July 26, 2021

International Benchmarks for Wheat Production (2021)

by Michael Langemeier

![]()

![]()

![]()

![]()

![]()

Examining the competitiveness of wheat production in different regions of the world is often difficult due to lack of comparable data and agreement regarding what needs to be measured. To be useful, international data needs to be expressed in common production units and converted to a common currency. Also, production and cost measures need to be consistently defined across production regions or farms.

This paper examines the competitiveness of wheat production for important international wheat production regions using 2015 to 2019 data from the agri benchmark network. An earlier paper examined international benchmarks for the 2013 to 2017 period (here). The agri benchmark network collects data on beef, cash crops, dairy, pigs and poultry, horticulture, and organic products. There are 23 countries with data for 2019 represented in the cash crop network. The agri benchmark concept of typical farms was developed to understand and compare current farm production systems around the world. Participant countries follow a standard procedure to create typical farms that are representative of national farm output shares, and categorized by production system or combination of enterprises and structural features. Costs and revenues are converted to U.S. dollars so that comparisons can be readily made. Data from ten typical farms with wheat enterprise data from Argentina, Australia, Canada, Germany, Russia, Ukraine, and United States were used in this paper. It is important to note that wheat enterprise data is collected from other countries. These seven countries were selected to simplify the illustration and discussion.

