The March 2026 Producer Price Index: Reading the Food Price Pipeline

April 16, 2026

PAEPB-2026-05

Ken Foster, Professor of Agricultural Economics and Director, Purdue Farm Policy Study Group; Bernhard Dalheimer, Assistant Professor of Macroeconomics and Trade

![]()

![]()

![]()

![]()

![]()

Key Takeaways

-Mid-March data collection window — a critical caveat: The PPI survey is conducted on the Tuesday of the week containing the 13th. March prices, therefore, reflect conditions as of approximately March 10 — about ten days after conflict onset. What the data shows is the cost environment as it stood in mid-March, not today. The April PPI (May 13) is the first full-month conflict-era reading.

-February PPI — the pre-conflict baseline — was already under stress, with final demand foods rising 2.4% and processed intermediate energy goods up 5.4% before a single barrel of conflict-disrupted oil reached market. Some of this reflects anticipatory risk pricing as markets responded to the protracted public escalation — Trump’s threats, the military buildup, and the February 20 ultimatum — before the conflict began.

-Ten days of conflict-era pricing are clearly visible in March. Final demand energy jumped 8.5%; processed energy goods for intermediate demand surged 11.3% — the largest advance since May 2022. Diesel fuel, the food system’s key logistics input, was the dominant driver.

-Retail food prices fell 0.3% in March — a price-stickiness signal, not a safety signal. Food wholesale margins collapsed 6.0%, confirming that distributors may be absorbing upstream cost increases rather than passing them through. That absorption has limits.

-The production flow data places the cost wave at Stage 3, one node from retail. Stage 3 goods inputs posted their largest monthly advance since August 2023. Consumer-level grocery price acceleration is projected for the May–August 2026 window.

-Natural gas fell sharply, providing a partial, and likely, temporary offset for electricity-intensive food processing. Substitution effects and global LNG market tightening make a rebound probable if the conflict persists.

A Critical Caveat: What the Data Measures — and When

The Bureau of Labor Statistics collects Producer Price Index (PPI) prices on the Tuesday of the week containing the 13th of each month. The March survey date was March 10. The Iran conflict began on February 28, making March 10 exactly ten days post-onset. The February survey date was February 10 — eighteen days before the conflict began – but well within the window of pre-conflict rhetoric and U.S. troop buildup in the region.

This timing helps to interpret both sets of PPI data with respect to food and agriculture. February PPI is the pre-conflict baseline, and March PPI captures the first ten days of Iran conflict-era prices, not only a one-day market panic reaction, but a full week and a half of supply-chain costs operating under active Strait of Hormuz disruption and international oil price and domestic motor fuels price increases. The April PPI release on May 13 will be the first full-month conflict reading and the most important upcoming data event.

One additional caveat applies to the February baseline. The pre-conflict escalation was protracted and public. Trump issued explicit threats to Iran in January, a second aircraft carrier was deployed to the region by mid-February, and a formal 10-day ultimatum was delivered on February 20. In addition, some economists have speculated that tariff effects may have begun impacting this data in late 2025 and early 2026. Commodity options markets had already embedded a modest war risk premium — estimated at roughly $4 per barrel for crude oil — by mid-January, following Trump’s Iran tariff announcement on January 12. This means the January and February PPI energy readings cannot be cleanly separated into “conflict” and “non-conflict” components. Some unknown portion of the pre-conflict energy cost escalation reflects anticipatory market pricing as well as a possible underlying economic trend related to residual tariff pass-through or other factors.

The February Baseline: Cost Pressure Was Already Building

With that caveat noted, the February PPI reveals a supply chain already under meaningful cost stress entering the conflict.

Final demand foods rose 2.4% in February alone — the largest single-month food price increase in the recent data run — before the conflict began. Processed energy goods for intermediate demand rose 5.4%, and Stage 2 goods inputs — encompassing petroleum refineries, natural gas distribution, and cattle ranching — surged 4.7%. The 12-month final demand PPI had reached 3.4% through February, re-accelerating across late 2025 and early 2026.

Whether driven by underlying economic trends related to tariffs or other factors, anticipatory market pricing, or both, the practical consequence is that the food supply chain entered the Iran conflict with less cost-absorbing capacity than it would have had under tranquil pre-conflict conditions. Any margin cushion available to absorb the energy shock without retail pass-through was already being consumed.

