per acre, and poor-quality rents increased 1.53% to $207 per acre. Similar to land values, the survey suggests that rental rates declined in the Southwest and Southeast but increased across northern and central Indiana, reflecting differences in local profitability and land demand. Rent-to-land-value ratios remained stable, and rental rates per bushel of corn changed very little, indicating cautious adjustments by both landlords and tenants.

To better understand how rental markets have evolved over time, Figure 2 displays the long-term trend in Indiana cash rents.

Figure 2

Indiana Farmland Cash Rent Trend (2000-2025)

2026 Crop Cost & Return projections suggest that producers may continue to face tight margins, with lower expected corn and soybean prices, tight operating margins and persistently high input costs contributing to continued pressure on farm profitability. These conditions align with survey respondents’ views that current and expected income levels remain among the most significant negative forces in the land market.

Outlook for 2026

Based on survey responses and margin expectations, cash rental rates in 2026 are expected to be stable to slightly lower. With tighter margins and uncertain commodity prices, tenants have limited ability to bid higher rents, suggesting rents will likely be stable or decline slightly, except in areas supported by development activity or other non-agricultural land uses.

![]()

![]()

![]()

![]()

![]()