January 1, 2015

The Great Margin Squeeze: Strategies for Managing Through the Cycle

![]()

![]()

![]()

![]()

![]()

After many years of high commodity prices and strong profitability, the landscape in the row-crop sector has shifted dramatically. Today, farmers are facing a substantial margin squeeze. Purdue’s early estimates of the 2015 budget for operations on average-quality Indiana farmland projected a loss ranging from $156 to $317 per acre. The declines in commodity prices have not been met with subsequent reductions in costs, creating the potential for a very serious margin squeeze.

In the long run, it is likely that a stabilized level of profitability will result through one or some combination of these three scenarios: 1.) variable costs moderate through eventual reduction in farmer demand for inputs, 2.) fixed costs decline through reductions in fixed asset demand and values, and/or 3.) output prices may improve. While it is nice to think about a long-run equilibrium, it is very important that farmers and everyone in the agricultural value chain prepare for what is likely to be an uncomfortable process of getting to the long run. The purpose of this article is to provide perspective on the situation and some management strategies that farmers can use as margins contract.

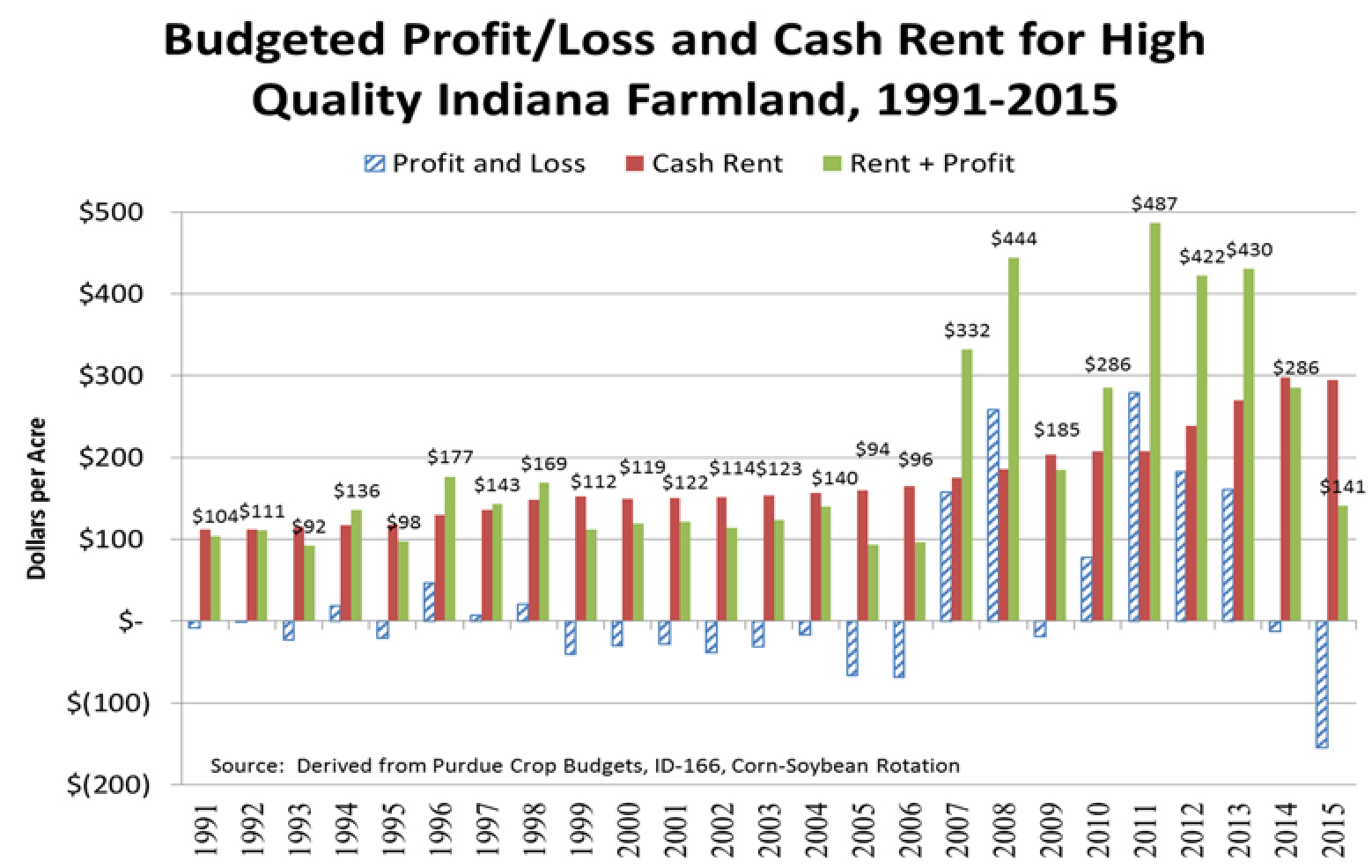

The immediate cause of the current squeeze is the decline in crop revenues. However, the longer-term cause is that the costs of production have increased tremendously in recent years. As commodity prices have fallen costs have been slow to adjust. One can see the extent of the commodity price squeeze that farmers are facing in Figure 1, which shows Purdue’s early estimated budgets for high-quality Indiana farmland in the context of budgets since 1991.