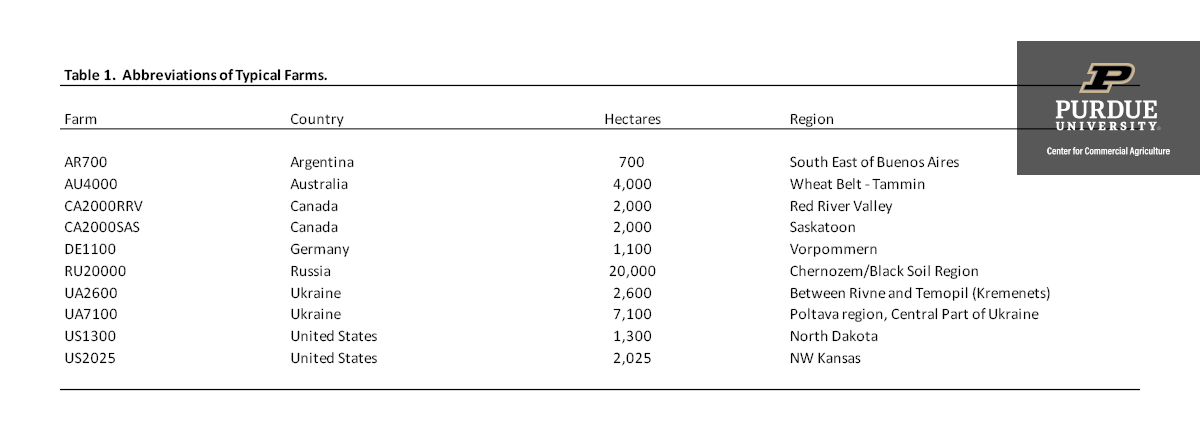

The farm and country abbreviations used in this paper are listed in table 1. All of the farms, except for the typical farm in Australia, had data for each year from 2015 to 2019. The typical farm in Australia had data for the 2015 to 2018 period. While the farms may produce a variety of crops, this paper only considers wheat production. Typical farms used in the agri benchmark network are defined using country initials and hectares on the farm. To fully understand the relative importance of the wheat enterprise on each typical farm, it is useful to note all of the crops produced. The typical farm in Argentina produced corn, soybeans, sunflowers, winter barley, and winter wheat in 2019. Wheat was produced on approximately 45 percent of the typical farm’s acreage during the five-year period. The typical farm in Australia produced malting barley, winter rapeseed, and summer wheat. Wheat was produced on approximately 41 percent of the typical farm’s acreage. The Canadian farm in the Red River Valley produced corn, summer rapeseed, soybeans, and summer wheat with wheat representing 32 percent of the farm’s acreage during the five-year period. The typical farm in Saskatoon produced malting barley, oats, linseed, summer rapeseed, peas, and summer wheat with wheat representing approximately 44 percent of the farm’s acreage during the five-year period. The German farm produced winter barley, corn silage, winter rapeseed, and winter wheat. During the five-year period, wheat was planted on 48 percent of the typical farm’s acreage. The farm in Russia produced alfalfa, chickpeas, corn, corn silage, fodder grass, soybeans, sugar beets, summer barley, sunflowers, winter rye, and winter wheat in 2019. Wheat was produced on approximately 12 percent of the typical farm’s acreage during the five-year period. The smaller farm in the Ukraine produced corn, winter rapeseed, soybeans, sunflowers, and winter wheat with wheat representing approximately 41 percent of the typical farm’s acreage during the five-year period. Crops produced on the larger farm in the Ukraine in 2019 included corn, winter rapeseed, soybeans, sunflowers, and winter wheat. Wheat was produced on approximately 19 percent of the typical farm’s acreage during the five-year period. There are five U.S. farms with corn in the network. The typical farms in North Dakota and Kansas are represented in this study. The typical farm in North Dakota produced corn, soybeans, and summer wheat in 2019. Wheat was produced on approximately 17 percent of the typical farm’s acreage during the five-year period. The typical farm in Kansas produced corn and winter wheat. Wheat was produced on approximately 36 percent of the typical farm’s acreage during the five-year period.

Table 1. Abbreviations of Typical Farms.

