March 18, 2020

U.S. Is A Pork Export Powerhouse

by James Mintert

![]()

![]()

![]()

![]()

![]()

Recent disruptions to economic activity around the world as a result of the Corona virus have served to reemphasize the importance of trade to the U.S. pork industry. Trade in pork products has grown as the U.S. has turned into a pork export powerhouse. Importantly, the relative importance of U.S. pork’s customers has changed dramatically in recent years suggesting future growth could lie outside traditional destinations. Finally, growth in pork trade means economic conditions in importing countries are important to the U.S. industry.

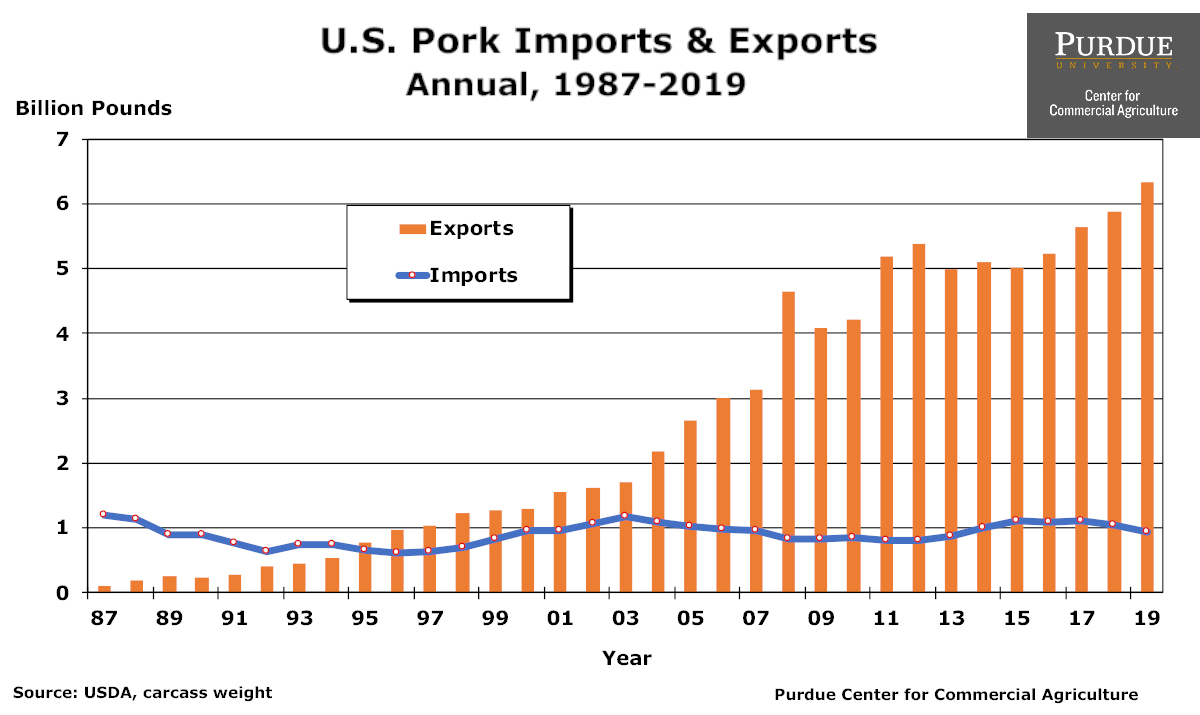

As recently as the mid-1980s the U.S. pork industry exported, worldwide, less than 1 percent of U.S. pork production each year. At the same time, the U.S. was also importing some pork products, equivalent to 6-8 percent of U.S. pork production. The imports augmented the U.S. pork supply, primarily in a small number of products. But world pork trade started to change in the late 1980s and the pace of change accelerated in the 1990s and 2000s.

By 1995 U.S. pork exports measured in carcass weight exceeded pork imports, turning the United States into a net exporter of pork. Exports of pork from the U.S. continued to grow throughout the rest of the 1990s and continued into the 2000s. Over the most recent five years, U.S. pork exports averaged the equivalent of about 22 percent of U.S. pork production. Stated another way, the U.S. was exporting the equivalent of just over 1 out of every 5 hogs in recent years.

While U.S. pork exports were growing, pork imports stagnated in relative terms. In recent years, imports of pork averaged the equivalent of just 4 percent of U.S. production. The result, over the last three plus decades the United States became a large net exporter of pork. Net exports (exports minus imports) of pork were the equivalent of just over 19 percent in 2019 and increased steadily over the last five years.

The destinations for U.S. pork exports have changed since the 1980s. During the 1980s and 1990s U.S. pork exports were driven primarily by exports to Japan. Thirty years ago, Japan was the destination for 55 percent of U.S. pork exports. Ten years ago, Japan absorbed 31 percent of U.S. pork exports, but in 2019 just 18 percent of pork exports were shipped to the Japanese market.

At the same time, Canada and Mexico have become even bigger trading partners than they were years ago. For example, in 2019 25 percent of U.S. pork exports went to Mexico and 9 percent of exports were shipped to Canada. Although both countries were important destinations three decades ago, growth in shipments to these two North American destinations grew rapidly as the total U.S. pork export market grew. Compared to 1994 when NAFTA was implemented, pork exports to Mexico and Canada increased tenfold. In contrast, exports to Japan over this same time frame increased fivefold.

What about China? In 2019, mainland China was the destination for 16 percent of U.S. pork exports. That trade volume was boosted sharply by China’s problems with African swine fever as U.S. shipments to China tripled in 2019 compared to 2018. In contrast to 2019, mainland China took in just 6 percent of U.S. pork exports in 2018. Depending on the status of trade negotiations with China, future growth in pork exports to China could be a bright spot for the U.S. pork industry.

U.S. Pork Imports and Exports Annual, 1987-2019

![]()

![]()

![]()

![]()

![]()

TAGS:

TEAM LINKS:

RELATED RESOURCES

U.S. farm income in 2026 appears stable, but increased government payments are masking weaker livestock receipts and rising costs. Indiana faces a sharper decline, with net farm income projected to fall 28%, highlighting tighter margins and growing financial pressure heading into 2027.

READ MOREUPCOMING EVENTS

We are taking a short break, but please plan to join us at one of our future programs that is a little farther in the future.