The March Data: Ten Days of Conflict-Era Energy Prices

The headline March number — final demand PPI up 0.5% for a 12-month advance of 4.0%, the largest since February 2023 — understates what is happening at the supply chain’s upstream nodes. The conflict-era price signal is concentrated in energy and logistics, not yet in consumer-facing food prices.

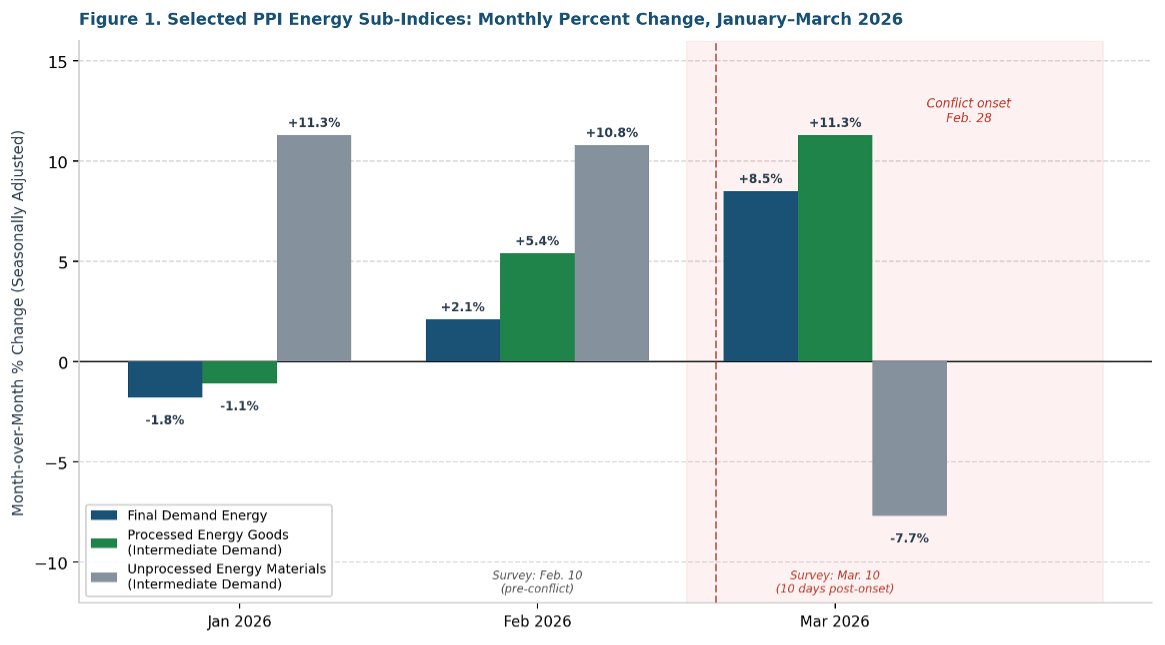

Final demand energy jumped 8.5% in March. Processed energy goods for intermediate demand surged 11.3% — the largest monthly increase since May 2022. Diesel fuel accounted for more than half of that advance on its own. Gasoline, jet fuel, and home heating oil also rose. The price of primary basic organic chemicals — the petrochemical feedstock for food packaging — also increased.

These figures reflect just ten days of market pricing under active Strait of Hormuz disruption. Figure 1 illustrates the energy cost trajectory across January through March, distinguishing the pre-conflict trend from the conflict-era surge.

Figure 1

Selected PPI Energy Sub-Indices: Monthly Percent Change, January-March 2026

Figure 1. Selected PPI energy sub-indices, monthly percent change, January–March 2026 (seasonally adjusted). Final demand energy and processed energy goods for intermediate demand show sharp conflict-era acceleration in March. Unprocessed energy materials fell in March, driven by the collapse in domestic natural gas prices. Conflict onset: February 28. March survey date: March 10 (~10 days post-onset). Source: U.S. Bureau of Labor Statistics, Producer Price Indexes, April 14, 2026.

Transportation and warehousing services for final demand rose 1.3% in March, with truck transportation of freight specifically noted as increasing. This is the logistics cost channel beginning to register at the stage immediately adjacent to consumer prices. Because diesel powers every truck moving food from farm to processor to warehouse to retail store, the 42% surge in intermediate-demand diesel fuel is the clearest available early signal of food logistics cost escalation building in the pipeline.

