Producers bullish about farmland values amid strong current conditions

Producers bullish about farmland values amid strong current conditions. (Purdue/CME Group Ag Economy Barometer/James Mintert)

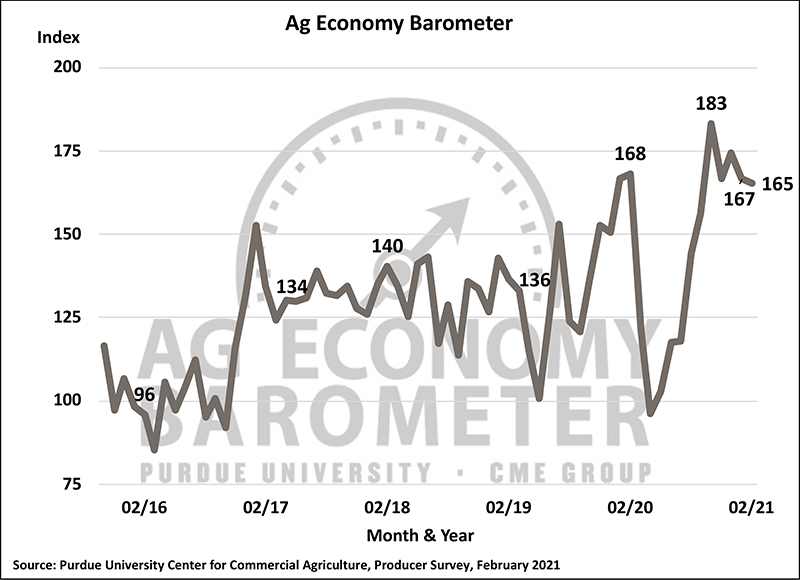

Producers bullish about farmland values amid strong current conditions. (Purdue/CME Group Ag Economy Barometer/James Mintert) Farmers continue to report strong current economic conditions on their farms, according to the February Purdue University/CME Group Ag Economy Barometer. While the overall reading for the Ag Economy Barometer changed very little compared to January, down 2 points to a reading of 165 in February; the Index of Current Conditions remained near its all-time high at a reading of 200. Meanwhile, the Index of Future Expectations continued a four-month decline, down 20% from its October peak, to a reading of 148.

The Ag Economy Barometer is calculated each month from 400 U.S. agricultural producers’ responses to a telephone survey. This month’s survey was conducted Feb. 15-19.

“The ongoing strength in ag commodity prices and farm income continue to support producers’ perspective on current conditions,” said James Mintert, the barometer’s principal investigator and director of Purdue University’s Center for Commercial Agriculture. “At the same time, concerns about possible policy changes affecting agriculture, and eroding confidence in future growth in ag trade, continue to weigh on producers’ future expectations.”

Producers are very bullish about farmland values. Fifty-one percent of respondents in February said they expect farmland values to rise during the next year, up 8 points from the January survey. U.S. farmers were also optimistic about the long-run trend in farmland values, as 62% of respondents indicated farmland values are likely to rise over the next five years.

That same bullishness spilled over into expectations for rising farmland cash rental rates in 2021. In February, more producers (36%) now say they expect cash rental rates to increase, compared to just 18% who felt that way in December. Those expecting rates to remain unchanged fell from 75% to 61%, the decrease primarily due to more producers’ expecting rental rates to increase.

The percentage of farms expecting to see a better financial performance in 2021 compared to the prior year has been rising since last summer and on the February survey reached 37%, up 4 points from January and 25 points higher than last July. When asked about their perception of the most critical risk facing their operation, 29% ranked production, up 8 percent from February 2020, and 18% ranked financial risk, down 8% from one year ago.

Each winter the barometer survey asks respondents about plans for growth on their farms. This winter: Fifty percent of commercial-scale farms reported that they either have no plans to grow or plan to exit/retire in the next five years; 17% expect their farm operation to grow at a rate of less than 5% annually; 25% expect their operation to grow 5%-10% annually; and 9% expect their farm to grow more than 10% per year. Overall, Mintert said, these results point toward continued consolidation in the farm sector.

Although producers are optimistic about the current situation on their farms, confidence in the future continues to erode. Reasons behind the 20% decline in the Index of Future Expectations that has taken place since October appear centered on concerns about the long-term future for agricultural trade and uncertainty about a variety of policies affecting agriculture. In February, only 45% of farmers expected ag exports to increase over the next 5 years, down from 65% in October. The percentage expecting a favorable outcome to the U.S. trade dispute with China is also down, 37% in February compared with 65% in October.

