May 10, 2021

Impact of Higher Corn Prices On Feeding Cost of Gain for Cattle Finishing

by Michael Langemeier

![]()

![]()

![]()

![]()

![]()

Corn price futures for the July 2021 contract (December 2021 contract) increased from $4.68 per bushel ($4.31 per bushel) in early January to $6.56 ($5.57) for the week ending April 30. Moreover, using the iFarm price distribution tool there was a 25 percent chance on May 4 that the expiration price for the December corn futures contract will be below $4.50 per bushel and a 25 percent chance that price will be above $6.50. Given that the U.S. stocks to use ratio is currently only 9.2 percent and continued questions related to U.S. corn acreage in 2021, there is tremendous uncertainty regarding corn prices for the rest of this year. To address this uncertainty, this article examines the impact of relatively high corn prices on feeding cost of gain for cattle finishing.

Feeding Cost of Gain

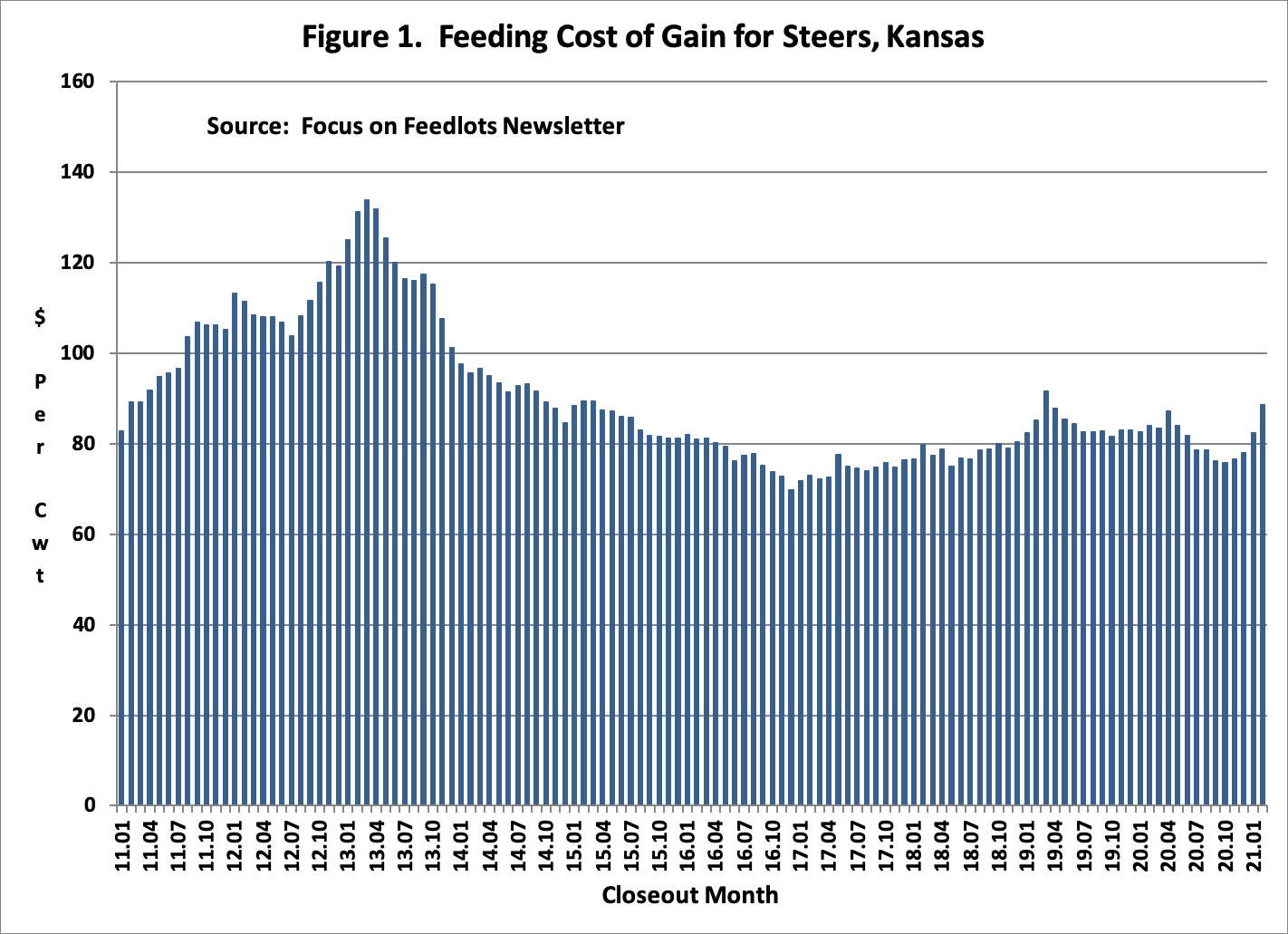

Feeding cost of gain is sensitive to changes in feed conversions, corn prices, and alfalfa prices. Information on these items are available from monthly issues of the Focus on Feedlots newsletter. Figure 1 illustrates feeding cost of gain from January 2011 to February 2021. In February 2021, corn and alfalfa inventory prices were $5.69 per bushel and $167 per ton, respectively. After averaging $80.50 per cwt. in 2020, feeding cost of gain for January and February was $82.30 and $88.60, respectively. The estimated feeding cost of gain in the February issue of Focus on Feedlots for placements in February was $103 per cwt. It is important to note that since this estimate was made corn prices have continued to increase.

Figure 1. Feeding Cost of Gain for Steers, Kansas

Feeding of gain for the rest of 2021 was estimated using early May projections of corn and alfalfa prices, and seasonal average feed conversions. Because feeding cost of gain is computed using corn prices from the time cattle are placed to the time they are sold, the relatively high corn prices we are currently experiencing will impact feeding cost of gain for the next several months. In other words, even though corn prices are expected to decline this fall, feeding cost of gain will remain relatively high through at least the third quarter of 2021. With this in mind, feeding cost of gain for the second quarter of 2021 is expected to range from $93 to $98 per cwt., with the higher cost occurring in June. For the third quarter, feeding cost of gain is expected to range from $102 to $105 per cwt. Feeding cost of gain for the fourth quarter is expected to range from $101 to $104 per cwt., with the highest cost occurring in July. If these feeding costs are realized, they will represent the highest feeding cost of gain since the fourth quarter of 2013.

Sensitivity of Feeding Cost of Gain to Changes in Corn Prices