Retail Food Prices: Stable for Now — Not Forever

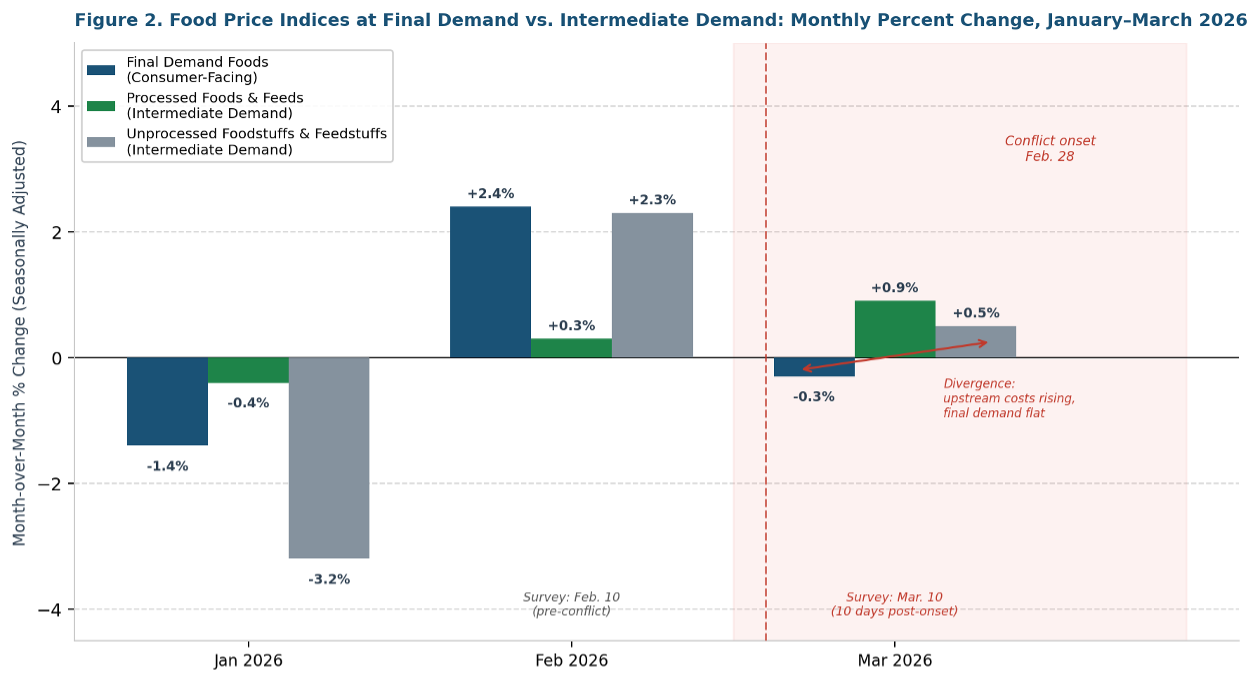

Final demand food prices fell 0.3% in March. While this may be misread as evidence that the conflict is not affecting food prices, it is likely the result of a price stickiness dynamic, which has been well documented in the economic literature.

More precisely, the decline is substantially driven by a 10.7% drop in fresh and dry vegetables, most of which is a seasonal effect, reflecting normal early-spring supply normalization. Strip this out, and the underlying March food price trajectory is firmer than the headline suggests. Meat prices even increased at the final demand stage.

The most informative signal is the 6.0% collapse in food and alcohol wholesaling margins. Distributors appear to be absorbing conflict-era energy and logistics costs rather than immediately passing them through. This is the first phase of the transmission sequence that the price transmission literature describes as “sticky” pricing behavior (Peltzman, 2000; Meyer and von Cramon-Taubadel, 2004). Once the absorption limit is reached, pass-through tends to arrive sharply. However, margins of the alcohol distribution sector are notoriously larger than in other food sectors (e.g., Conlson and Rao, 2024). Food retailing margins increased in March, meaning retailers appear to already be defending their own margins even as wholesale costs rise — a divergence consistent with the competitive dynamics that delay initial price increases and then slow subsequent decreases.

Figure 2 illustrates the core divergence: upstream food commodity costs are rising at intermediate stages of demand, while final-demand food prices remain flat or negative.