Wheat Yields

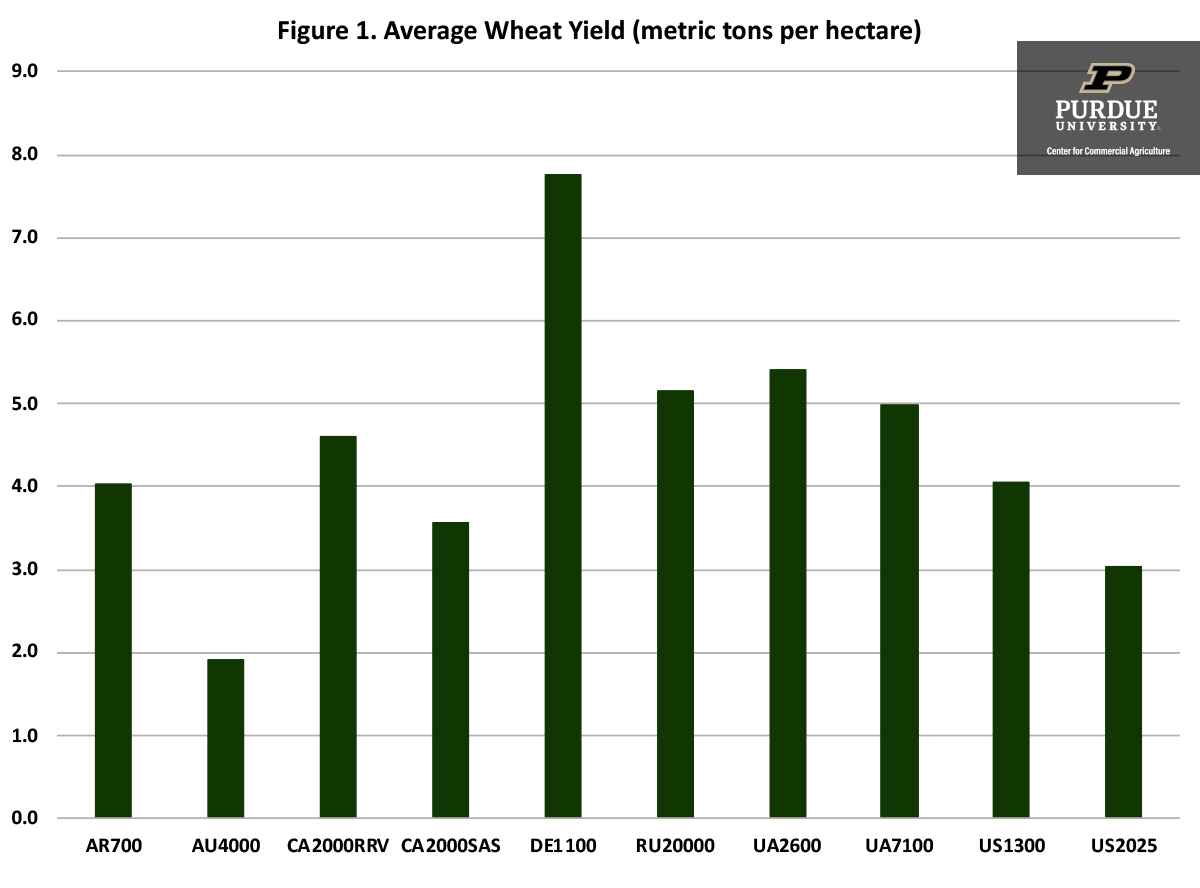

Although yield is only a partial gauge of performance, it reflects the available production technology across farms. Average wheat yield for the farms in 2015 to 2019 was 4.45 metric tons per hectare (66.2 bushels per acre). Average farm yields ranged from approximately 1.91 metric tons per hectare (28.3 bushels per acre) for the typical farm in Australia to 7.76 metric tons per hectare (115.4 bushels per acre) for the typical farm in Germany. Figure 1 illustrates average wheat yield for each typical farm. The farms in North Dakota and Kansas had average yields of 60.4 and 45.1 bushels per acre (4.06 and 3.03 metric tons per hectare), respectively.

Figure 1. Average Wheat Yield (metric tons per hectare)