Figure 1. Budgeted Profit and Loss for High-Quality Indiana Farmland, 1991-2015.

The expected level of losses for 2015 are unprecedented over the period from 1991-2015. It is not uncommon that farmers face a potential loss prior to planting. In fact, of the 25 years shown, 15 showed potential economic losses prior to planting. However, none of the budgeted losses were of the magnitude currently expected. Of course, much can happen after the release of the budget. Yields can be better or worse, output prices can be higher or lower than expected, or costs could even fall. However, the magnitude of this potential loss is sobering. So why has this situation arisen?

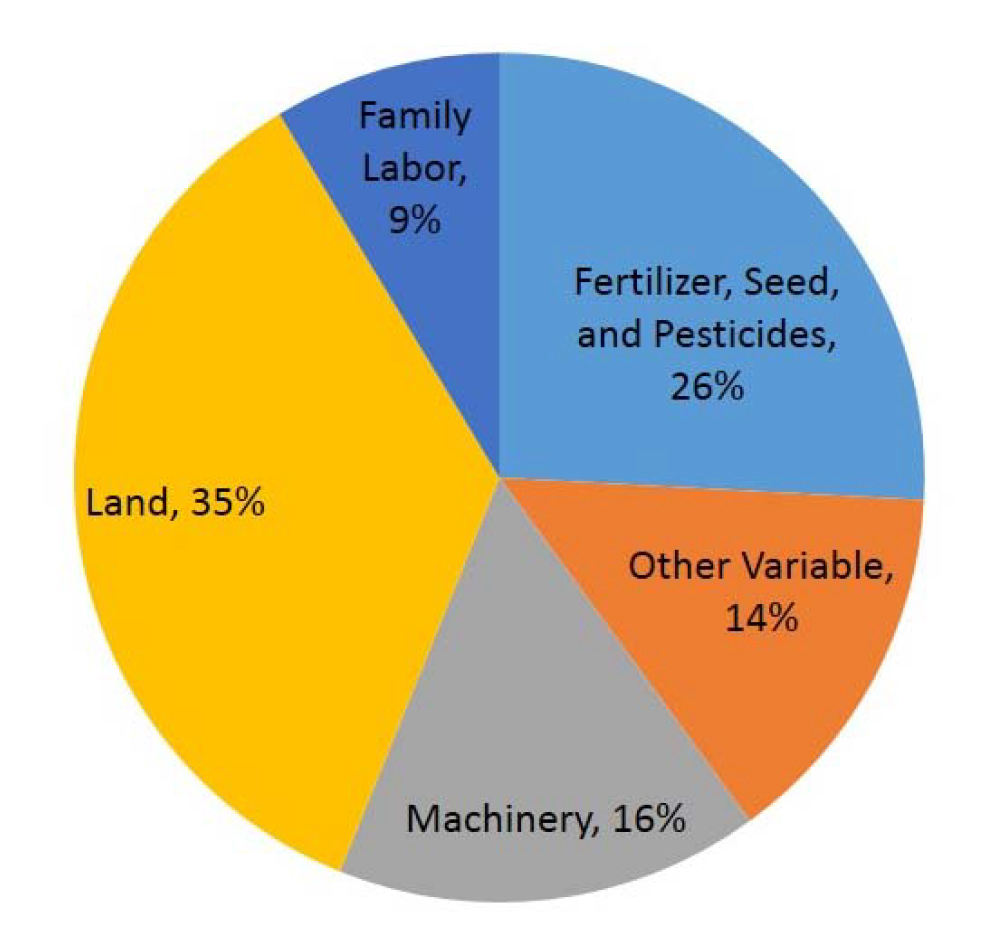

There are a variety of explanations for the squeeze, but a large part of the explanation is due to the overall cost structure of the farming sector. Farms have a high proportion of fixed costs relative to many industries. Figure 2 shows the distribution of budgeted costs, averaged across several years of the Purdue budgets. One can see that less than half (40 percent) of a farmer’s typical costs consist of variable costs such as seed, fertilizer, chemicals, etc. The traditional fixed costs, such as land rent, equipment ownership costs and family labor, make up the remainder of the expense distribution.

Figure 2. Average Annual Distribution of Expected Expenses for 50-50 Corn-Soybean Rotation on High Quality Indiana Farmland, 1991-2014. Source: Derived from Purdue Crop Budgets, ID-166, Corn-Soybean Rotation.