Figure 2

Food Price Indices at Final Demand vs. Intermediate Demand: Monthly Percent Change, January-March 2026

Figure 2. Food price indices at final demand versus intermediate demand stages, monthly percent change, January–March 2026. The March divergence between rising upstream food costs (processed and unprocessed intermediate stages) and flat final demand food prices is a classic price-stickiness signal, not evidence of insulation from the conflict. Conflict onset: February 28. March survey date: March 10. Source: U.S. Bureau of Labor Statistics, Producer Price Indexes, April 14, 2026.

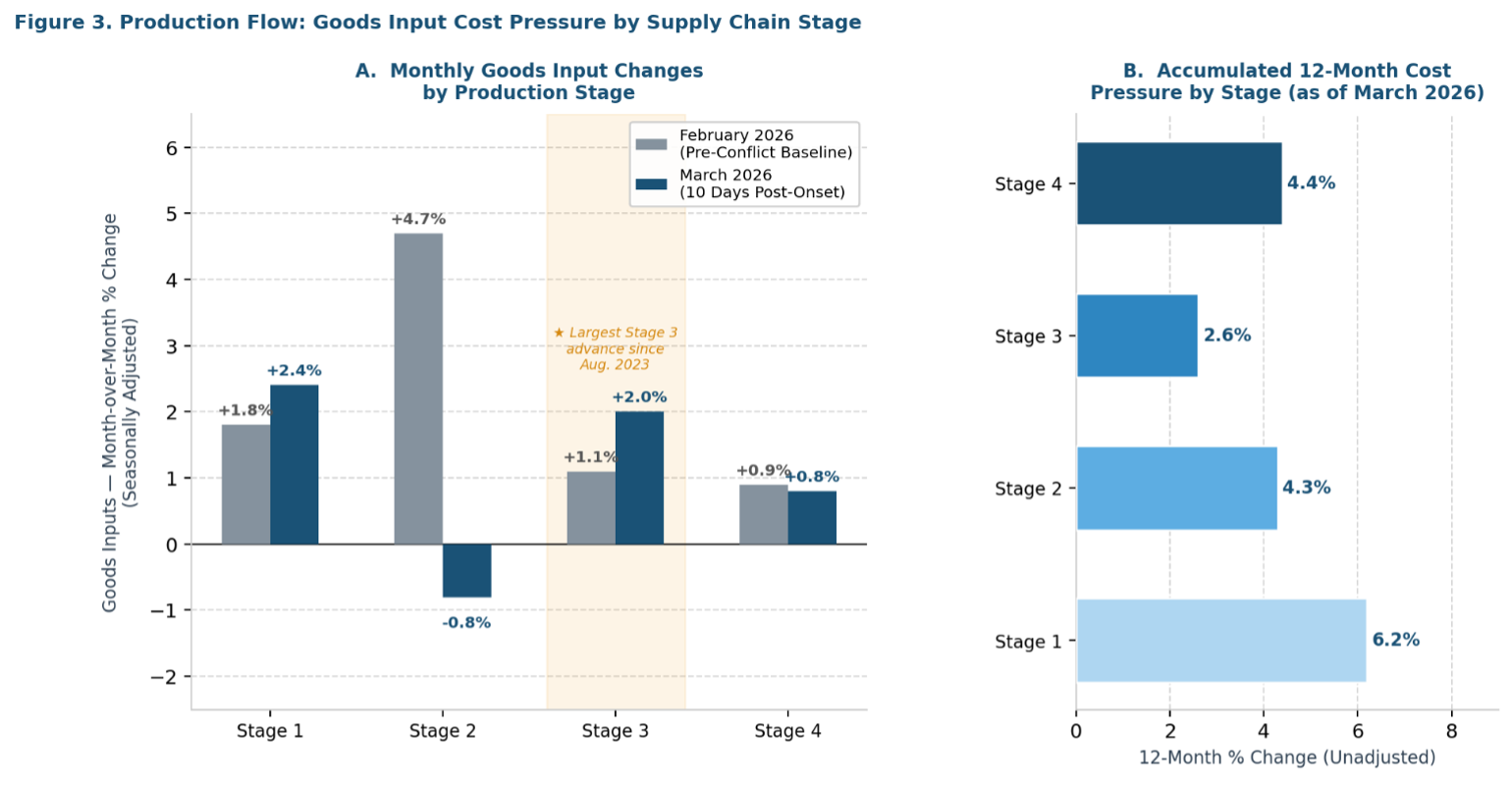

The Production Flow: Where the Cost Wave Stands as of Mid-March

The BLS intermediate demand indexes, organized by production stage, provide the most precise available picture of where the energy cost shock sits within the food supply chain. Stage 4 outputs flow directly into final consumer demand, and Stage 1 is the earliest extractive/farm-input stage.