To determine the sensitivity of feeding cost of gain to changes in corn prices, alfalfa prices, and feed conversion, a regression using data for the last ten years was estimated. Results are as follows: each 0.10 increase in feed conversion increases feeding cost of gain by $1.20 per cwt., each $0.10 per bushel increase in corn prices increases feeding cost of gain by $0.88 per cwt., and each $5 per ton increase in alfalfa prices increases feeding cost of gain by $0.45 per cwt. To more fully understand the impact of feed conversion, corn price, and alfalfa price on feeding cost of gain, we computed coefficients of separate determination (Langemeier et al., 1992). These coefficients can be used to measure the influence of each independent variable upon the dependent variable. The sum of the coefficients of separate determination for each variable equals the R-square goodness of fit measure, which was 0.976 for the feeding cost of gain regression. This goodness of fit statistic indicates that 97.6 percent of the variation in feeding cost of gain was explained by fluctuations in feed conversions, corn prices, and alfalfa prices. Computed coefficients of separate determination indicated that corn price explained approximately 79 percent of the variation in feeding cost of gain.

As noted above, there is currently a $2 per bushel difference between the December corn futures price at expiration at the lower and upper 25 percentiles. The projections above used the middle range of corn prices. For example, the average corn price for July closeouts was projected to be $6.45. If corn price was $1 lower, feeding cost of gain would be $93.10 rather than $101.90. In contrast, if corn was $1 higher, feeding cost of gain would be $110.70 rather than $101.90.

Summary and Conclusions

Corn prices have increased steadily so far this year and are expected to be quite volatile for the rest of the year. This article examined the impact of higher corn prices on feeding cost of gain for cattle finishing. Using projected corn prices, feeding cost of gain is expected to peak in the third quarter at approximately $103.50. However, each $0.10 increase in corn price results in an increase in feeding cost of gain of $0.88 per cwt. If corn prices are $1 higher than projected prices, which is certainly possible in today’s environment, feeding cost of gain would be approximately $111 in the third quarter of 2021.

References

Focus on Feedlots, Animal Sciences and Industry, Kansas State University, www.asi.k-state.edu/about/newsletters/focus-on-feedlots , accessed May 4, 2021.

Langemeier, M., T. Schroeder, and J. Mintert. “Determinants of Cattle Finishing Profitability.” Southern Journal of Agricultural Economics. 24(December 1993):41-47.

![]()

![]()

![]()

![]()

![]()

TAGS:

TEAM LINKS:

RELATED RESOURCES

UPCOMING EVENTS

We are taking a short break, but please plan to join us at one of our future programs that is a little farther in the future.