Input Cost Shares

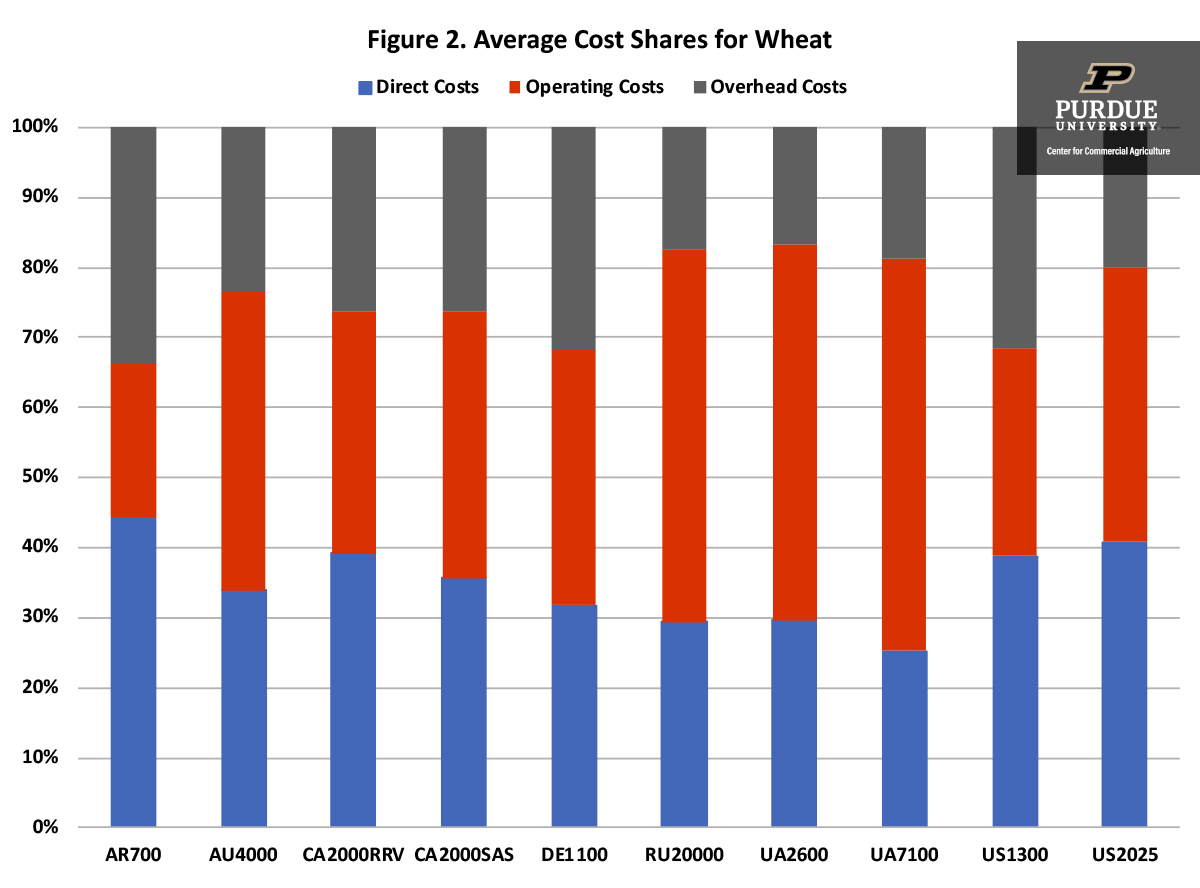

Due to differences in technology adoption, input prices, fertility levels, efficiency of farm operators, trade policy restrictions, exchange rate effects, and labor and capital market constraints, input use varies across wheat farms. Figure 2 presents the average input cost shares for each farm. Cost shares were broken down into three major categories: direct costs, operating costs, and overhead costs. Direct costs included seed, fertilizer, crop protection, crop insurance, and interest on these cost items. Operating cost included labor, machinery depreciation and interest, contractor cost, fuel, and repairs. Overhead cost included land, building depreciation and interest, property taxes, general insurance, and miscellaneous cost.

The average input cost shares were 34.9 percent for direct cost, 40.6 percent for operating cost, and 24.6 percent for overhead cost. The typical farms in Russia and Ukraine had the lowest cost shares for direct cost which includes crop establishment costs pertaining to seed, fertilizer, and pesticides. The typical farms in Argentina and in North Dakota had the lowest cost shares in terms of operating cost. Labor costs as a proportion of total costs were relatively higher for the typical farms in the Ukraine, the typical farm in Australia, and typical farm in Germany. Overhead costs as a proportion of total costs were relatively higher in Argentina, in Germany, and in North Dakota. In general, overhead costs are driven by land cost.

