March 6, 2013

Farm Managers and Rural Appraisers’ Assessment of Indiana’s Farmland Market

![]()

![]()

![]()

![]()

![]()

Even with a severe drought during the summer of 2012, the Indiana land market continues to move higher. The February 2013 issue of the AgLetter, a Federal Reserve Bank of Chicago newsletter, indicated that farmland values in the Seventh District (Iowa, and parts of Illinois, Indiana, Michigan, and Wisconsin) increased 16% from January 1, 2012 to January 1, 2013. This was the third highest increase since the late 70s.

To obtain a perspective about changes in Indiana’s farmland market, members of the Indiana Chapter of Farm Managers & Rural Appraisers were surveyed during their winter meeting on February 5, 2013. To obtain information about Indiana’s farmland market, members were asked to estimate current farmland values in the context of the following situation:

80 acres or more, all tillable, no buildings, capable of averaging 165 bushels of corn per acre and 50 bushels of soybeans in a corn/bean rotation under typical management and not having special non-farm uses.

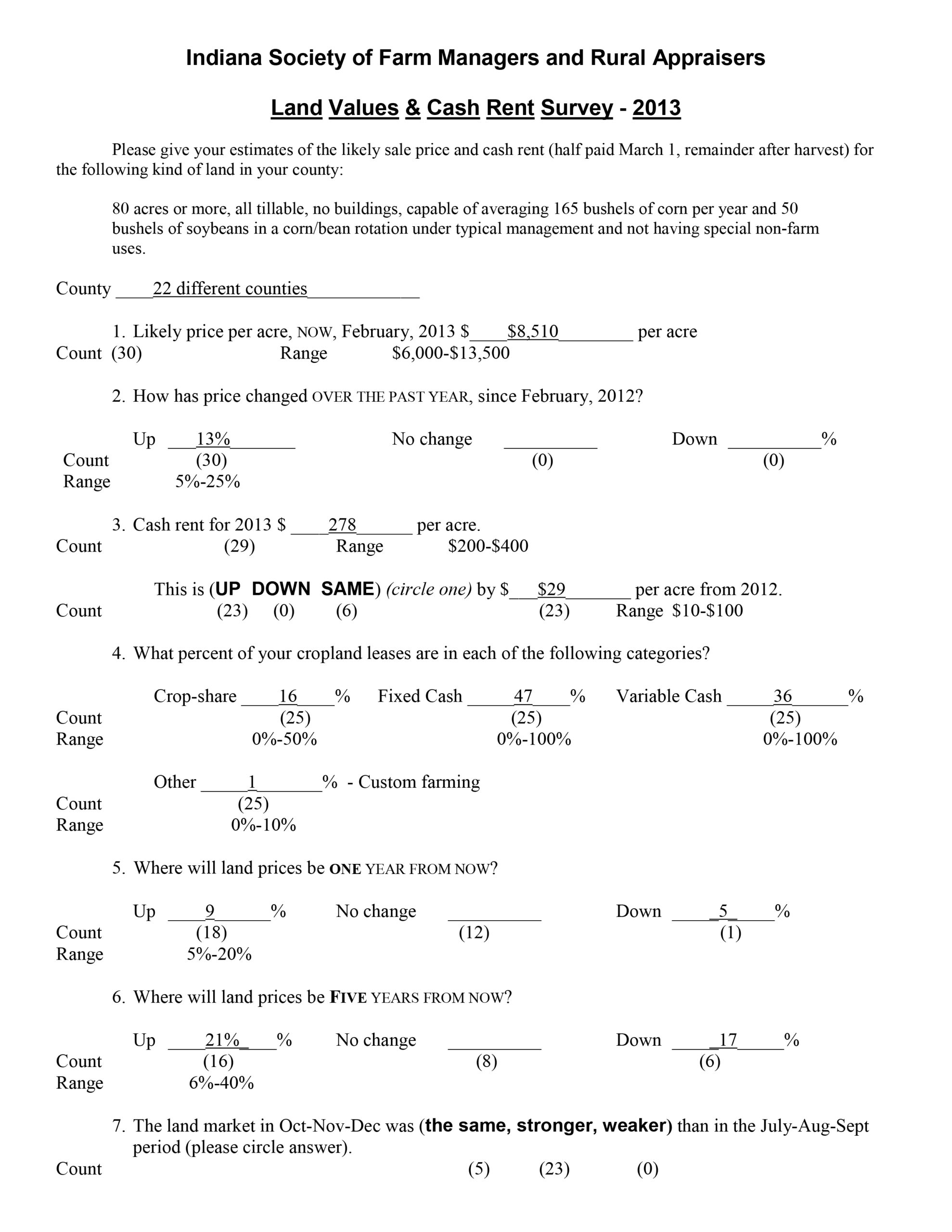

Thirty responses were received from people in 22 different Indiana counties. The average estimated price of farmland was $8,510 per acre. All of the respondents indicated their estimated price was higher than the value in February 2012. The average percentage increase from February 2012 to February 2013 was 13%. This makes the annual percentage increase more than the annual increase of 10% reported for Indiana in the Federal Reserve Bank of Chicago survey. The range in estimated increase provided by the farm managers & rural appraisers was 5% to 25%.