In order to understand why margin squeezes can last for an extended period of time, it is important to think about the input markets that give rise to the variable and fixed costs. Prices in markets for variable inputs such as fertilizers, seed and crop protection chemicals tend to adjust more rapidly than prices for fixed assets. This is because there is considerable competition in these markets and the product life cycles match the production cycle. However, these markets only account for a portion of a farmer’s total costs. Fixed asset markets, such as the land market, tend to adjust more slowly. Rents are frequently not negotiated every year, only a small portion of land sells in any year and equipment has a multi-year life cycle. As a result, the fixed costs tend to adjust more slowly. Since they comprise a large part of total costs,farmers’ margins tend to get squeezed until fixed costs adjust downward.

The downward adjustment in fixed costs is typically painful. It is difficult for farmers to let high-priced leases go. In some cases, they are contractually bound (for at least a year or two) to higher lease payments than can be justified. It is difficult to see land values fall, particularly if they are a key source of borrowing capacity and wealth accumulation in a farming operation. Equipment values also tend to resist downward adjustment as farmers avoid sales and ride out the squeeze with the equipment that they have. Eventually, fixed costs adjust downward and margins return to a more stable level. However, for farmers with high levels of debt service during the adjustment process, the squeeze can make debt repayment difficult, at best. These high fixed costs also mean that farmers are slow to reduce production as prices above variable costs contribute to servicing the fixed costs. This keeps downward pressure on output prices and upward pressure on variable costs of production.

So, in this environment of lower prices and a margin squeeze, what are some strategies that farmers can use to make it through the adjustment period? We offer a few ideas that we believe can help farmers navigate the squeeze.

1. Maintain ample cash reserves and operating credit.

One of the first questions that farmers should ask themselves is how much cash is required to run the business and what level of cash reserves they are comfortable with in the business. Maintaining a strong working capital position (lots of current assets relative to current liabilities) keeps the business stable. When cash reserves dwindle, management attention is quickly diverted from all other tasks to address the immediate need of finding cash to pay bills. Make sure to understand the cash flow needs of your farm operation. When is cash required in the future, and how much? Work closely with your lender to arrange for operating credit ahead of immediate needs.

2. Get fixed costs under control.

The first step in the process is identifying the primary fixed costs that need to be managed. These are typically rents and land costs, depreciation on equipment, family living expenses and interest expenses. One of the biggest challenges in this process is that adjustments in one area can significantly impact the efficiency of the operation. For instance, farms might wish to reduce their equipment expenses through sales of unnecessary equipment. However, it is important to make sure that any equipment sales do not adversely impact the efficiency of your operation. In short, look to make sure that your equipment line is optimally sized for the operation.

Reducing exposure to high-priced cash leases may be another good alternative. If the rented land does not generate a positive contribution margin (if it doesn’t at least cover variable costs plus the rent payment), it is a large drag on the operation. Additionally, the sale of farmland, although difficult, may provide an operation a chance to both reduce cash flow required for principal payments as well as reduce interest expenses.

Another area one should examine is employee expenses. Employees are important parts of the farm team, and it is very critical to think carefully about adding employee expenses at the start of a margin squeeze. Saving on family living expenses can also be important in reducing cash flow needs in a downturn. In this tougher environment, it will be important to carefully consider expenditures in all areas including family living.

3. Carefully evaluate debt structure.

Many times, farmers seek to aggressively pay down debt. This is typically a very good strategy. Where it usually goes awry is when payment terms are set too short, creating debt service obligations that are unrealistic in a margin squeeze. For instance, financing a farmland purchase with a 7- or 10-year mortgage requires income from several parcels of land to support the debt payment. Debt terms should generally match the expected life of the asset. Make sure that an asset’s life and the terms on associated liabilities are appropriately matched. Most farmers’ assets are dominated by farmland. Debt should be structured accordingly.

4. Obtain low costs of production.

It is critical to work to reduce your costs of production to match the lower price levels. Having a low cost of production is the absolute best defense against price declines. How does one do this? There are many, many different strategies that can be used, but the first step in the process is to determine your cost of production. Then, compare the cost of production to benchmarks from record-keeping associations or your agricultural lender. What areas of costs are you doing well with, and what areas do you need to work on? Make sure that you understand both cost composition and total cost per unit of production sold. Then, start identifying areas to work on. Some questions that you should ask along the process are:

- What is your purchasing strategy for inputs? How do your variable costs/input costs compare to other farmers of similar size and scope?

- How well are you doing on asset utilization? Do you have significantly more equipment in your operation than other farmers in similar situations?

- Have you been timely in your operation? Are yields suffering or benefiting from your current level of timeliness? Have you considered alternatives such as custom hire (in or out) as a way to improve timeliness without more equipment or to utilize your equipment more efficiently?