Reading February and March together is key to determining how far the shock has propagated. In February — the pre-conflict baseline — Stage 2 goods inputs had already surged 4.7% in the pre-conflict economy. Notably, tariff pass-through could have played a major role, especially via primary basic organic chemicals, which have been subject to high tariffs for most of 2025 and all of 2026. This pre-loading, whether trend-driven or anticipatory, gave the cost wave a head start even before the conflict began.

In March, ten days of conflict-era prices advanced the wave materially into Stage 3. Stage 3 goods inputs rose 2.0% — the largest monthly advance since August 2023 — with diesel fuel, raw milk, gasoline, and organic chemicals cited as primary drivers. Stage 3 encompasses animal slaughtering and processing and wholesale trade: the supply chain nodes immediately upstream of grocery retail. Stage 4 goods inputs rose 0.8%, indicating the leading edge of the wave is beginning to register at the final-demand stage.

The 12-month accumulated cost pressure tells the fuller story: Stage 1 is up 6.2% (the largest increase since November 2022); Stage 4 is up 4.4% (the largest increase since early 2023). Importantly, the conflict has not created this pipeline, but so far only accelerated the rate of fill. Figure 3 shows both the monthly dynamics and the accumulated 12-month pressure by stage. One can visualize pre-conflict price pressure that has reached stage 4, and conflict-induced pressure that is showing up in stage 1 and possibly, to some extent, in stage 2.

Figure 3

Production Flow: Goods Input Cost Pressure by Supply Chain Stage

Figure 3. Production flow goods input cost pressure by supply chain stage. Panel A: monthly goods input percent changes for February 2026 (pre-conflict baseline, including anticipatory risk pricing) and March 2026 (~10 days post-onset). Stage 3 advance in March was the largest since August 2023. Panel B: 12-month accumulated goods input cost pressure by stage as of March 2026. Darker shading indicates proximity to final consumer demand. Stage 2 March decline driven by natural gas price collapse; see text. Source: U.S. Bureau of Labor Statistics, Producer Price Indexes, April 14, 2026.

The production flow data are most usefully read as a single crude oil shock manifesting at multiple cost nodes simultaneously, but at different intensities and with different timing depending on how directly each stage’s input cost structure is exposed to petroleum prices. Stages 1 and 2 — the extractive, refining, and raw materials stages — carry the strongest conflict-era signal. Stage 1’s 12-month accumulated goods input pressure reached +6.2% through March, the largest since November 2022, driven in March by diesel, gasoline, crude petroleum, and organic chemicals; Stage 2’s 12-month reading of +4.3% remains elevated despite the March natural gas collapse masking its underlying petroleum exposure. These upstream stages reflect the direct impact of conflict-era energy pricing hitting operating costs at the point of extraction and initial processing. Stages 3 and 4, by contrast, carry readings that are more consistent with the pre-conflict (such as residual tariff pass through) and anticipatory pipeline charging described earlier in this brief: Stage 3’s 12-month accumulated pressure (+2.6%) is the weakest of the four stages despite its notable March monthly advance, and Stage 4’s monthly reading (+0.8%) likely reflects the pre-conflict Stage 2 surge from February now arriving at the retail-adjacent stage. This gradient — earlier stages more directly conflict-driven, later stages more reflective of anticipatory forces — does not imply two sequential waves so much as a supply chain in which conflict-era energy costs are still working their way forward through a pipeline that was already charged. The distributed-lag implications (Baumeister and Kilian, 2014; Reed et al., 2002) are significant: with 12-month pressure running between +2.6% and +6.2% across all four stages simultaneously, and the conflict-driven upstream surge at Stages 1 and 2 still needing to transit through two to three additional production nodes before reaching retail, the data point to a sustained and reinforcing sequence of food price pressure rather than a single arrival event.

Thus, Consumer-level grocery price impacts should be expected to emerge and accumulate progressively over a period extending from late spring through at least late 2026 — and potentially into 2027. The extent depends on how long the conflict persists and thus how long and how strongly oil prices are elevated, as well as how comfortable the margins of distributors and processors are and the extent to which they will be able to use them as cushion.