Figure 2. Average Cost Shares for Wheat

Revenue and Cost

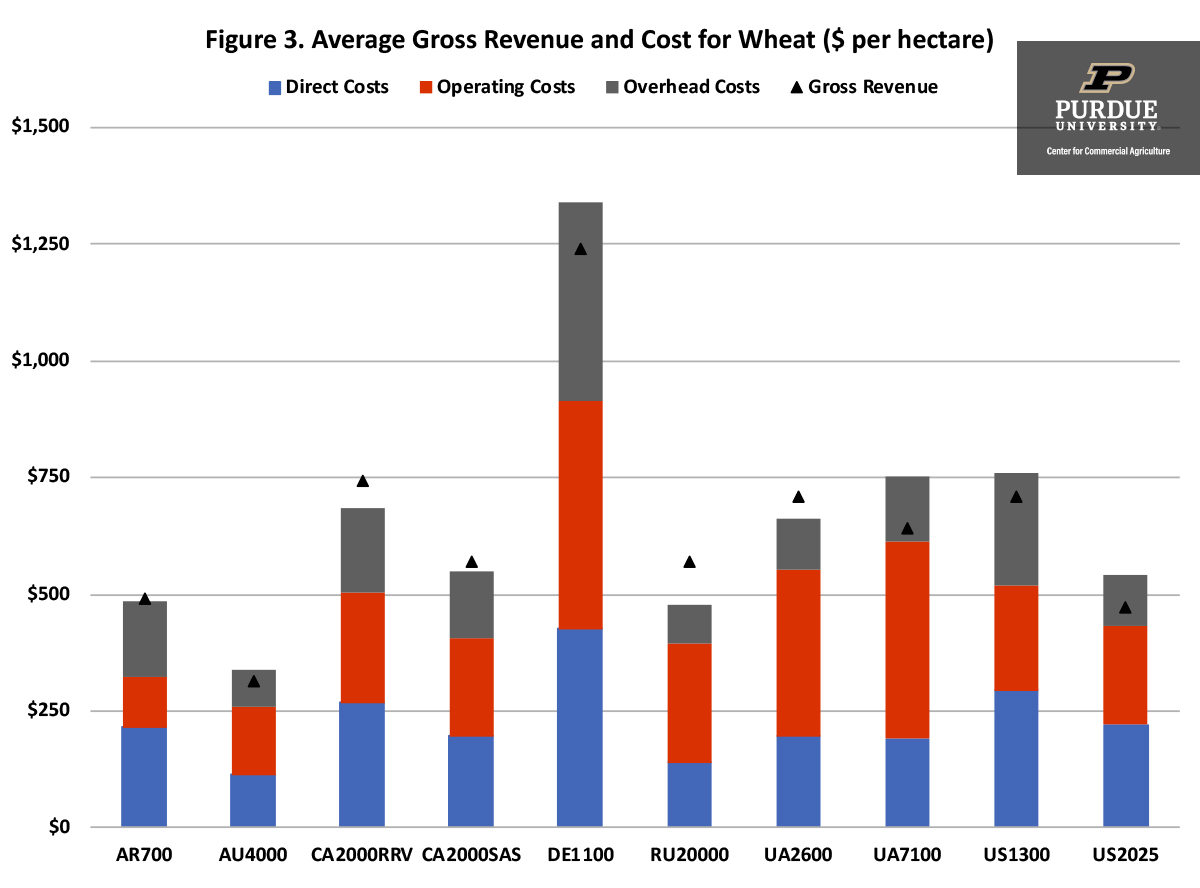

Figure 3 presents average gross revenue and cost for each typical farm. Gross revenue and cost are reported as U.S. dollars per hectare. It is obvious from figure 3 that gross revenue per hectare is substantially higher for the typical farm in Germany. However, cost is also substantially higher for this farm. The typical farms from Argentina, Canada, and Russia exhibited economic profit during the five-year period. In addition, the smallest typical farm in Ukraine also had a positive economic profit during the study period. Average losses per hectare for the typical farms in Australia, Germany, North Dakota, and Kansas were $23, $100, $48, and $68 per hectare, respectively, during the five-year period. The largest typical farm in the Ukraine had an average loss per hectare of $113. The lowest economic profit during the five-year period for the typical farms was 2019 with an average loss of $75 per hectare. Both 2015 and 2017 had an average economic profit that was positive.

Figure 3. Average Gross Revenue and Cost for Wheat ($ per hectare)

