“What to Watch” in Dairy Markets in 2026

March 23, 2026

PAER-2026-10

Authors: Nicole Olynk Widmar, Department Head and Professor of Agricultural Economics; Joscelyn Pilcher, Undergraduate Research Assistant

![]()

![]()

![]()

![]()

![]()

Total milk production for 2025 was forecasted (per December 2025 ERS-USDA Outlook Report) at 231.4 billion pounds, which was unchanged from the previous projection. Upward movement in dairy cattle numbers and milk per cow fueled this increase. Expectations for 2026 are for a slight reduction in the national herd to 9.555 million head, but with milk yield per cow to increase by 10 pounds, this brings the 2026 forecast to 234.1 billion pounds.

The national dairy herd peaked at 9.575 million head in the fourth quarter of 2025, according to the ERS-USDA December Outlook Report, and has gradually increased since October 2024. Even without growth (and a slight decline) in total head, improvements in production efficiency are expected to support an increase in milk production, as herd size decreases.

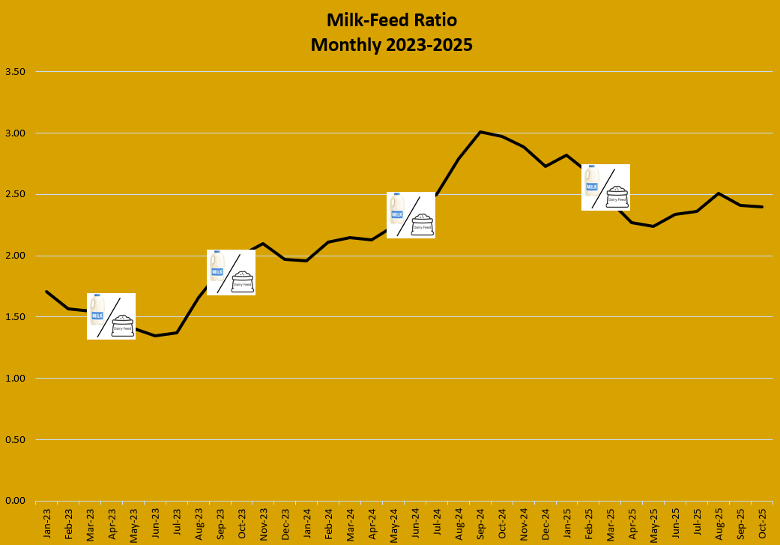

Looking back over 2023 through today, the milk-feed price ratio peaked at 3.00 in September and October of 2024 and has since been on a slow decrease through 2025, flattening off heading into Q4 of 2025. Lower feed costs have bolstered more favorable milk-feed ratios. However, as milk prices continue to fall in 2026, and can be expected to lower to $18.75 – $20.40/cwt (from ~$21.35 in 2025) per the ERS-USDA December Outlook Report, margins are likely to be squeezed further, even with sustained cheaper feed inputs.

While it seems that discussions about Highly Pathogenic Avian Influenza (HPAI) detections have slowed down to some degree, there is still risk, especially in migratory seasons. While production loss in infected dairy herds remains a concern, the more imminent threat in 2026 is regulatory and trade partner reactions to herd infections. There isn’t any new guidance at this time, but the 2024 federal order can be accessed here. The USDA has five steps of Testing, Biosecurity, Collaboration, and Prevention that are available here. As the USDA is progressing further, there should be a watch for new testing requirements as well as new interstate movement restrictions that could disrupt markets.

Domestic use for dairy products for January through August of 2025, compared to the same period in 2024, saw an increase for butter, skim milk products, lactose, and whey protein, while there was a decline for cheese and dry whey. Demand remains strong, but supplies are also abundant, so buyers aren’t feeling pressure. As milk production remains strong, we have a lot of milk domestically and in global supplies, and while demand is strong, that strength is in consistent demand more so than major growth. And, growth in demand varies across products.

A variety of factors from adjacent markets, including feed and beef markets, will fuel conversations this year. Strength in beef prices might play into culling decisions, and we know that calf and heifer prices will respond, but attempting to foresee beef markets far enough out to make meaningful on-farm decisions remains a challenge in the current environment and in the context of rapidly evolving regulatory and trade relationships. Policy changes, both domestically focused and trade-focused abroad, remain top of mind for many heading into 2026. Changing dietary recommendations by the U.S. government and associated agencies largely favor consumption of more protein from meat and dairy, but how recommendations are implemented and how fast the public does or does not adapt is yet to be seen.

![]()

![]()

![]()

![]()

![]()