The Natural Gas Offset: Real but Likely Temporary

Unprocessed natural gas fell 51.7% in March, and natural gas to electric utilities fell 7.2%. These declines provide a partial offset for electricity-intensive food-processing operations — refrigeration, freezing, sterilization, and baking — that depend on natural gas or gas-fired electricity.

The explanation is structural: the Strait of Hormuz disruption constrains oil and LNG tanker routes, but domestic U.S. natural gas supply — priced at Henry Hub — is not directly exposed to the same chokepoint. In the first ten days of the conflict, domestic gas markets separated from crude oil markets because U.S. export infrastructure was already running at full capacity and therefore could not address demand elsewhere. In addition, substantial stocks were on hand in the U.S., having been accumulated expecting normal winter heating demand, whereas mild weather ended up prevailing that month.

The LNG price offset is sector-specific: it does not mitigate the diesel shock hitting food transportation, nor the petrochemical shock affecting packaging. And if the conflict persists, industrial demand substitution away from petroleum products toward natural gas, combined with global LNG market tightening, will drive domestic natural gas prices back upward. The March natural gas decline is a temporary cushion, not a structural counterweight.

Three Indicators to Watch

- April PPI release, May 13. The first full-month conflict-era PPI. A monthly increase in processed foods and feeds for intermediate demand above 1.5–2.0% would signal the pipeline is advancing toward the central scenario in Foster and Dalheimer PAEPB-2026-02. Stage 3 and Stage 4 goods input readings will be equally telling.

- USDA ERS Food Price Outlook, May. The first consumer-level corroboration of whether the PPI pipeline is delivering into retail prices. Meaningful acceleration in processed foods will be the earliest visible grocery-level signal.

- Crude oil and natural gas prices through April. Whether food manufacturing and logistics contracts reprice at conflict-era energy costs depends on whether elevated energy prices persist through April. A resolution before mid-April limits the retail food price impact to the lower range of Foster and Dalheimer PAEPB-2026-02 scenarios. Sustained disruption through the spring contracting season puts the trajectory toward the central and high scenarios.

- Conflict duration and tension. Will the current ceasefire continue and expand into a settlement that allows traffic in the Strait of Hormuz to return to pre-conflict norms? If so, how soon will this transpire?

References and Data Sources

Baumeister, C., and Kilian, L. (2014). “Do oil price increases cause higher food prices?” Economic Policy, 29(80), 691–747. https://doi.org/10.1111/1468-0327.12039

BloombergNEF. (2026, January 16). Oil Can Hit $91 a Barrel in Late 2026 on Iran Disruption. https://about.bnef.com/insights/commodities/oil-can-hit-91-a-barrel-in-late-2026-on-iran-disruption/

Conlon, C., & Rao, N. L. (2024). The cost of curbing externalities with market power: Alcohol regulations and tax alternatives (No. w30896, p. 20230088884). Cambridge, MA, USA: National Bureau of Economic Research.

Foster, K., and Dalheimer, B. (2026, March). The Iran Conflict and Consumer Food Prices: A Broad but Lagged and Sticky Shock. PAEPB-2026-02. https://ag.purdue.edu/commercialag/home/paer-article/the-iran-conflict-and-consumer-food-prices-a-broad-but-lagged-and-sticky-shock

Foster, K., and Dalheimer, B. (2026, March). The Iran Conflict, Energy Prices, and U.S. Farm Profitability: A Balanced Assessment. PAEPB-2026-01, https://ag.purdue.edu/commercialag/home/paer-article/the-iran-conflict-energy-prices-and-u-s-farm-profitability-a-balanced-assessment/

Meyer, J., and von Cramon-Taubadel, S. (2004). “Asymmetric price transmission: A survey.” Journal of Agricultural Economics, 55(3), 581–611. https://doi.org/10.1111/j.1477-9552.2004.tb00116.x

Peltzman, S. (2000). “Prices rise faster than they fall.” Journal of Political Economy, 108(3), 466–502. https://doi.org/10.1086/262126

Reed, A., Elitzak, H., and Wohlgenant, M. (2002). Retail-Farm Price Margins and Consumer Product Diversity. USDA ERS Technical Bulletin No. 1899.

U.S. Bureau of Labor Statistics. (2026, April 14). Producer Price Indexes — March 2026. USDL 26-0619. https://www.bls.gov/news.release/archives/ppi_04142026.htm

![]()

![]()

![]()

![]()

![]()