- How are your yields compared to others’ yields, and what is your cost per unit of yield?

5. Develop and implement a risk management plan.

One of the keys of any risk management plan is to identify the amount of risk that you are willing to accept and the risks that you wish to manage. When considering price risk management, you should ask what level of income you wish to guard against. In order to do this, you have to understand your costs of production. Then, put in place a plan to guard against price levels that do not offer an acceptable level of income. Remember that it is not possible to eliminate all risk and retain all opportunities. You must make trade-offs. This is why risk management is so difficult to implement. It requires trade-offs. Quantifying the risks and having a discussion with the rest of your family and/or business partners will likely help you better understand the risks that you are willing to take and the risks that you want to protect against. For producers with a risk management plan already in place, it’s critical to revisit and reevaluate. As market conditions have changed, so has the protection level and effectiveness of various risk management tools. While crop insurance has provided great revenue protection in recent years, in some cases locking in a positive return over variable expenses and land rent, this won’t likely be the case moving forward.

6. Consider diversification.

Diversification provides you with alternative sources of cash flow. However, one must be careful to consider whether alternative crops or enterprises are really going to provide diversification. For example, corn and soybean prices are quite likely to be highly correlated, i.e., both are high or low at the same time. It is likely that the best source of diversification is finding employment off the farm. Additionally, many farmers are heavily invested in farmland. While farmland can be a wonderful financial investment, most farmers have extreme exposure to this asset class. Furthermore, while farmland is a productive and critical asset of the business, it is hard to diversify away this risk.

7. Be willing to make the difficult decision of off-loading enterprises or assets.

Understanding the best alternatives requires one to carefully evaluate how well an asset or operation fits with the overall business and your plans for its future. The 2015 Purdue crop budgets estimated a return over variable costs (or a contribution margin) for wheat greater than that of corn, both rotational and continuous. While market prices can quickly change this relative positioning of commodities, regions of Indiana and the broader Corn Belt will have to carefully watch the returns of these enterprises to make certain they have an appropriate crop rotation.

Off-loading assets is usually a difficult decision to consider. Some farms have likely overbought their equipment inventories. A resourceful strategy might be considering if fewer assets, say tractors, can be justified or if older, lower-valued equipment can be used. Additionally, some farm operations, such as chemical and fertilizer application, can be custom-hired.

Finally, future conditions may warrant certain land assets (both owned and leased) being off-loaded. While the enterprises may be core to the operation, some may not prove as efficient to operate or may be expensive relative to their productivity.

8. Understand and make the government farm program decision.

Although many thought that government programs would not be as important in the future as they were in the past, it is becoming clear that the government program will likely provide substantial benefits. The program offers many choices, including updating base acres and yields and selecting a program(s) for enrollment. It is important that you make a decision as just waiting for the default decision will make you ineligible for 2014 payments. The next key thing to understand is that the program payments will not depend on the crops you plant in the coming years. Finally, the payments will not come until the end of the marketing year, so they will be of little assistance in meeting cash flow needs on the crop that they are paid for. For example, the 2014 corn payments will not arrive until harvest time in 2015, meaning that they will likely help with cash flow needs in 2015, but be of little aid in 2014.

9. Moderate growth and asset ownership strategies.

As the downturn comes, it may be important to carefully consider whether additional expansion is necessary or desirable. While one must continue to think long-term, you should carefully consider how an expansion would impact your financial condition.

10. Communicate with lenders.

Given the importance of cash and liquidity, it will be important to understand your needs for operating credit. Clearly communicating your financial needs and a plan for dealing with lower prices will be very critical in developing a strong relationship with your lender. Have an open dialogue with your lender and understand how they look at your operation. Be honest with where you are, and develop a plan for working through the next several years.

11. Develop a strategic plan.

Many of the choices that are required in a margin squeeze are trade-offs. Developing a long-term plan will help you understand the pros and cons of different trade-offs. The plan development also requires that you discuss the future with your family members and partners. Take time to inventory your current resources and the resources you will need to achieve your plan.

12. Brush up on your agronomic skills.

If input expenses would come down as fast and as much as commodity prices, things wouldn’t be all that bad. Unfortunately, it’s likely that variable expenses will be slow to adjust. This means that it is important to be a wise buyer of inputs. It is also important to assess whether you have been achieving the kinds of yields and outputs that are possible. One might consider whether there are different agronomic practices that could be used to achieve lower variable costs per unit of input. Finally, carefully scout each field to determine the appropriate crop protection practices.

![]()

![]()

![]()

![]()

![]()

TAGS:

TEAM LINKS:

RELATED RESOURCES

UPCOMING EVENTS

We are taking a short break, but please plan to join us at one of our future programs that is a little farther in the future.