“Even though we have seen a recent ‘ramp-up’ in ag exports to China, producers remain worried about the future of ag trade,” said Michael Langemeier, associate director of the Center for Commercial Agriculture. “They are also concerned about the possibility of more restrictive environmental regulations as well as higher estate and income taxes, all expressed on previous barometer surveys. Uncertainty about all these factors appears to be the motivation for the divergence between farmers’ perspective on the current versus the future situation.”

Interest in alternative protein sources has increased markedly over the last year. Respondents on the February survey were asked several questions to learn about their perspectives on the possible impact of alternative proteins on U.S. agriculture. More than half of producers indicated they expect to see alternative protein sources increase market share in the years ahead (55% expect a total protein market share of up to 10%; 15% expect total market share to exceed 10%) and, indicated that if the market share becomes significant, they think it’s likely to reduce aggregate farm income.

Read the full Ag Economy Barometer report at https://purdue.ag/agbarometer. The site also offers additional resources – such as past reports, charts and survey methodology – and a form to sign up for monthly barometer email updates and webinars.

Each month, the Purdue Center for Commercial Agriculture provides a short video analysis of the barometer results, and for even more information, check out the Purdue Commercial AgCast podcast. It includes a detailed breakdown of each month’s barometer, in addition to a discussion of recent agricultural news that impacts farmers. Available now.

The Ag Economy Barometer, Index of Current Conditions and Index of Future Expectations are available on the Bloomberg Terminal under the following ticker symbols: AGECBARO, AGECCURC and AGECFTEX.

About the Purdue University Center for Commercial Agriculture

The Center for Commercial Agriculture was founded in 2011 to provide professional development and educational programs for farmers. Housed within Purdue University’s Department of Agricultural Economics, the center’s faculty and staff develop and execute research and educational programs that address the different needs of managing in today’s business environment.

About CME Group

As the world’s leading and most diverse derivatives marketplace, CME Group (www.cmegroup.com) enables clients to trade futures, options, cash and OTC markets, optimize portfolios, and analyze data – empowering market participants worldwide to efficiently manage risk and capture opportunities. CME Group exchanges offer the widest range of global benchmark products across all major asset classes based on interest rates, equity indexes, foreign exchange, energy, agricultural products and metals. The company offers futures and options on futures trading through the CME Globex® platform, fixed income trading via BrokerTec and foreign exchange trading on the EBS platform. In addition, it operates one of the world’s leading central counterparty clearing providers, CME Clearing. With a range of pre- and post-trade products and services underpinning the entire lifecycle of a trade, CME Group also offers optimization and reconciliation services through TriOptima, and trade processing services through Traiana.

CME Group, the Globe logo, CME, Chicago Mercantile Exchange, Globex, and E-mini are trademarks of Chicago Mercantile Exchange Inc. CBOT and Chicago Board of Trade are trademarks of Board of Trade of the City of Chicago, Inc. NYMEX, New York Mercantile Exchange and ClearPort are trademarks of New York Mercantile Exchange, Inc. COMEX is a trademark of Commodity Exchange, Inc. BrokerTec, EBS, TriOptima, and Traiana are trademarks of BrokerTec Europe LTD, EBS Group LTD, TriOptima AB, and Traiana, Inc., respectively. Dow Jones, Dow Jones Industrial Average, S&P 500, and S&P are service and/or trademarks of Dow Jones Trademark Holdings LLC, Standard & Poor’s Financial Services LLC and S&P/Dow Jones Indices LLC, as the case may be, and have been licensed for use by Chicago Mercantile Exchange Inc. All other trademarks are the property of their respective owners.

Featured Stories

Land plants have spent nearly half a billion years honing a vast array of metabolic skills that...

Coffee makers are everywhere — from kitchens to office break rooms — brewing up...

Ask Purdue biochemistry students in the College of Agriculture about their experience and their...

By learning how to cut through the hype and focus on what truly matters, you can shop smarter...

Channing Arndt, research professor in agricultural economics and director of the Global Trade...

Daniel Szymanski and his former postdoctoral scholar Youngwoo Lee, lead author on their paper...