Attendees were also asked to estimate the cash rent for 2013 given the previously described situation. The average cash rent was $278 per acre. Twenty-three of the respondents indicated that cash rent was higher than in 2012 and six respondents indicated it was the same. No one indicated a decline in cash rent. On average, the cash rent increased $29 per acre; an increase of 12%. There was a wide range in the estimated cash rent and cash rent change. Estimated cash rent varied from $200 to $400 per acre. The change in cash rent varied from $10 to $100 per acre.

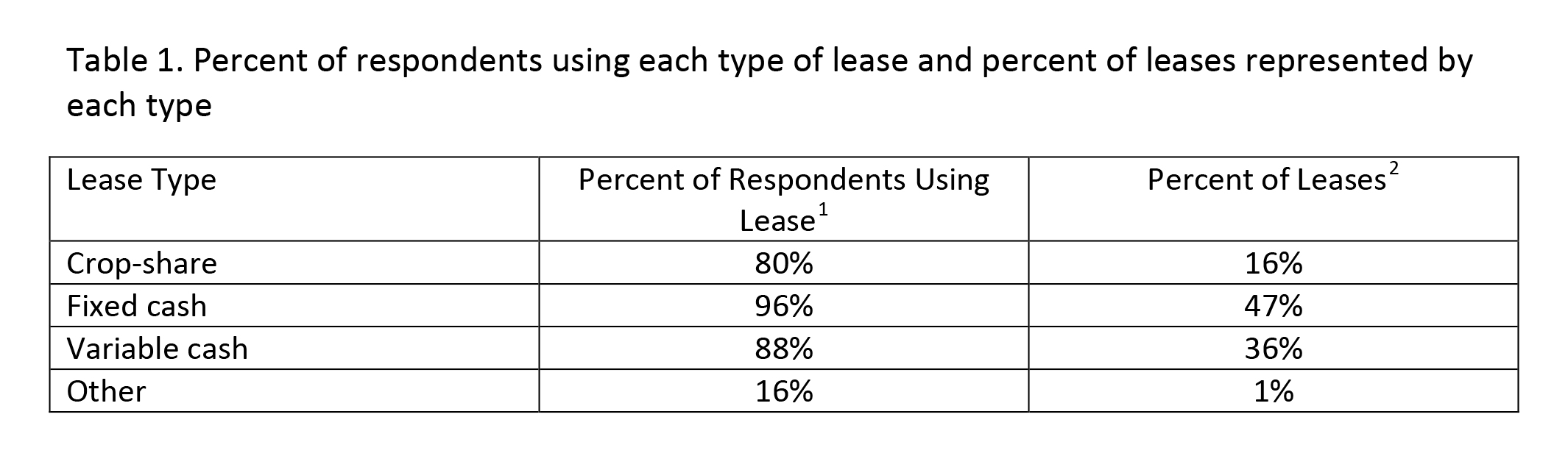

The increased variability of net returns associated with leasing farmland has prompted tenants and landlords to experiment with various types of adjustable leases. To get a sense of the type of lease used, attendees were asked to report the percentage of their cropland leases that were crop-share, fixed cash, variable cash, and other. The percentage of the respondents that reported using each type of lease and the percentage of their leases of each type is presented in Table 1.

Crop-share, fixed cash, and variable cash leases all had a high rate of usage among the respondents. Many of the respondents were using all three types of lease. The most commonly used lease was the fixed cash lease, averaging 47% of the leases. This was followed by the variable cash lease at 36%. Crop-share leases were 16% of the leases.Many people ask if the increase in farmland values is likely to continue. The farm managers and rural appraisers were asked to provide two forecasts about future farmland values. One was where farmland values would be in one year. The second was where land values would be in five years. When asked about land values in one year, 60% of the respondents indicated that values would be higher. The other 40% said there would be no change. The expected increase averaged 9% with a range of 5% to 20%.There was less agreement about the change in farmland values over the next five year. In this case, 53% of the respondents indicated farmland values would be higher, 27% indicated there would be no change, and 20% indicated farmland values would be lower. For those respondents indicating that farmland values would be higher, the expected increase averaged 21% with a range from 6% to 40%. For those respondents expecting a decrease in farmland values, the decrease averaged 17% with a range from 10% to 25%.

These results indicate that in the short term, Indiana’s farmland market is expected to remain strong. No one expects farmland values to decline for the year, but relative to the past few years, respondents expect the rate of increase to be much less. Longer term there is less certainty in how farmland values will change. More respondents expect farmland values to be steady or higher than to decline in five years, but sound risk management suggests that the effect of a 10% to 25% decline in farmland values on the business needs to be explored.

Indiana Society of Farm Manager and Rural Appraisers, Land Values & Cash Rent Survey – 2013

[1] These will not total 100% because a respondent often uses more than one type of lease.

[2] Across the different types of leases the total will be 100%.

*A special thanks is expressed to the Indiana Chapter of Farm Managers and Rural Appraisers that participated in the survey. Without their assistance it would not have been possible to take the pulse of Indiana’s farmland.

![]()

![]()

![]()

![]()

![]()

TAGS:

TEAM LINKS:

RELATED RESOURCES

UPCOMING EVENTS

We are taking a short break, but please plan to join us at one of our future programs that is a little farther in the future.