Indiana Pasture Land, Irrigated Farmland, Hay Ground, and On-Farm Grain Storage Rent

August 8, 2015

PAER-2015-09

Craig L. Dobbins, Professor of Agricultural Economics and Kim Cook, Research Associate

![]()

![]()

![]()

![]()

![]()

Estimates for the rental value of irrigated farmland, pasture land, hay ground, and on-farm grain storage in Indiana are often difficult to find. For the past several years, questions about these items have been included in the Purdue Farmland Value Survey. The values from the June 2015 survey are reported here. Because the number of responses for some items is small, the number of responses is also reported.

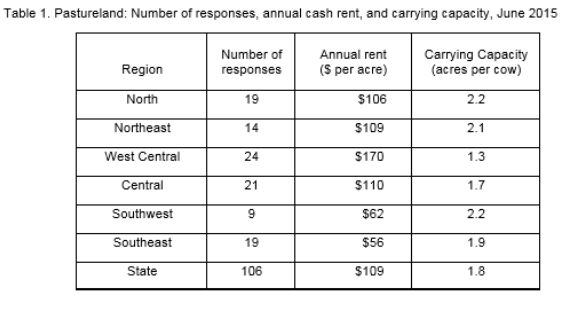

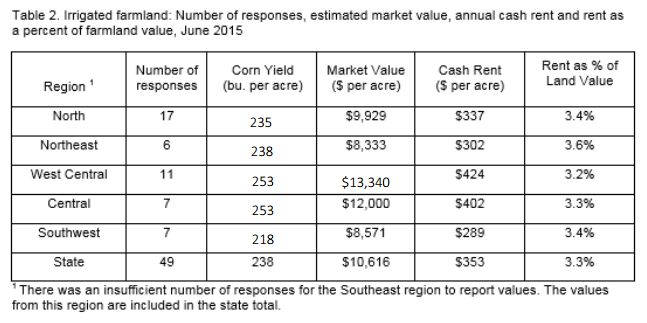

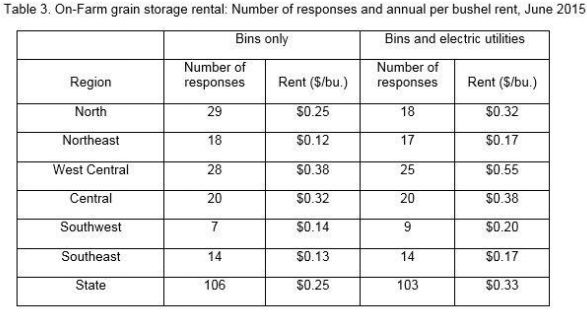

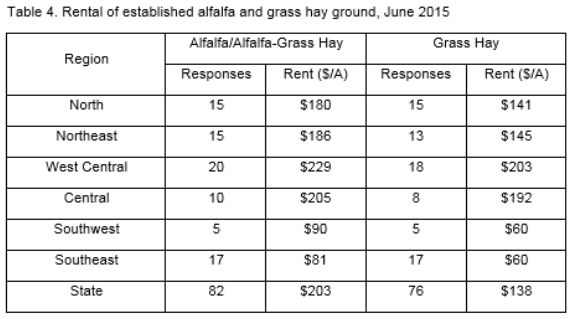

Averages for pasture rent, the market value of and cash rent for irrigated farmland, and the rental of on-farm grain storage are presented in Tables 1, 2, and 3, respectively. The rental rate for grain bins includes two situations; one for just the bin and a second for the bin and utilities. Table 4 (page 11) provides information about the rental rate for established alfalfa-grass and grass hay ground.

Information from prior years’ surveys can be found in the Purdue Agricultural Economics Report archive.

This information can be found in the August issue beginning in 2006.

Table 1: Pastureland: Number of responses, annual cash rent, and carrying capacity, June 2015

Table 2. Irrigated farmland: Number of responses, estimated market value, annual cash rent and rent as a percent of farmland value, June 2015

Table 3. On-Farm grain storage rental: Number of responses and annual per bushel rent, June 2015

Table 4. Rental of established alfalfa and grass hay ground, June 2015

![]()

![]()

![]()

![]()

![]()