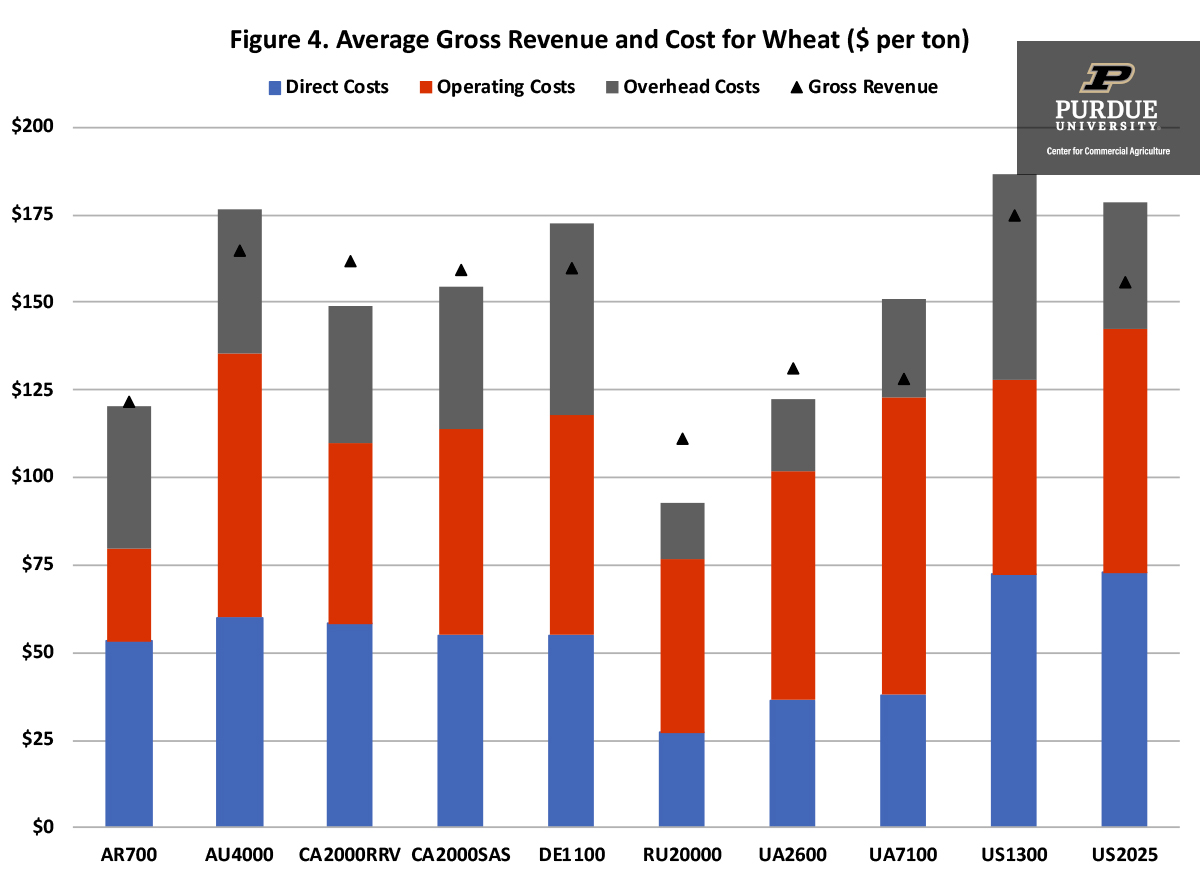

Figure 4 presents average gross revenue and cost for wheat on a per ton basis. Gross revenue per ton was relatively higher for the typical farms in Australia, Canada, Germany, and the United States. However, the typical farms in Australia, Germany, and the United States also had the highest costs per ton. Economic profit for the five-year period was the highest for the typical farm in Russia and the typical farm in the Red River Valley region of Canada.

Figure 4. Average Gross Revenue and Cost for Wheat ($ per ton)

Conclusions

This paper examined yield, gross revenue, and cost for farms in the agri benchmark network from Argentina, Australia, Canada, Germany, Russia, the Ukraine, and the United States with wheat enterprise data. The German farm had the highest yield. However, this farm had an average loss per ton of $13 over the 2015 to 2019 period. The typical farms in Argentina, Canada, and Russia exhibited a positive average economic profit during the 2015 to 2019 period. The data for 2020 will be available early this fall. It will be interesting to see how the strong crop prices that occurred in the later part of 2020 will impact comparative results.

References

agri benchmark. http://www.agribenchmark.org/home.html. Accessed on May 24, 2021.

Langemeier, M. and R. Purdy. “International Benchmarks for Wheat Production.” Center for Commercial Agriculture, Purdue University, May 2019.

![]()

![]()

![]()

![]()

![]()

TAGS:

TEAM LINKS:

RELATED RESOURCES

UPCOMING EVENTS

We are taking a short break, but please plan to join us at one of our future programs that is a little farther in the future.